Bank of America 2014 Annual Report Download - page 179

Download and view the complete annual report

Please find page 179 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

Bank of America 2014 177

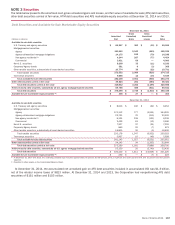

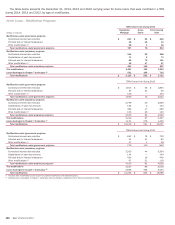

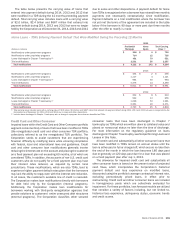

Impaired Loans and Troubled Debt Restructurings

A loan is considered impaired when, based on current information,

it is probable that the Corporation will be unable to collect all

amounts due from the borrower in accordance with the contractual

terms of the loan. Impaired loans include nonperforming

commercial loans and all consumer and commercial TDRs.

Impaired loans exclude nonperforming consumer loans and

nonperforming commercial leases unless they are classified as

TDRs. Loans accounted for under the fair value option are also

excluded. PCI loans are excluded and reported separately on page

186. For additional information, see Note 1 – Summary of

Significant Accounting Principles.

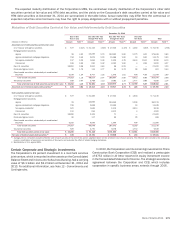

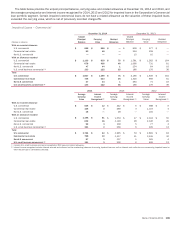

Home Loans

Impaired home loans within the Home Loans portfolio segment

consist entirely of TDRs. Excluding PCI loans, most modifications

of home loans meet the definition of TDRs when a binding offer

is extended to a borrower. Modifications of home loans are done

in accordance with the government’s Making Home Affordable

Program (modifications under government programs) or the

Corporation’s proprietary programs (modifications under

proprietary programs). These modifications are considered to be

TDRs if concessions have been granted to borrowers experiencing

financial difficulties. Concessions may include reductions in

interest rates, capitalization of past due amounts, principal and/

or interest forbearance, payment extensions, principal and/or

interest forgiveness, or combinations thereof. During 2013 and

2012, the Corporation provided interest rate modifications to

qualified borrowers pursuant to the 2012 National Mortgage

Settlement and these interest rate modifications are not

considered to be TDRs.

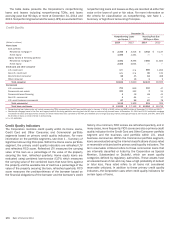

Prior to permanently modifying a loan, the Corporation may

enter into trial modifications with certain borrowers under both

government and proprietary programs. Trial modifications generally

represent a three- to four-month period during which the borrower

makes monthly payments under the anticipated modified payment

terms. Upon successful completion of the trial period, the

Corporation and the borrower enter into a permanent modification.

Binding trial modifications are classified as TDRs when the trial

offer is made and continue to be classified as TDRs regardless of

whether the borrower enters into a permanent modification.

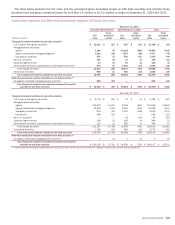

Home loans that have been discharged in Chapter 7 bankruptcy

with no change in repayment terms of $2.4 billion were included

in TDRs at December 31, 2014, of which $1.4 billion were

classified as nonperforming and $1.0 billion were loans fully-

insured by the Federal Housing Administration (FHA). For more

information on loans discharged in Chapter 7 bankruptcy, see

Nonperforming Loans and Leases in this Note.

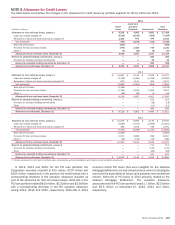

A home loan, excluding PCI loans which are reported separately,

is not classified as impaired unless it is a TDR. Once such a loan

has been designated as a TDR, it is then individually assessed for

impairment. Home loan TDRs are measured primarily based on

the net present value of the estimated cash flows discounted at

the loan’s original effective interest rate, as discussed in the

following paragraph. If the carrying value of a TDR exceeds this

amount, a specific allowance is recorded as a component of the

allowance for loan and lease losses. Alternatively, home loan TDRs

that are considered to be dependent solely on the collateral for

repayment (e.g., due to the lack of income verification or as a

result of being discharged in Chapter 7 bankruptcy) are measured

based on the estimated fair value of the collateral and a charge-

off is recorded if the carrying value exceeds the fair value of the

collateral. Home loans that reached 180 days past due prior to

modification had been charged off to their net realizable value,

less costs to sell, before they were modified as TDRs in accordance

with established policy. Therefore, modifications of home loans

that are 180 or more days past due as TDRs do not have an impact

on the allowance for loan and lease losses nor are additional

charge-offs required at the time of modification. Subsequent

declines in the fair value of the collateral after a loan has reached

180 days past due are recorded as charge-offs. Fully-insured loans

are protected against principal loss, and therefore, the Corporation

does not record an allowance for loan and lease losses on the

outstanding principal balance, even after they have been modified

in a TDR.

The net present value of the estimated cash flows used to

measure impairment is based on model-driven estimates of

projected payments, prepayments, defaults and loss-given-default

(LGD). Using statistical modeling methodologies, the Corporation

estimates the probability that a loan will default prior to maturity

based on the attributes of each loan. The factors that are most

relevant to the probability of default are the refreshed LTV, or in

the case of a subordinated lien, refreshed CLTV, borrower credit

score, months since origination (i.e., vintage) and geography. Each

of these factors is further broken down by present collection status

(whether the loan is current, delinquent, in default or in

bankruptcy). Severity (or LGD) is estimated based on the refreshed

LTV for first mortgages or CLTV for subordinated liens. The

estimates are based on the Corporation’s historical experience as

adjusted to reflect an assessment of environmental factors that

may not be reflected in the historical data, such as changes in

real estate values, local and national economies, underwriting

standards and the regulatory environment. The probability of

default models also incorporate recent experience with

modification programs including redefaults subsequent to

modification, a loan’s default history prior to modification and the

change in borrower payments post-modification.

At December 31, 2014 and 2013, remaining commitments to

lend additional funds to debtors whose terms have been modified

in a home loan TDR were immaterial. Home loan foreclosed

properties totaled $630 million and $533 million at December 31,

2014 and 2013.