Bank of America 2014 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2014 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

100 Bank of America 2014

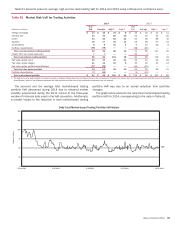

Additional VaR statistics produced within the Corporation’s

single VaR model are provided in Table 62 at the same level of

detail as in Table 61. Evaluating VaR with additional statistics

allows for an increased understanding of the risks in the portfolio

as the historical market data used in the VaR calculation does not

necessarily follow a predefined statistical distribution. Table 62

presents average trading VaR statistics for 99 percent and 95

percent confidence levels for 2014 and 2013.

Table 62 Average Market Risk VaR for Trading Activities – 99 percent and 95 percent VaR Statistics

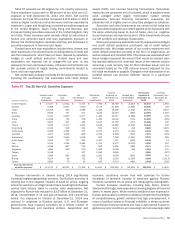

2014 2013

(Dollars in millions) 99 percent 95 percent 99 percent 95 percent

Foreign exchange $16$ 9

$19$ 12

Interest rate 34 21 32 19

Credit 52 26 58 33

Equities 17 9 28 15

Commodities 84

13 8

Portfolio diversification (78) (43) (85) (51)

Total covered positions trading portfolio 49 26 65 36

Impact from less liquid exposures 7343

Total market-based trading portfolio 56 29 69 39

Fair value option loans 31 15 42 21

Fair value option hedges 14 9 19 13

Fair value option portfolio diversification (24) (14) (32) (19)

Total fair value option portfolio 21 10 29 15

Portfolio diversification (12) (8)(13) (9)

Total market-based portfolio $65$31 $85$ 45

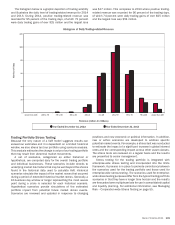

Backtesting

The accuracy of the VaR methodology is evaluated by backtesting,

which compares the daily VaR results, utilizing a one-day holding

period, against a comparable subset of trading revenue. A

backtesting excess occurs when a trading loss exceeds the VaR

for the corresponding day. These excesses are evaluated to

understand the positions and market moves that produced the

trading loss and to ensure that the VaR methodology accurately

represents those losses. As our primary VaR statistic used for

backtesting is based on a 99 percent confidence level and a one-

day holding period, we expect one trading loss in excess of VaR

every 100 days, or between two to three trading losses in excess

of VaR over the course of a year. The number of backtesting

excesses observed can differ from the statistically expected

number of excesses if the current level of market volatility is

materially different than the level of market volatility that existed

during the three years of historical data used in the VaR calculation.

We conduct daily backtesting on our portfolios, ranging from

the total market-based portfolio to individual trading areas.

Additionally, we conduct daily backtesting on our regulatory VaR

results as well as the VaR results for key legal entities, regions

and risk factors. These results are reported to senior market risk

management. Senior management regularly reviews and evaluates

the results of these tests.

The trading revenue used for backtesting is defined by

regulatory agencies in order to most closely align with the VaR

component of the regulatory capital calculation. This revenue

differs from total trading-related revenue in that it excludes revenue

from trading activities that either do not generate market risk or

the market risk cannot be included in VaR. Some examples of the

types of revenue excluded for backtesting are fees, commissions,

reserves, net interest income and intraday trading revenues. In

addition, CVA is not included in the VaR component of the regulatory

capital calculation and is therefore not included in the revenue

used for backtesting of the regulatory VaR results.

During 2014, there were no days in which there was a

backtesting excess for our total market-based portfolio, utilizing a

one-day holding period. There were three backtesting excesses for

our regulatory VaR results, utilizing a one-day holding period, due

to increased volatility during the three months ended

December 31, 2014.

Total Trading Revenue

Total trading-related revenue, excluding brokerage fees, represents

the total amount earned from trading positions, including market-

based net interest income, which are taken in a diverse range of

financial instruments and markets. Trading account assets and

liabilities are reported at fair value. For more information on fair

value, see Note 20 – Fair Value Measurements to the Consolidated

Financial Statements. Trading-related revenues can be volatile and

are largely driven by general market conditions and customer

demand. Also, trading-related revenues are dependent on the

volume and type of transactions, the level of risk assumed, and

the volatility of price and rate movements at any given time within

the ever-changing market environment. Significant daily revenues

by business are monitored and the primary drivers of these are

reviewed. When it is deemed material, an explanation of these

revenues is provided to the GM subcommittee.