Bank of America 2013 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2013 107

To enhance the visibility of the market risks to which we are

exposed, additional VaR statistics produced within the

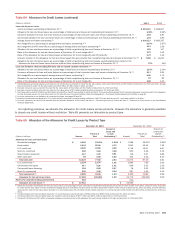

Corporation’s single VaR model are provided in Table 67. Evaluating

VaR with additional statistics allows for an increased

understanding of the risks in the portfolio as the historical market

data used in the VaR calculation does not necessarily follow a

predefined statistical distribution. Table 67 presents average

trading VaR statistics for 99 percent and 95 percent confidence

intervals for 2013 and 2012.

Table 67 Average Market Risk VaR for Trading Activities – Additional VaR Statistics

2013 2012

(Dollars in millions) 99 percent 95 percent 99 percent 95 percent (1)

Foreign exchange $20$13 $21$ 12

Interest rate 34 20 46 26

Credit 53 23 50 24

Real estate/mortgage 28 17 34 18

Equities 29 16 28 16

Commodities 12 7 13 7

Portfolio diversification (107) (63) (117) (65)

Total market-based trading portfolio $69$33 $75$ 38

(1) Due to system constraints, the 95 percent VaR for the three months ended March 31, 2012 is not available and therefore average 95 percent VaR for that period has been estimated. It is not

expected that this estimation materially affected the average 95 percent VaR for 2012.

Limits on quantitative risk measures, including VaR, are

monitored on a daily basis. The trading limits are independently

set by market risk management and reviewed on a regular basis

to ensure they remain relevant and within our overall risk appetite

for market risks. Limits are reviewed in the context of market

liquidity, volatility and strategic business priorities. The limits are

set at both a granular level to ensure extensive coverage of risks

as well as at aggregated portfolios to account for correlations

among risk factors. Trading limits are approved at least annually.

The ALMRC has given authority to the GMRC to approve changes

to trading limits throughout the year. Approved trading limits are

stored and tracked in a centralized limits management system.

Trading limit excesses are communicated to management for

review. Certain quantitative market risk measures and

corresponding limits have been identified as critical in the

Corporation’s Risk Appetite Statement. These risk appetite limits

are monitored on a daily basis and are approved at least annually

by the Board. The market risk based risk appetite limits were not

exceeded during 2013.

In periods of market stress, the GMRC members communicate

daily to discuss losses, key risk positions and any limit excesses.

As a result of this process, the businesses may selectively reduce

risk. Where economically feasible, positions are sold or

macroeconomic hedges are executed to reduce the exposures.

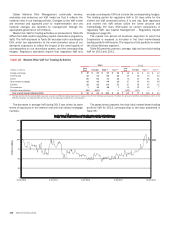

Backtesting

The accuracy of the VaR methodology is evaluated by backtesting,

which compares the daily regulatory VaR results, utilizing a one-

day holding period, against the realized daily profit and loss.

Backtesting excesses occur when a trading loss exceeds the VaR

for the corresponding day. These excesses are evaluated to

understand the positions and market moves that produced the

trading loss and to ensure that the VaR methodology accurately

represents those losses. As our primary VaR statistic used for

backtesting is based on a 99 percent confidence interval and a

one-day holding period, we expect one trading loss in excess of

VaR every 100 days, or between two to three trading losses in

excess of VaR over the course of a year. The number of backtesting

excesses observed can differ from the statistically expected

number of excesses if the current level of market volatility is

materially different than the level of market volatility that existed

during the three years of historical data used in the VaR calculation.

We conduct daily backtesting on our portfolios and report the

results to senior market risk management. Senior management,

including the GMRC, regularly reviews and evaluates the results

of these tests. The government agencies that regulate our

operations also regularly review these results.

The revenue used for backtesting is defined by regulatory

agencies in order to most closely align with the VaR component

of the regulatory capital calculation. This revenue differs from total

trading-related revenue in that it excludes revenues from trading

activities that either do not generate market risk or the market

risk cannot be included in VaR. Some examples of the types of

revenue excluded for backtesting are fees, commissions, reserves,

net interest income and intraday trading revenues. In addition,

counterparty CVA is not included in the VaR component of the

regulatory capital calculation and is therefore not included in the

revenue used for backtesting.

There were no days with backtesting excesses for our total

market-based trading portfolio VaR, utilizing a holding period,

during 2013.

Total Trading Revenue

Total trading-related revenue, excluding brokerage fees, represents

the total amount earned from trading positions, including market-

based net interest income, which are taken in a diverse range of

financial instruments and markets. Trading account assets and

liabilities are reported at fair value. For more information on fair

value, see Note 20 – Fair Value Measurements to the Consolidated

Financial Statements. Trading-related revenues can be volatile and

are largely driven by general market conditions and customer

demand. Also, trading-related revenues are dependent on the

volume and type of transactions, the level of risk assumed, and

the volatility of price and rate movements at any given time within

the ever-changing market environment. Significant daily revenues

by business are monitored and the primary drivers of these are

reviewed. When it is deemed material, an explanation of these

revenues is provided to the GMRC.