Bank of America 2014 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

Bank of America 2014 57

Basel 3

Basel 3 materially changes Tier 1 and Total capital calculations

and formally establishes a Common equity tier 1 capital ratio.

Basel 3 introduces new minimum capital ratios and buffer

requirements and a supplementary leverage ratio (SLR); changes

the composition of regulatory capital; and revises the adequately

capitalized minimum requirements under the Prompt Corrective

Action (PCA) framework. Changes to the composition of regulatory

capital under Basel 3, as compared to the Basel 1 – 2013 Rules,

are subject to a transition period as described below. The new

minimum capital ratio requirements and related buffers will be

phased in from January 1, 2014 through January 1, 2019. For

more information on the SLR, see Capital Management – Other

Regulatory Capital Matters on page 61.

As an advanced approaches bank, under Basel 3, we are

required to complete a qualification period (parallel run) to

demonstrate compliance with the final Basel 3 rules to the

satisfaction of U.S. banking regulators. Upon notification of

approval by U.S. banking regulators to exit our parallel run, we will

be required to calculate regulatory capital ratios and risk-weighted

assets under both the Standardized and Advanced approaches.

The approach that yields the lower ratio is to be used to assess

capital adequacy including under the PCA framework. Prior to

receipt of notification of approval, we are required to assess our

capital adequacy under the Standardized approach only.

Effective January 1, 2015, the PCA framework was amended

to reflect the new capital requirements under Basel 3. The PCA

framework establishes categories of capitalization, including “well

capitalized,” based on regulatory ratio requirements. U.S. banking

regulators are required to take certain mandatory actions

depending on the category of capitalization, with no mandatory

actions required for “well capitalized” banking organizations.

Effective January 1, 2015, Common equity tier 1 capital is included

in the measurement of “well capitalized.”

Regulatory Capital Composition – Transition

Important differences in determining the composition of regulatory

capital between the Basel 1 – 2013 Rules and Basel 3 include

changes in capital deductions related to our MSRs, deferred tax

assets and defined benefit pension assets, and the inclusion of

unrealized gains and losses on AFS debt and certain marketable

equity securities recorded in accumulated OCI. These changes will

be impacted by, among other things, future changes in interest

rates, overall earnings performance and corporate actions.

Changes to the composition of regulatory capital under Basel 3,

as compared to the Basel 1 – 2013 Rules, are recognized in 20

percent annual increments, and will be fully recognized as of

January 1, 2018. When presented on a fully phased-in basis,

capital, risk-weighted assets and the capital ratios assume all

regulatory capital adjustments and deductions are fully

recognized.

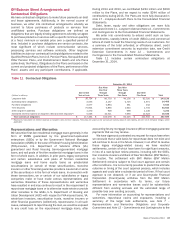

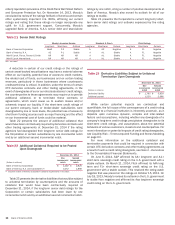

Table 13 summarizes how certain regulatory capital deductions

and adjustments have been or will be transitioned from 2014

through 2018 for Common equity tier 1 and Tier 1 capital.

Table 13 Summary of Certain Basel 3 Regulatory Capital Transition Provisions

Beginning on January 1 of each year 2014 2015 2016 2017 2018

Common equity tier 1 capital

Percent of total amount deducted from Common equity tier 1 capital includes: 20% 40% 60% 80% 100%

Deferred tax assets arising from net operating loss and tax credit carryforwards; intangibles, other than mortgage servicing rights and goodwill; defined benefit pension

fund net assets; net unrealized cumulative gains (losses) related to changes in own credit risk on liabilities, including derivatives, measured at fair value; direct and

indirect investments in own Common equity tier 1 capital instruments; certain amounts exceeding the threshold by 10 percent individually and 15 percent in aggregate

Percent of total amount used to adjust Common equity tier 1 capital includes (1): 80% 60% 40% 20% 0%

Net unrealized gains (losses) on AFS debt and certain marketable equity securities recorded in accumulated OCI; employee benefit plan adjustments recorded in

accumulated OCI

Tier 1 capital

Percent of total amount deducted from Tier 1 capital includes: 80% 60% 40% 20% 0%

Deferred tax assets arising from net operating loss and tax credit carryforwards; defined benefit pension fund net assets; net unrealized cumulative gains (losses)

related to changes in own credit risk on liabilities, including derivatives, measured at fair value

(1) Represents the phase-out percentage of the exclusion by year (e.g., 20 percent of net unrealized gains (losses) on AFS debt and certain marketable equity securities recorded in accumulated OCI

will be included in 2014).

Additionally, Basel 3 revised the regulatory capital treatment

for Trust Securities, requiring them to be partially transitioned from

Tier 1 capital into Tier 2 capital in 2014 and 2015, until fully

excluded from Tier 1 capital in 2016, and partially transitioned

from Tier 2 capital beginning in 2016 with the full amount excluded

in 2022. As of December 31, 2014, our qualifying Trust Securities

were $2.9 billion (approximately 23 bps of the Tier 1 capital ratio).

Standardized Approach

Under the Basel 3 Standardized approach, exposures subject to

market risk are measured on a basis generally consistent with

how market risk-weighted assets were measured under the Basel

1 – 2013 Rules. Credit risk-weighted assets are measured by

applying fixed risk weights to each exposure, determined based

on the characteristics of the exposure, such as type of obligor,

Organization for Economic Cooperation and Development (OECD)

country risk code and maturity, among others. Under the

Standardized approach, no distinction is made for variations in

credit quality for corporate exposures, and the economic benefit

of collateral is restricted to a limited list of eligible securities and

cash. We estimate our Common equity tier 1 capital ratio under

the Basel 3 Standardized approach, on a fully phased-in basis,

would have been 10.0 percent at December 31, 2014. As of

December 31, 2014, we estimate that our Basel 3 Standardized

Common equity tier 1 capital would have been $141.2 billion and

total risk-weighted assets would have been $1,415 billion, on a

fully phased-in basis. For a reconciliation of Basel 3 Standardized

– Transition to Basel 3 Standardized estimates on a fully phased-

in basis for Common equity tier 1 capital and risk-weighted assets,

see Table 16. Our estimates under the Basel 3 Standardized

approach may be refined over time as a result of further rulemaking