Bank of America 2014 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

Bank of America 2014 75

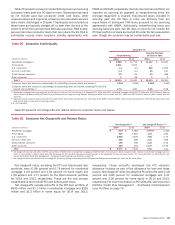

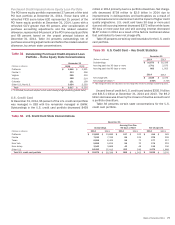

Table 31 presents outstandings, nonperforming balances and

net charge-offs by certain state concentrations for the home equity

portfolio. In the New York area, the New York-Northern New Jersey-

Long Island MSA made up 12 percent of the outstanding home

equity portfolio at both December 31, 2014 and 2013. Loans

within this MSA contributed 14 percent and nine percent of net

charge-offs in 2014 and 2013 within the home equity portfolio.

The Los Angeles-Long Beach-Santa Ana MSA within California

made up 12 percent of the outstanding home equity portfolio at

both December 31, 2014 and 2013. Loans within this MSA

contributed four percent and nine percent of net charge-offs in

2014 and 2013 within the home equity portfolio.

Table 31 Home Equity State Concentrations

December 31

Outstandings (1) Nonperforming (1) Net Charge-offs (2)

(Dollars in millions) 2014 2013 2014 2013 2014 2013

California $ 23,250 $ 25,061 $ 1,012 $ 1,047 $118 $ 509

Florida (3) 9,633 10,604 574 643 170 315

New Jersey (3) 5,883 6,153 299 304 68 93

New York (3) 5,671 6,035 387 405 81 110

Massachusetts 3,655 3,881 148 144 30 42

Other U.S./Non-U.S. 32,016 35,345 1,481 1,532 440 734

Home equity loans (4) $ 80,108 $ 87,079 $ 3,901 $ 4,075 $907 $ 1,803

Purchased credit-impaired home equity portfolio 5,617 6,593

Total home equity loan portfolio $ 85,725 $ 93,672

(1) Outstandings and nonperforming amounts exclude loans accounted for under the fair value option. There were $196 million and $147 million of home equity loans accounted for under the fair value

option at December 31, 2014 and 2013. For more information on the fair value option, see Consumer Portfolio Credit Risk Management – Consumer Loans Accounted for Under the Fair Value Option

on page 79 and Note 21 – Fair Value Option to the Consolidated Financial Statements.

(2) Net charge-offs exclude $265 million of write-offs in the home equity PCI loan portfolio in 2014 compared to $1.2 billion in 2013. These write-offs decreased the PCI valuation allowance included

as part of the allowance for loan and lease losses. For more information on PCI write-offs, see Consumer Portfolio Credit Risk Management – Purchased Credit-impaired Loan Portfolio on page 75.

(3) In these states, foreclosure requires a court order following a legal proceeding (judicial states).

(4) Amount excludes the PCI home equity portfolio.

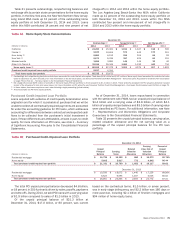

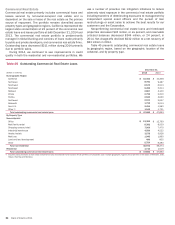

Purchased Credit-impaired Loan Portfolio

Loans acquired with evidence of credit quality deterioration since

origination and for which it is probable at purchase that we will be

unable to collect all contractually required payments are accounted

for under the accounting guidance for PCI loans, which addresses

accounting for differences between contractual and expected cash

flows to be collected from the purchaser’s initial investment in

loans if those differences are attributable, at least in part, to credit

quality. For more information on PCI loans, see Note 1 – Summary

of Significant Accounting Principles to the Consolidated Financial

Statements.

As of December 31, 2014, loans repurchased in connection

with the settlement with FNMA had an unpaid principal balance of

$4.4 billion and a carrying value of $3.8 billion, of which $4.1

billion of unpaid principal balance and $3.5 billion of carrying value

were classified as PCI loans. For additional information, see Note

7 – Representations and Warranties Obligations and Corporate

Guarantees to the Consolidated Financial Statements.

Table 32 presents the unpaid principal balance, carrying value,

related valuation allowance and the net carrying value as a

percentage of the unpaid principal balance for the PCI loan

portfolio.

Table 32 Purchased Credit-impaired Loan Portfolio

December 31, 2014

(Dollars in millions)

Unpaid

Principal

Balance

Carrying

Value

Related

Valuation

Allowance

Carrying

Value Net of

Valuation

Allowance

Percent of

Unpaid

Principal

Balance

Residential mortgage $ 15,726 $ 15,152 $ 880 $14,272 90.75%

Home equity 5,605 5,617 772 4,845 86.44

Total purchased credit-impaired loan portfolio $ 21,331 $ 20,769 $ 1,652 $ 19,117 89.62

December 31, 2013

Residential mortgage $ 19,558 $ 18,672 $ 1,446 $ 17,226 88.08%

Home equity 6,523 6,593 1,047 5,546 85.02

Total purchased credit-impaired loan portfolio $ 26,081 $ 25,265 $ 2,493 $ 22,772 87.31

The total PCI unpaid principal balance decreased $4.8 billion,

or 18 percent, in 2014 primarily driven by sales, payoffs, paydowns

and write-offs. During 2014, we sold PCI loans with a carrying value

of $1.9 billion compared to sales of $1.3 billion in 2013.

Of the unpaid principal balance of $21.3 billion at

December 31, 2014, $17.0 billion, or 80 percent, was current

based on the contractual terms, $1.5 billion, or seven percent,

was in early stage delinquency, and $2.2 billion was 180 days or

more past due, including $2.1 billion of first-lien mortgages and

$94 million of home equity loans.