Bank of America 2014 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

20 Bank of America 2014

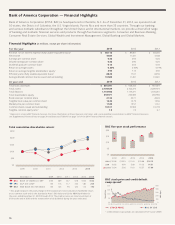

Executive Summary

Business Overview

The Corporation is a Delaware corporation, a bank holding company

(BHC) and a financial holding company. When used in this report,

“the Corporation” may refer to Bank of America Corporation

individually, Bank of America Corporation and its subsidiaries, or

certain of Bank of America Corporation’s subsidiaries or affiliates.

Our principal executive offices are located in Charlotte, North

Carolina. Through our banking and various nonbank subsidiaries

throughout the U.S. and in international markets, we provide a

diversified range of banking and nonbank financial services and

products through five business segments: Consumer & Business

Banking (CBB), Consumer Real Estate Services (CRES), Global

Wealth & Investment Management (GWIM), Global Banking and

Global Markets, with the remaining operations recorded in All Other.

Effective January 1, 2015, to align the segments with how we

manage the businesses in 2015, we changed our basis of segment

presentation as follows: the Home Loans subsegment within CRES

was moved to CBB, and Legacy Assets & Servicing became a

separate segment. Also, a portion of the Business Banking

business, based on the size of the client relationship, was moved

from CBB to Global Banking. Prior periods will be restated to

conform to the new segment alignment. Prior to October 1, 2014,

we operated our banking activities primarily under two charters:

Bank of America, National Association (Bank of America, N.A. or

BANA) and, to a lesser extent, FIA Card Services, National

Association (FIA Card Services, N.A. or FIA). On October 1, 2014,

FIA was merged into BANA. At December 31, 2014, the Corporation

had approximately $2.1 trillion in assets and approximately

224,000 full-time equivalent employees.

As of December 31, 2014, we operated in all 50 states, the

District of Columbia, the U.S. Virgin Islands, Puerto Rico and more

than 35 countries. Our retail banking footprint covers

approximately 80 percent of the U.S. population and we serve

approximately 48 million consumer and small business

relationships with approximately 4,800 banking centers, 15,800

ATMs, nationwide call centers, and leading online and mobile

banking platforms (www.bankofamerica.com). We offer industry-

leading support to approximately three million small business

owners. Our industry leading wealth management and trust

businesses, with client balances of $2.5 trillion, provide tailored

solutions to meet client needs through a full set of brokerage,

banking, trust and retirement products. We are a global leader in

corporate and investment banking and trading across a broad

range of asset classes serving corporations, governments,

institutions and individuals around the world.

2014 Economic and Business Environment

In the U.S., economic growth continued in 2014, ending the year

in the midst of its sixth consecutive year of recovery. After a

tentative and generally soft trajectory for five years where

annualized GDP growth averaged 2.3 percent, there were clear

signs of accelerated growth in the final three quarters of 2014

following a first quarter impacted by adverse weather conditions.

Employment gains picked up during the year, and the

unemployment rate fell to 5.6 percent at year end. Consumption

grew slowly early in the year, before picking up steadily and ending

with a robust pace in the final quarter. Core inflation remained

relatively unchanged in 2014, rising modestly in the first half and

falling thereafter, and ended the year more than half a percentage

point below the Board of Governors of the Federal Reserve

System’s (Federal Reserve) longer-term annual target of two

percent.

U.S. household net worth continued to rise in 2014 but at a

substantially slower pace than 2013. Home price appreciation was

less in 2014 than 2013 but prices still rose approximately five

percent in 2014 while equity markets gained approximately 11

percent. However, consumer spending was more significantly

enhanced by sharply lower oil prices late in the year, reflecting

foreign economic weakness amid an ample and growing energy

supply.

U.S. Treasury yields fell over the course of the year, reversing

much of the previous year’s increase. Declining world inflation and

interest rates helped push U.S. Treasury yields lower even as the

Federal Reserve steadily reduced and finally ended its purchases

of agency mortgage-backed securities (MBS) and long-term U.S.

Treasury securities. The Federal Reserve ended the year amid

indications that it can be patient with regard to normalizing

monetary policy.

Internationally, the eurozone grew modestly for much of the

year, with growth restrained by continued deleveraging of the

financial sector, high unemployment and political uncertainty.

Inflation in the eurozone also fell significantly to near zero by year

end. European bond yields continued to decline, especially as the

European Central Bank eased monetary policy and expectations

grew late in the year for outright purchases of sovereign and/or

corporate securities in 2015, and were subsequently confirmed

to begin in March 2015. The Euro/U.S. Dollar exchange rate also

fell significantly, boosting European competitiveness, particularly

in the second half of 2014, in direct reaction to the differing

directions of U.S. and eurozone monetary policies. Contentious

negotiations between parties to Greek sovereign and bank support

programs added to uncertainty and market volatility in the first

quarter of 2015.

In Russia, the combination of the U.S. and European Union

sanctions and sharply lower oil prices weakened growth. Select

emerging nations that are net energy suppliers also saw growth

diminish sharply, although other nations, including some emerging

economies in Asia received some benefits from declining energy

prices.

Following a quarter of strong economic growth ahead of a

consumption tax increase, Japan contracted through the middle

of the year and the Bank of Japan responded with stepped up

quantitative easing. Amid gradual economic moderation, China

also eased monetary policy late in the year.