Bank of America 2014 Annual Report Download - page 4

Download and view the complete annual report

Please find page 4 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

2

$152 7.5%

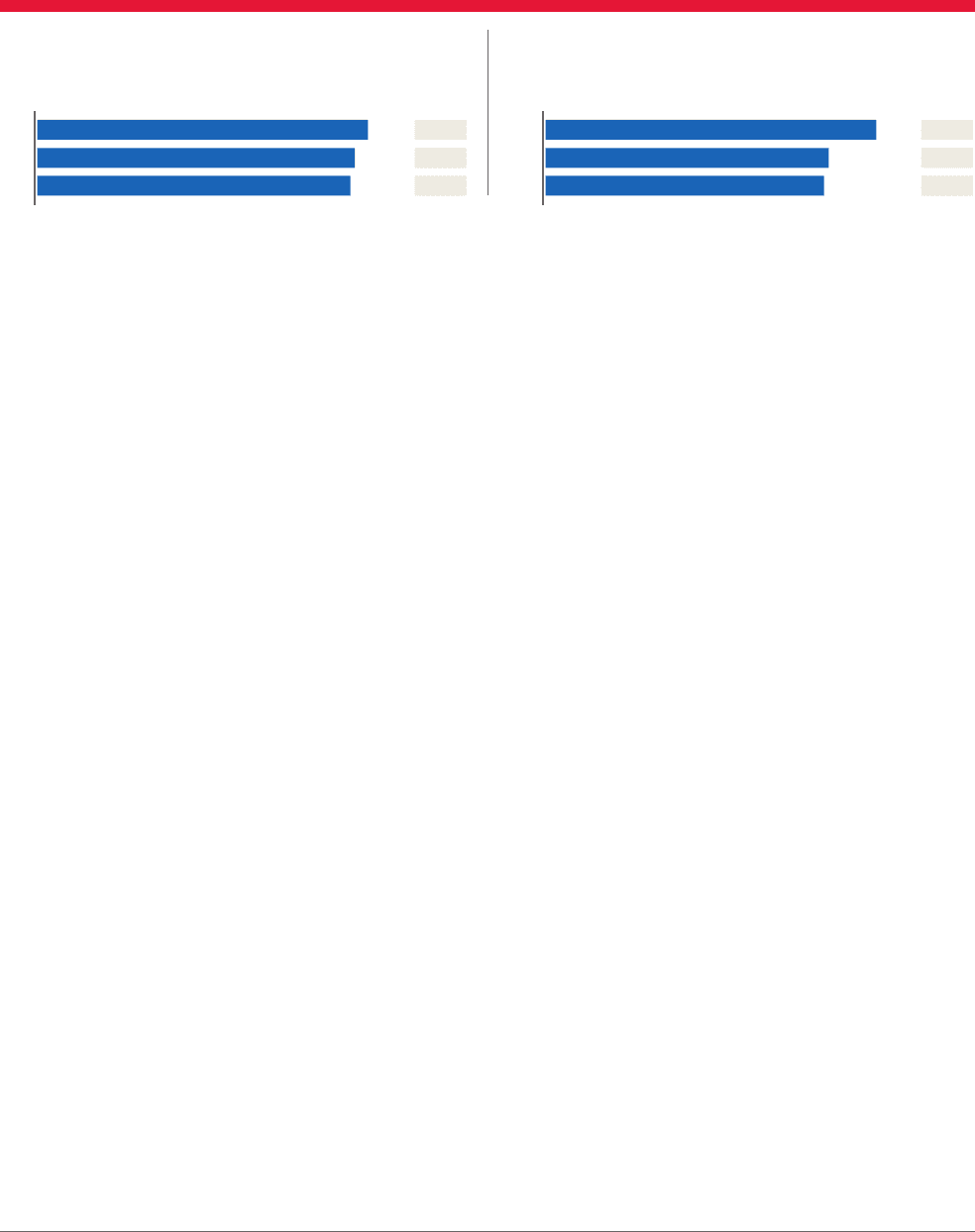

7.2%

6.7%$144

$146

2012

2013

2014

Ratio

$439 39

38

$372

$376

4Q14

4Q13

4Q12 33

Months

their goods to overseas markets. Others are accessing more

markets for their American-made products. Serving these

increasingly global small- and medium-sized companies takes

global capabilities — cash management or, with our sales and

trading capabilities, helping these companies protect against

currency fluctuations and counter-party risk.

Our approach to serving these companies is the same as our

approach to the individuals we serve — connect all of our capabilities

to help them achieve their goals. Being able to do that globally

puts our company at a competitive advantage with these clients.

Our businesses that serve these clients provide great earnings

stability to you as shareholders as we use our balance sheet

to help clients prosper and benefit the economies in which

they operate. Lending and cash management services provide

strong returns. Our Global Markets capabilities also serve

these clients by helping them raise capital efficiently and

effectively, in the U.S. and around the world. As I’ll discuss,

we have sized our capital markets capabilities to serve clients,

not to take outsized proprietary trading positions. Those

capabilities provide direct benefit to companies of all sizes,

helping them access markets and grow. This is an efficient

method of contributing to global economic growth.

We also continue to invest and help business clients by

offering the best means of managing their capital and making

it easier for them to transact with their own customers. With

our CashPro® Online payment application, we have created a

better, more efficient experience for our clients and lowered

our own costs by retiring aging payment technology. This is

just one example of the focus we have to be simpler and to

drive operational excellence. The results of these investments

are seen in many ways, including recognition by Global Finance

magazine as “Best Bank for Cash Management” in North

America for the fih consecutive year.

Our integrated approach makes it more convenient for business

clients to do more with us. In the work we do for our larger

Global Corporate and Investment Banking clients, our teams

advised on three of the top five global mergers in 2014. Other

indications of greater activity with these clients are seen in

higher average loan balances, which increased $13 billion last

year to $270 billion, and higher average deposit balances,

which grew $25 billion last year to $261 billion.

Also, we are doing more for our business clients through

our Merrill Lynch and U.S. Trust teammates working with

our commercial bankers. For example, the number of funded

institutional retirement plans purchased by companies we

serve grew by 53 percent last year, generating assets of nearly

$9 billion. In addition, we have had thousands of commercial

and corporate clients bring their private assets into our

Global Wealth and Investment Management businesses.

Our teams serving business clients are collaborating across

our franchise to deliver all of our industry-leading products

and services. As I said above, this work is just beginning.

Balanced Global Markets capabilities serving

institutional investors

Alongside the progress we are making in serving individuals

and companies, our third group of clients — institutional

investors — continues to benefit from the investment we

are making in our sales and trading team and in our research

platform of 700 analysts. For the fourth consecutive year,

Bank of America Merrill Lynch was ranked the No. 1 research

firm in the world by Institutional Investor magazine.

We have reduced risk in Global Markets sales and trading

operations over the past several years. At the time of the

Bank of America merger with Merrill Lynch, the markets

business had assets of nearly $1 trillion; and at the end of

the year we were below $600 billion. All measures of risk in

the business were low in 2014 and down significantly from a

few years ago. Our mix of activities has changed, too. Most

importantly, our focus is on enabling our investor clients to

provide the capital and liquidity to companies and markets

around the world, not taking our own trading positions.

We do this by serving as the intermediary between our “issuer”

clients (companies issuing debt or equity) and our investor

clients (pension and retirement funds, for example) looking for

growth and overall returns. We also see synergy with our wealth

management clients in the research we provide to help them

make investment decisions. These industry-leading platforms —

providing ideas and analysis for investors, executing transactions

in markets around the world, and helping companies raise

capital and grow — drive the real economy in the U.S. and

globally. All the while, the team continues to reduce risk, simplify

the business, and produce higher-quality revenue and profits.

Our goal is simple: We do not need to be the largest in the

business, but we want to be the best for the clients we serve.

Tangible common equity ($B)1Global excess liquidity sources

and time-to-required funding ($B)2

1 Represents a non-GAAP financial measure. Common shareholders’ equity was $224B,

$221B and $219B at December 31, 2014, 2013 and 2012, respectively. Common share-

holders’ equity ratio was 10.7%, 10.4% and 9.9% at December 31, 2014, 2013 and 2012,

respectively.

2 Global Excess Liquidity Sources include cash and high-quality, liquid, unencumbered

securities, limited to U.S. government and agency securities, U.S. agency mortgage-

backed securities, and a select group of non-U.S. government and supranational

securities, and are readily available to meet funding requirements as they arise. It does

not include Federal Reserve Discount Window or Federal Home Loan Bank borrowing

capacity. Transfers of liquidity from the bank or other regulated entities are subject to

certain regulatory restrictions.