Bank of America 2014 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

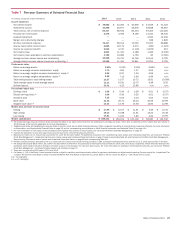

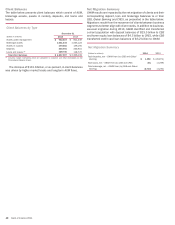

36 Bank of America 2014

noninterest expense decreased $4.0 billion to $8.0 billion driven

by a decline in default-related servicing expenses, including

mortgage-related assessments, waivers and similar costs related

to foreclosure delays in Legacy Assets & Servicing and a decline

in personnel expense resulting from lower loan originations in

Home Loans.

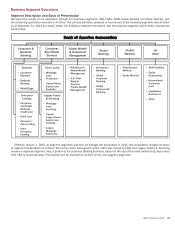

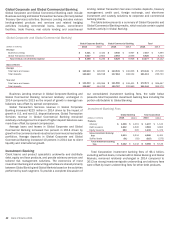

Home Loans

Home Loans products are available to our customers through our

retail network, direct telephone and online access delivered by a

sales force of nearly 2,500 mortgage loan officers, including 1,500

banking center mortgage loan officers covering 2,600 banking

centers, and a nearly 700-person centralized sales force based in

five call centers.

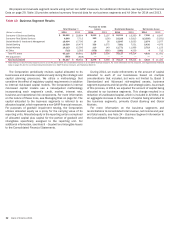

The net loss for Home Loans increased $155 million to a net

loss of $283 million driven by lower mortgage banking income,

partially offset by lower noninterest expense and lower provision

for credit losses. Mortgage banking income decreased $1.1 billion

due to a decline in core production revenue as a result of lower

first mortgage origination volumes, and to a lesser extent, industry-

wide margin compression. The provision for credit losses

decreased $94 million reflecting continued improvement in

portfolio trends including increased home prices. Noninterest

expense decreased $747 million primarily due to lower personnel

expense resulting from lower loan originations.

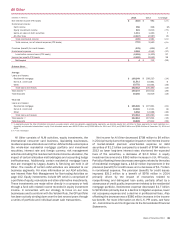

Legacy Assets & Servicing

Legacy Assets & Servicing is responsible for all of our in-house

servicing activities related to the residential mortgage and home

equity loan portfolios, including owned loans and loans serviced

for others (collectively, the mortgage serviced portfolio). A portion

of this portfolio has been designated as the Legacy Serviced

Portfolio, which represented 26 percent, 30 percent and 39

percent of the total mortgage serviced portfolio, as measured by

unpaid principal balance, at December 31, 2014, 2013 and 2012,

respectively. In addition, Legacy Assets & Servicing is responsible

for managing subservicing agreements.

Legacy Assets & Servicing results reflect the net cost of legacy

exposures that are included in the results of CRES, including

representations and warranties provision, litigation expense,

financial results of the CRES home equity portfolio selected as

part of the Legacy Owned Portfolio, the financial results of the

servicing operations and the results of MSR activities, including

net hedge results. The financial results of the servicing operations

reflect certain revenues and expenses on loans serviced for

others, including owned loans serviced for Home Loans, GWIM

and All Other.

Servicing activities include collecting cash for principal,

interest and escrow payments from borrowers, disbursing

customer draws for lines of credit, accounting for and remitting

principal and interest payments to investors and escrow payments

to third parties, and responding to customer inquiries. Our home

retention efforts, including single point of contact resources, are

also part of our servicing activities, along with supervision of

foreclosures and property dispositions. Prior to foreclosure,

Legacy Assets & Servicing evaluates various workout options in

an effort to help our customers avoid foreclosure. For more

information on our servicing activities, including the impact of

foreclosure delays, see Off-Balance Sheet Arrangements and

Contractual Obligations – Servicing, Foreclosure and Other

Mortgage Matters on page 50.

The net loss for Legacy Assets & Servicing increased $8.2

billion to a net loss of $13.1 billion driven by higher litigation

expense, which is included in noninterest expense, a lower tax

benefit rate resulting from the non-deductible treatment of a

portion of the settlement with the DoJ, lower mortgage banking

income and higher provision for credit losses.

Mortgage banking income decreased $1.6 billion primarily

driven by a decline in servicing income due to a smaller servicing

portfolio combined with less favorable MSR net-of-hedge

performance. The provision for credit losses increased $410

million primarily due to additional costs associated with the

consumer relief portion of the settlement with the DoJ.

Noninterest expense increased $8.2 billion due to higher

litigation expense as a result of the settlements with the DoJ and

FHFA. Excluding litigation, noninterest expense decreased $3.3

billion to $5.4 billion driven by a decrease in default-related

servicing expenses, including mortgage-related assessments,

waivers and similar costs related to foreclosure delays. We expect

that noninterest expense in Legacy Assets & Servicing, excluding

litigation expense, will decline to approximately $800 million per

quarter by the end of 2015.

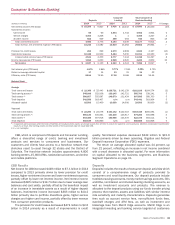

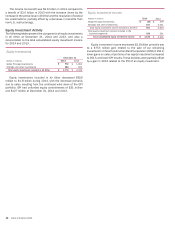

Legacy Portfolios

The Legacy Portfolios (both owned and serviced) include those

loans originated prior to January 1, 2011 that would not have been

originated under our established underwriting standards in place

as of December 31, 2010. The purchased credit-impaired (PCI)

portfolio, as well as certain loans that met a pre-defined

delinquency status or probability of default threshold as of January

1, 2011, are also included in the Legacy Portfolios. Since

determining the pool of loans to be included in the Legacy Portfolios

as of January 1, 2011, the criteria have not changed for these

portfolios, but will continue to be evaluated over time.

Legacy Owned Portfolio

The Legacy Owned Portfolio includes those loans that met the

criteria as described above and are on the balance sheet of the

Corporation. The home equity loan portfolio is held on the balance

sheet of Legacy Assets & Servicing, and the residential mortgage

loan portfolio is held on the balance sheet of All Other. The financial

results of the on-balance sheet loans are reported in the segment

that owns the loans or in All Other. Total loans in the Legacy Owned

Portfolio decreased $22.2 billion in 2014 to $89.9 billion at

December 31, 2014, of which $33.1 billion were held on the

Legacy Assets & Servicing balance sheet and the remainder was

held on the balance sheet of All Other. The decrease was primarily

related to paydowns, loan sales, PCI write-offs and charge-offs.