Bank of America 2014 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

Bank of America 2014 91

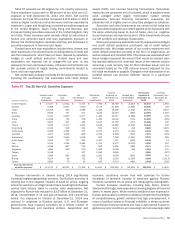

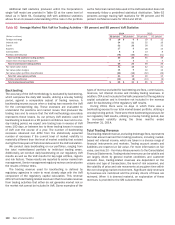

Table 57 presents our 20 largest non-U.S. country exposures.

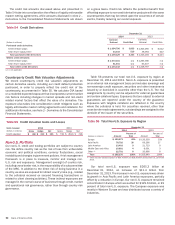

These exposures accounted for 88 percent of our total non-U.S.

exposure at both December 31, 2014 and 2013. Net country

exposure for these 20 countries increased $13.6 billion in 2014

driven by higher funded and unfunded loans and loan equivalents

exposure in Japan and Hong Kong, increased derivatives exposure

in the United Kingdom, Japan, Hong Kong and Germany, and

increased trading securities exposure in the United Kingdom, Italy

and India. These increases were partially offset by reductions in

funded and unfunded loans and loan equivalents exposure in

Russia, the United Kingdom, Australia and Italy, and decreases in

securities exposure in Germany and Japan.

Funded loans and loan equivalents include loans, leases, and

other extensions of credit and funds, including letters of credit and

due from placements, which have not been reduced by collateral,

hedges or credit default protection. Funded loans and loan

equivalents are reported net of charge-offs but prior to any

allowance for loan and lease losses. Unfunded commitments are

the undrawn portion of legally binding commitments related to

loans and loan equivalents.

Net counterparty exposure includes the fair value of derivatives,

including the counterparty risk associated with credit default

swaps (CDS), and secured financing transactions. Derivatives

exposures are presented net of collateral, which is predominantly

cash, pledged under legally enforceable master netting

agreements. Secured financing transaction exposures are

presented net of eligible cash or securities pledged as collateral.

Securities and other investments are carried at fair value and

long securities exposures are netted against short exposures with

the same underlying issuer to, but not below, zero (i.e., negative

issuer exposures are reported as zero). Other investments include

our GPI portfolio and strategic investments.

Net country exposure represents country exposure less hedges

and credit default protection purchased, net of credit default

protection sold. We hedge certain of our country exposures with

credit default protection primarily in the form of single-name, as

well as indexed and tranched CDS. The exposures associated with

these hedges represent the amount that would be realized upon

the isolated default of an individual issuer in the relevant country

assuming a zero recovery rate for that individual issuer, and are

calculated based on the CDS notional amount adjusted for any

fair value receivable or payable. Changes in the assumption of an

isolated default can produce different results in a particular

tranche.

Table 57 Top 20 Non-U.S. Countries Exposure

(Dollars in millions)

Funded Loans

and Loan

Equivalents

Unfunded

Loan

Commitments

Net

Counterparty

Exposure

Securities/

Other

Investments

Country

Exposure at

December 31

2014

Hedges and

Credit Default

Protection

Net Country

Exposure at

December 31

2014

Increase

(Decrease) from

December 31

2013

United Kingdom $ 23,727 $ 11,921 $ 6,373 $ 7,769 $ 49,790 $ (4,243) $45,547 $ 1,961

Canada 6,388 6,847 1,950 5,173 20,358 (1,818) 18,540 129

Japan 12,518 506 3,589 1,453 18,066 (1,332) 16,734 8,619

Brazil 9,923 727 511 4,183 15,344 (360) 14,984 1,352

Germany 5,341 5,840 3,477 1,489 16,147 (3,588) 12,559 (159)

China 10,238 725 556 1,483 13,002 (710) 12,292 (629)

India 5,631 507 496 4,126 10,760 (174) 10,586 335

France 3,246 5,117 1,495 5,038 14,896 (4,458) 10,438 275

Hong Kong 6,413 616 924 691 8,644 (36) 8,608 3,251

Netherlands 2,928 3,392 675 2,275 9,270 (1,135) 8,135 500

Australia 3,237 1,908 826 2,235 8,206 (533) 7,673 (324)

Switzerland 2,493 3,663 1,018 622 7,796 (1,265) 6,531 985

South Korea 3,559 707 534 2,327 7,127 (678) 6,449 14

Italy 2,545 1,596 2,484 1,752 8,377 (2,978) 5,399 197

Mexico 3,038 807 245 566 4,656 (385) 4,271 272

Singapore 1,984 203 673 1,206 4,066 (62) 4,004 175

Taiwan 2,248 — 437 1,180 3,865 — 3,865 (207)

Spain 2,296 994 296 1,022 4,608 (992) 3,616 213

Russia 4,124 80 732 66 5,002 (1,393) 3,609 (3,113)

Turkey 2,695 75 15 185 2,970 (482) 2,488 (205)

Total top 20 non-U.S.

countries exposure $ 114,572 $ 46,231 $ 27,306 $ 44,841 $ 232,950 $ (26,622) $ 206,328 $ 13,641

Russian intervention in Ukraine during 2014 significantly

increased regional geopolitical tensions. The Russian economy is

slowing due to the negative impacts of weak oil prices, ongoing

economic sanctions and high interest rates resulting from Russian

central bank actions taken to counter ruble depreciation. Net

exposure to Russia was reduced to $3.6 billion at December 31,

2014, concentrated in oil and gas companies and commercial

banks. Our exposure to Ukraine at December 31, 2014 was

minimal. In response to Russian actions, U.S. and European

governments have imposed sanctions on a limited number of

Russian individuals and business entities. Geopolitical and

economic conditions remain fluid with potential for further

escalation of tensions, severity of sanctions against Russian

interests, sustained low oil prices and rating agency downgrades.

Certain European countries, including Italy, Spain, Ireland,

Greece and Portugal, have experienced varying degrees of financial

stress in recent years. While market conditions have improved in

Europe, policymakers continue to address fundamental challenges

of competitiveness, growth, deflation and high unemployment. A

return of political stress or financial instability in these countries

could disrupt financial markets and have a detrimental impact on

global economic conditions and sovereign and non-sovereign debt