Bank of America 2014 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

Bank of America 2014 105

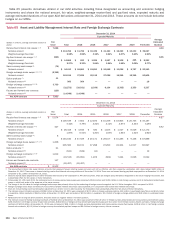

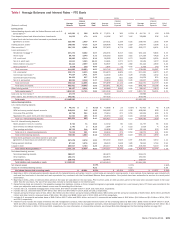

We use interest rate derivative instruments to hedge the

variability in the cash flows of our assets and liabilities and other

forecasted transactions (collectively referred to as cash flow

hedges). The net losses on both open and terminated cash flow

hedge derivative instruments recorded in accumulated OCI were

$2.7 billion and $3.6 billion, on a pretax basis, at December 31,

2014 and 2013. These net losses are expected to be reclassified

into earnings in the same period as the hedged cash flows affect

earnings and will decrease income or increase expense on the

respective hedged cash flows. Assuming no change in open cash

flow derivative hedge positions and no changes in prices or interest

rates beyond what is implied in forward yield curves at

December 31, 2014, the pretax net losses are expected to be

reclassified into earnings as follows: $803 million, or 30 percent

within the next year, 46 percent in years two through five, and 16

percent in years six through ten, with the remaining eight percent

thereafter. For more information on derivatives designated as cash

flow hedges, see Note 2 – Derivatives to the Consolidated Financial

Statements.

We hedge our net investment in non-U.S. operations determined

to have functional currencies other than the U.S. Dollar using

forward foreign exchange contracts that typically settle in less than

180 days, cross-currency basis swaps and foreign exchange

options. We recorded net after-tax losses on derivatives in

accumulated OCI associated with net investment hedges which

were offset by gains on our net investments in consolidated non-

U.S. entities at December 31, 2014.

Mortgage Banking Risk Management

We originate, fund and service mortgage loans, which subject us

to credit, liquidity and interest rate risks, among others. We

determine whether loans will be HFI or held-for-sale at the time of

commitment and manage credit and liquidity risks by selling or

securitizing a portion of the loans we originate.

Interest rate risk and market risk can be substantial in the

mortgage business. Fluctuations in interest rates drive consumer

demand for new mortgages and the level of refinancing activity,

which in turn affects total origination and servicing income.

Hedging the various sources of interest rate risk in mortgage

banking is a complex process that requires complex modeling and

ongoing monitoring. Typically, an increase in mortgage interest

rates will lead to a decrease in mortgage originations and related

fees. IRLCs and the related residential first mortgage LHFS are

subject to interest rate risk between the date of the IRLC and the

date the loans are sold to the secondary market, as an increase

in mortgage interest rates will typically lead to a decrease in the

value of these instruments.

MSRs are nonfinancial assets created when the underlying

mortgage loan is sold to investors and we retain the right to service

the loan. Typically, an increase in mortgage rates will lead to an

increase in the value of the MSRs driven by lower prepayment

expectations. This increase in value from increases in mortgage

rates is opposite of, and therefore offsets, the risk described for

IRLCs and LHFS. Previously we hedged MSRs separately from the

IRLCs and first mortgage LHFS assets. Because the interest rate

risks of these two hedged items offset, we decided to combine

them into one overall hedged item with one combined economic

hedge portfolio.

Beginning in the fourth quarter of 2014, interest rate and

certain market risks of IRLCs and residential mortgage LHFS were

economically hedged in combination with MSRs. To hedge these

combined assets, we use certain derivatives such as interest rate

options, interest rate swaps, forward sale commitments,

eurodollar and U.S. Treasury futures, and mortgage TBAs, as well

as other securities including agency MBS, principal-only and

interest-only MBS and U.S. Treasury securities. The fair value and

notional amounts of the derivative contracts and the fair value of

securities hedging the combined MSRs, IRLCs and residential first

mortgage LHFS were $(3.6) billion, $1.1 trillion and $558 million

at December 31, 2014. The fair value and notional amounts of

the derivative contracts and the fair value of securities hedging

the MSRs at December 31, 2013 were $(2.9) billion, $1.8 trillion

and $2.5 billion. The notional amount of derivatives economically

hedging only the IRLCs and residential first mortgage LHFS at

December 31, 2013 were $7.9 billion. In 2014, we recorded in

mortgage banking income gains of $1.6 billion related to the

change in fair value of the derivative contracts and other securities

used to hedge the market risks of the MSRs compared to losses

of $1.1 billion for 2013. For more information on MSRs, see Note

23 – Mortgage Servicing Rights to the Consolidated Financial

Statements and for more information on mortgage banking

income, see CRES on page 35.

Compliance Risk Management

Compliance risk is the risk of legal or regulatory sanctions, material

financial loss or damage to the reputation of the Corporation in

the event of the failure of the Corporation to comply with the

requirements of applicable laws, rules, regulations, related self-

regulatory organization standards and codes of conduct

(collectively, applicable laws, rules and regulations). Global

Compliance independently assesses compliance risk, and

evaluates adherence to applicable laws, rules and regulations,

including identifying compliance issues and risks, performing

monitoring and testing, and reporting on the state of compliance

activities across the Corporation. Additionally, Global Compliance

works with FLUs and control functions so that day-to-day activities

operate in a compliant manner. For more information on FLUs and

control functions, see Managing Risk on page 52.

The Corporation’s approach to the management of compliance

risk is further described in the Global Compliance Policy, which

outlines the requirements of the Corporation’s global compliance

program, and defines roles and responsibilities related to the

implementation, execution and management of the compliance

program by Global Compliance. The requirements work together

to drive a comprehensive risk-based approach for the proactive

identification, management and escalation of compliance risks

throughout the Corporation.

The Global Compliance Policy sets the requirements for

reporting compliance risk information to executive management

as well as the Board or appropriate Board-level committees with

an outline for conducting objective oversight of the Corporation’s

compliance risk management activities. The Board provides

oversight of compliance risks through its Audit Committee and

ERC.