Bank of America 2014 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

Bank of America 2014 37

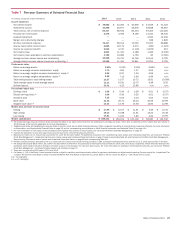

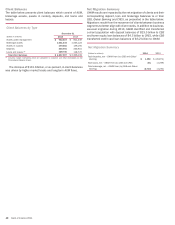

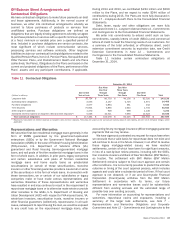

Legacy Serviced Portfolio

The Legacy Serviced Portfolio includes loans serviced by Legacy

Assets & Servicing in both the Legacy Owned Portfolio and those

loans serviced for outside investors that met the criteria as

described above. The table below summarizes the balances of the

residential mortgage loans included in the Legacy Serviced

Portfolio (the Legacy Residential Mortgage Serviced Portfolio)

representing 24 percent, 28 percent and 38 percent of the total

residential mortgage serviced portfolio of $609 billion, $719

billion and $1.2 trillion, as measured by unpaid principal balance,

at December 31, 2014, 2013 and 2012, respectively. The decline

in the Legacy Residential Mortgage Serviced Portfolio was primarily

due to MSR sales, loan sales and other servicing transfers,

paydowns and payoffs.

Legacy Residential Mortgage Serviced Portfolio, a subset

of the Residential Mortgage Serviced Portfolio (1)

December 31

(Dollars in billions) 2014 2013 2012

Unpaid principal balance

Residential mortgage loans

Total $ 148 $ 203 $ 467

60 days or more past due 25 49 137

Number of loans serviced (in thousands)

Residential mortgage loans

Total 794 1,083 2,542

60 days or more past due 135 258 649

(1) Excludes $34 billion, $39 billion and $52 billion of home equity loans and HELOCs at

December 31, 2014, 2013 and 2012, respectively.

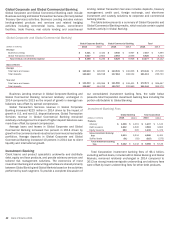

Non-Legacy Portfolio

As previously discussed, Legacy Assets & Servicing is responsible

for all of our servicing activities. The table below summarizes the

balances of the residential mortgage loans that are not included

in the Legacy Serviced Portfolio (the Non-Legacy Residential

Mortgage Serviced Portfolio) representing 76 percent, 72 percent

and 62 percent of the total residential mortgage serviced portfolio,

as measured by unpaid principal balance, at December 31, 2014,

2013 and 2012, respectively. The decline in the Non-Legacy

Residential Mortgage Serviced Portfolio was primarily due to MSR

sales and other servicing transfers, paydowns and payoffs.

Non-Legacy Residential Mortgage Serviced Portfolio, a

subset of the Residential Mortgage Serviced Portfolio (1)

December 31

(Dollars in billions) 2014 2013 2012

Unpaid principal balance

Residential mortgage loans

Total $ 461 $ 516 $ 755

60 days or more past due 912 22

Number of loans serviced (in thousands)

Residential mortgage loans

Total 2,951 3,267 4,764

60 days or more past due 54 67 124

(1) Excludes $50 billion, $52 billion and $58 billion of home equity loans and HELOCs at

December 31, 2014, 2013 and 2012, respectively.

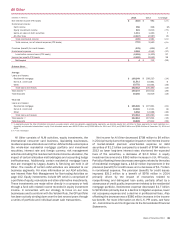

Mortgage Banking Income

CRES mortgage banking income is categorized into production and

servicing income. Core production income is comprised primarily

of revenue from the fair value gains and losses recognized on our

interest rate lock commitments (IRLCs) and LHFS, the related

secondary market execution and costs related to representations

and warranties in the sales transactions along with other

obligations incurred in the sales of mortgage loans. Ongoing costs

related to representations and warranties and other obligations

that were incurred in the sales of mortgage loans in prior periods

are also included in production income.

Servicing income includes income earned in connection with

servicing activities and MSR valuation adjustments, net of results

from risk management activities used to hedge certain market

risks of the MSRs. The costs associated with our servicing

activities are included in noninterest expense.

The table below summarizes the components of mortgage

banking income.

Mortgage Banking Income

(Dollars in millions) 2014 2013

Production income:

Core production revenue $ 1,181 $ 2,543

Representations and warranties provision (683) (840)

Total production income 498 1,703

Servicing income:

Servicing fees 1,884 3,030

Amortization of expected cash flows (1) (818) (1,043)

Fair value changes of MSRs, net of risk management

activities used to hedge certain market risks (2) 294 867

Other servicing-related revenue 828

Total net servicing income 1,368 2,882

Total CRES mortgage banking income 1,866 4,585

Eliminations (3) (303) (711)

Total consolidated mortgage banking income $ 1,563 $ 3,874

(1) Represents the net change in fair value of the MSR asset due to the recognition of modeled

cash flows.

(2) Includes gains (losses) on sales of MSRs.

(3) Includes the effect of transfers of mortgage loans from CRES to the ALM portfolio included in

All Other and intercompany allocations of servicing costs.

Core production revenue decreased $1.4 billion to $1.2 billion

in 2014 due to lower first mortgage origination volumes as

described below, and to a lesser extent, industry-wide margin

compression. The representations and warranties provision

decreased $157 million to $683 million and was primarily related

to non-government-sponsored enterprises exposures, partially

offset by lower exposure to mortgage insurance companies as a

result of settlements in 2014.

Net servicing income decreased $1.5 billion to $1.4 billion

driven by lower servicing fees due to a smaller servicing portfolio

and less favorable MSR net-of-hedge performance, partially offset

by lower amortization of expected cash flows. The decline in the

size of our servicing portfolio was driven by strategic sales of MSRs

during 2014 and 2013 as well as loan prepayment activity, which

exceeded new originations primarily due to our exit from non-retail

channels.