Bank of America 2014 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

Bank of America 2014 87

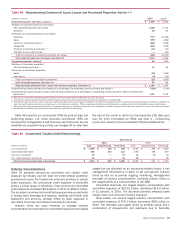

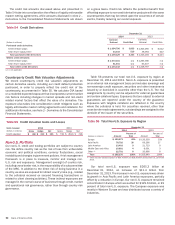

Table 48 Nonperforming Commercial Loans, Leases and Foreclosed Properties Activity (1, 2)

(Dollars in millions) 2014 2013

Nonperforming loans and leases, January 1 $ 1,309 $3,224

Additions to nonperforming loans and leases:

New nonperforming loans and leases 1,228 1,112

Advances 48 30

Reductions to nonperforming loans and leases:

Paydowns (717)(1,342)

Sales (149)(498)

Returns to performing status (3) (261)(588)

Charge-offs (332)(549)

Transfers to foreclosed properties (4) (13) (54)

Transfers to loans held-for-sale —(26)

Total net reductions to nonperforming loans and leases (196)(1,915)

Total nonperforming loans and leases, December 31 1,113 1,309

Foreclosed properties, January 1 90 250

Additions to foreclosed properties:

New foreclosed properties (4) 11 38

Reductions to foreclosed properties:

Sales (26) (169)

Write-downs (8)(29)

Total net reductions to foreclosed properties (23) (160)

Total foreclosed properties, December 31 67 90

Nonperforming commercial loans, leases and foreclosed properties, December 31 $ 1,180 $1,399

Nonperforming commercial loans and leases as a percentage of outstanding commercial loans and leases (5) 0.29%0.34%

Nonperforming commercial loans, leases and foreclosed properties as a percentage of outstanding commercial loans, leases and foreclosed

properties (5) 0.31 0.36

(1) Balances do not include nonperforming LHFS of $212 million and $296 million at December 31, 2014 and 2013.

(2) Includes U.S. small business commercial activity. Small business card loans are excluded as they are not classified as nonperforming.

(3) Commercial loans and leases may be returned to performing status when all principal and interest is current and full repayment of the remaining contractual principal and interest is expected, or

when the loan otherwise becomes well-secured and is in the process of collection. TDRs are generally classified as performing after a sustained period of demonstrated payment performance.

(4) New foreclosed properties represents transfers of nonperforming loans to foreclosed properties net of charge-offs recorded during the first 90 days after transfer of a loan to foreclosed properties.

(5) Outstanding commercial loans exclude loans accounted for under the fair value option.

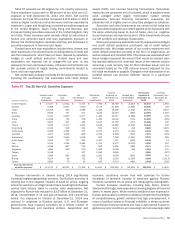

Table 49 presents our commercial TDRs by product type and

performing status. U.S. small business commercial TDRs are

comprised of renegotiated small business card loans and are not

classified as nonperforming as they are charged off no later than

the end of the month in which the loan becomes 180 days past

due. For more information on TDRs, see Note 4 – Outstanding

Loans and Leases to the Consolidated Financial Statements.

Table 49 Commercial Troubled Debt Restructurings

December 31

2014 2013

(Dollars in millions) Total Nonperforming Performing Total Nonperforming Performing

U.S. commercial $ 1,096 $ 308 $788 $ 1,318 $ 298 $ 1,020

Commercial real estate 456 234 222 835 198 637

Non-U.S. commercial 43 — 43 48 38 10

U.S. small business commercial 35 — 35 88 — 88

Total commercial troubled debt restructurings $ 1,630 $ 542 $ 1,088 $ 2,289 $ 534 $ 1,755

Industry Concentrations

Table 50 presents commercial committed and utilized credit

exposure by industry and the total net credit default protection

purchased to cover the funded and unfunded portions of certain

credit exposures. Our commercial credit exposure is diversified

across a broad range of industries. Total commercial committed

credit exposure increased $8.6 billion in 2014 to $832.4 billion.

The increase in commercial committed exposure was concentrated

in energy, food, beverage and tobacco, retailing, and health care

equipment and services, partially offset by lower exposure in

diversified financials and telecommunications services.

Industry limits are used internally to manage industry

concentrations and are based on committed exposures and capital

usage that are allocated on an industry-by-industry basis. A risk

management framework is in place to set and approve industry

limits as well as to provide ongoing monitoring. Management

oversight of industry concentrations, including industry limits, is

the responsibility of a subcommittee of the MRC.

Diversified financials, our largest industry concentration with

committed exposure of $103.5 billion, decreased $14.6 billion,

or 12 percent, in 2014. The decrease primarily reflected lower

margin loans and consumer finance exposure.

Real estate, our second largest industry concentration with

committed exposure of $76.2 billion, decreased $265 million in

2014. The decrease was largely driven by portfolio sales, and a

combination of prepayments and paydowns due to favorable