Bank of America 2014 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

Bank of America 2014 67

Credit Risk Management

Credit quality improved during 2014 due in part to improving

economic conditions. In addition, our proactive credit risk

management activities positively impacted the credit portfolio as

charge-offs and delinquencies continued to improve. For additional

information, see Executive Summary – 2014 Economic and

Business Environment on page 20.

Credit risk is the risk of loss arising from the inability or failure

of a borrower or counterparty to meet its obligations. Credit risk

can also arise from operational failures that result in an erroneous

advance, commitment or investment of funds. We define the credit

exposure to a borrower or counterparty as the loss potential arising

from all product classifications including loans and leases, deposit

overdrafts, derivatives, assets held-for-sale and unfunded lending

commitments which include loan commitments, letters of credit

and financial guarantees. Derivative positions are recorded at fair

value and assets held-for-sale are recorded at either fair value or

the lower of cost or fair value. Certain loans and unfunded

commitments are accounted for under the fair value option. Credit

risk for categories of assets carried at fair value is not accounted

for as part of the allowance for credit losses but as part of the fair

value adjustments recorded in earnings. For derivative positions,

our credit risk is measured as the net cost in the event the

counterparties with contracts in which we are in a gain position

fail to perform under the terms of those contracts. We use the

current fair value to represent credit exposure without giving

consideration to future mark-to-market changes. The credit risk

amounts take into consideration the effects of legally enforceable

master netting agreements and cash collateral. Our consumer and

commercial credit extension and review procedures encompass

funded and unfunded credit exposures. For more information on

derivatives and credit extension commitments, see Note 2 –

Derivatives and Note 12 – Commitments and Contingencies to the

Consolidated Financial Statements.

We manage credit risk based on the risk profile of the borrower

or counterparty, repayment sources, the nature of underlying

collateral, and other support given current events, conditions and

expectations. We classify our portfolios as either consumer or

commercial and monitor credit risk in each as discussed below.

We proactively refine our underwriting and credit management

practices as well as credit standards to meet the changing

economic environment. To actively mitigate losses and enhance

customer support in our consumer businesses, we have in place

collection programs and loan modification and customer

assistance infrastructures. We utilize a number of actions to

mitigate losses in the commercial businesses including increasing

the frequency and intensity of portfolio monitoring, hedging activity

and our practice of transferring management of deteriorating

commercial exposures to independent special asset officers as

credits enter criticized categories.

We have non-U.S. exposure largely in Europe and Asia Pacific.

For more information on our exposures and related risks in non-

U.S. countries, see Non-U.S. Portfolio on page 90 and Item 1A.

Risk Factors of our 2014 Annual Report on Form 10-K.

For more information on our credit risk management activities,

see Consumer Portfolio Credit Risk Management on page 67,

Commercial Portfolio Credit Risk Management on page 81, Non-

U.S. Portfolio on page 90, Provision for Credit Losses on page 92

and Allowance for Credit Losses on page 92, Note 1 – Summary

of Significant Accounting Principles, Note 4 – Outstanding Loans

and Leases and Note 5 – Allowance for Credit Losses to the

Consolidated Financial Statements.

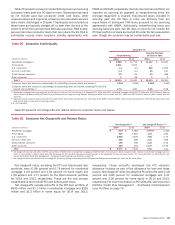

Consumer Portfolio Credit Risk Management

Credit risk management for the consumer portfolio begins with

initial underwriting and continues throughout a borrower’s credit

cycle. Statistical techniques in conjunction with experiential

judgment are used in all aspects of portfolio management

including underwriting, product pricing, risk appetite, setting credit

limits, and establishing operating processes and metrics to

quantify and balance risks and returns. Statistical models are built

using detailed behavioral information from external sources such

as credit bureaus and/or internal historical experience. These

models are a component of our consumer credit risk management

process and are used in part to assist in making both new and

ongoing credit decisions, as well as portfolio management

strategies, including authorizations and line management,

collection practices and strategies, and determination of the

allowance for loan and lease losses and allocated capital for credit

risk.

During 2014, we completed approximately 71,600 customer

loan modifications with a total unpaid principal balance of

approximately $13 billion, including approximately 33,400

permanent modifications, under the U.S. government’s Making

Home Affordable Program. Of the loan modifications completed in

2014, in terms of both the volume of modifications and the unpaid

principal balance associated with the underlying loans,

approximately half were in the Corporation’s held-for-investment

(HFI) portfolio. For modified loans on our balance sheet, these

modification types are generally considered troubled debt

restructurings (TDRs). For more information on TDRs and portfolio

impacts, see Consumer Portfolio Credit Risk Management –

Nonperforming Consumer Loans, Leases and Foreclosed

Properties Activity on page 79 and Note 4 – Outstanding Loans

and Leases to the Consolidated Financial Statements.

Consumer Credit Portfolio

Improvement in the U.S. economy, labor markets and home prices

continued during 2014 resulting in improved credit quality and

lower credit losses across all consumer portfolios compared to

2013. Consumer loans 30 days or more past due and 90 days or

more past due declined during 2014 across all consumer

portfolios as a result of improved delinquency trends. Although

home prices have shown steady improvement since the beginning

of 2012, they have not fully recovered to their 2006 levels.

Improved credit quality, increased home prices and continued

loan balance run-off across the consumer portfolio drove a $3.4

billion decrease in the consumer allowance for loan and lease

losses in 2014 to $10.0 billion at December 31, 2014. For more

information, see Allowance for Credit Losses on page 92.

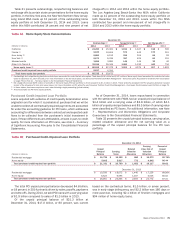

In connection with the 2013 settlement with FNMA, we

repurchased certain residential mortgage loans that had

previously been sold to FNMA, which we have valued at less than

the purchase price. As of December 31, 2014, these loans had

an unpaid principal balance of $4.4 billion and a carrying value of

$3.8 billion, of which $4.1 billion of unpaid principal balance and

$3.5 billion of carrying value were classified as PCI loans. All of

these loans are included in the Legacy Assets & Servicing portfolio

in Table 27. For more information on PCI loans, see Consumer

Portfolio Credit Risk Management – Purchased Credit-impaired

Loan Portfolio on page 75 and Note 4 – Outstanding Loans and

Leases to the Consolidated Financial Statements.

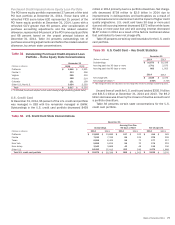

For more information on our accounting policies regarding

delinquencies, nonperforming status, charge-offs and TDRs for the