Bank of America 2013 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2013 87

We classify junior-lien home equity loans as nonperforming

when the first-lien loan becomes 90 days past due even if the

junior-lien loan is performing. At December 31, 2013 and 2012,

$1.2 billion and $1.5 billion of such junior-lien home equity loans

were included in nonperforming loans and leases.

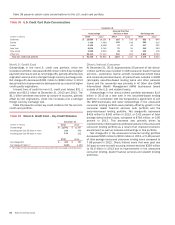

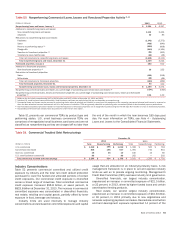

Table 42 presents TDRs for the home loans portfolio.

Performing TDR balances are excluded from nonperforming loans

in Table 41.

Table 42 Home Loans Troubled Debt Restructurings

December 31

2013 2012

(Dollars in millions) Total Nonperforming Performing Total Nonperforming Performing

Residential mortgage (1, 2) $ 29,312 $ 7,555 $ 21,757 $ 28,125 $ 9,040 $ 19,085

Home equity (3) 2,146 1,389 757 2,125 1,242 883

Total home loans troubled debt restructurings $ 31,458 $ 8,944 $ 22,514 $ 30,250 $ 10,282 $ 19,968

(1) Residential mortgage TDRs deemed collateral dependent totaled $8.2 billion and $9.4 billion, and included $5.7 billion and $6.4 billion of loans classified as nonperforming and $2.5 billion and

$3.0 billion of loans classified as performing at December 31, 2013 and 2012.

(2) Residential mortgage performing TDRs included $14.3 billion and $11.9 billion of loans that were fully-insured at December 31, 2013 and 2012.

(3) Home equity TDRs deemed collateral dependent totaled $1.4 billion and $1.4 billion, and included $1.2 billion and $1.0 billion of loans classified as nonperforming and $227 million and $348

million of loans classified as performing at December 31, 2013 and 2012.

We work with customers that are experiencing financial difficulty

by modifying credit card and other consumer loans, while complying

with Federal Financial Institutions Examination Council (FFIEC)

guidelines. Credit card and other consumer loan modifications

generally involve a reduction in the customer’s interest rate on the

account and placing the customer on a fixed payment plan not

exceeding 60 months, all of which are considered TDRs (the

renegotiated TDR portfolio). In addition, non-U.S. credit card

modifications may involve reducing the interest rate on the account

without placing the customer on a fixed payment plan, and these

are also considered TDRs (also a part of the renegotiated TDR

portfolio).

In all cases, the customer’s available line of credit is canceled.

We make modifications primarily through internal renegotiation

programs utilizing direct customer contact, but may also utilize

external renegotiation programs. The renegotiated TDR portfolio

is excluded in large part from Table 41 as substantially all of the

loans remain on accrual status until either charged off or paid in

full. At December 31, 2013 and 2012, our renegotiated TDR

portfolio was $2.1 billion and $3.9 billion, of which $1.6 billion

and $3.1 billion were current or less than 30 days past due under

the modified terms. The decline in the renegotiated TDR portfolio

was primarily driven by paydowns and charge-offs as well as lower

program enrollments. For more information on the renegotiated

TDR portfolio, see Note 4 – Outstanding Loans and Leases to the

Consolidated Financial Statements.

Commercial Portfolio Credit Risk Management

Credit risk management for the commercial portfolio begins with

an assessment of the credit risk profile of the borrower or

counterparty based on an analysis of its financial position. As part

of the overall credit risk assessment, our commercial credit

exposures are assigned a risk rating and are subject to approval

based on defined credit approval standards. Subsequent to loan

origination, risk ratings are monitored on an ongoing basis, and if

necessary, adjusted to reflect changes in the financial condition,

cash flow, risk profile or outlook of a borrower or counterparty. In

making credit decisions, we consider risk rating, collateral, country,

industry and single name concentration limits while also balancing

this with total borrower or counterparty relationship. Our business

and risk management personnel use a variety of tools to

continuously monitor the ability of a borrower or counterparty to

perform under its obligations. We use risk rating aggregations to

measure and evaluate concentrations within portfolios. In addition,

risk ratings are a factor in determining the level of allocated capital

and the allowance for credit losses.

For information on our accounting policies regarding

delinquencies, nonperforming status and net charge-offs for the

commercial portfolio, see Note 1 – Summary of Significant

Accounting Principles to the Consolidated Financial Statements.

Management of Commercial Credit Risk

Concentrations

Commercial credit risk is evaluated and managed with the goal

that concentrations of credit exposure do not result in undesirable

levels of risk. We review, measure and manage concentrations of

credit exposure by industry, product, geography, customer

relationship and loan size. We also review, measure and manage

commercial real estate loans by geographic location and property

type. In addition, within our non-U.S. portfolio, we evaluate

exposures by region and by country. Tables 47, 52, 60 and 61

summarize our concentrations. We also utilize syndications of

exposure to third parties, loan sales, hedging and other risk

mitigation techniques to manage the size and risk profile of the

commercial credit portfolio.

As part of our ongoing risk mitigation initiatives, we attempt to

work with clients experiencing financial difficulty to modify their

loans to terms that better align with their current ability to pay. In

situations where an economic concession has been granted to a

borrower experiencing financial difficulty, we identify these loans

as TDRs.

We account for certain large corporate loans and loan

commitments, including issued but unfunded letters of credit

which are considered utilized for credit risk management purposes,

that exceed our single name credit risk concentration guidelines

under the fair value option. Lending commitments, both funded

and unfunded, are actively managed and monitored, and as

appropriate, credit risk for these lending relationships may be

mitigated through the use of credit derivatives, with the

Corporation’s credit view and market perspectives determining the

size and timing of the hedging activity. In addition, we purchase

credit protection to cover the funded portion as well as the

unfunded portion of certain other credit exposures. To lessen the

cost of obtaining our desired credit protection levels, credit

exposure may be added within an industry, borrower or

counterparty group by selling protection. These credit derivatives