Bank of America 2013 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

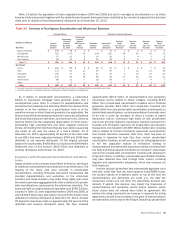

Bank of America 2013 51

Table 13 details the population of loans originated between 2004 and 2008 and sold in non-agency securitizations or as whole

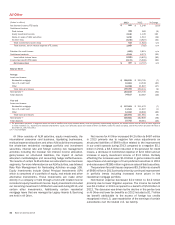

loans by entity and product together with the defaulted and severely delinquent loans stratified by the number of payments the borrower

made prior to default or becoming severely delinquent as of December 31, 2013.

Table 13 Overview of Non-Agency Securitization and Whole-loan Balances

Principal Balance Defaulted or Severely Delinquent

(Dollars in billions)

By Entity

Original

Principal

Balance

Outstanding

Principal

Balance

December

31, 2013

Outstanding

Principal

Balance

180 Days or

More

Past Due

Defaulted

Principal

Balance

Defaulted or

Severely

Delinquent

Borrower

Made

Less than 13

Payments

Borrower

Made

13 to 24

Payments

Borrower

Made

25 to 36

Payments

Borrower

Made

More than 36

Payments

Bank of America $ 100 $ 18 $ 3 $ 7 $ 10 $ 1 $ 2 $ 2 $ 5

Countrywide 716 173 43 144 187 24 45 45 73

Merrill Lynch 67 15 3 16 19 3 4 3 9

First Franklin 82 15 4 25 29 5 6 5 13

Total (1, 2) $ 965 $ 221 $ 53 $ 192 $ 245 $33$57 $55 $ 100

By Product

Prime $ 302$ 66$ 8$ 26$ 34$ 2$ 6$ 7$ 19

Alt-A 172 50 11 39 50 7 12 12 19

Pay option 150 37 14 41 55 5 13 15 22

Subprime 247 55 18 66 84 17 20 16 31

Home equity 88 11 — 18 182547

Other 62224—112

Total $ 965 $ 221 $ 53 $ 192 $ 245 $33$57 $55 $ 100

(1) Excludes transactions sponsored by Bank of America and Merrill Lynch where no representations or warranties were made.

(2) Includes exposures on third-party sponsored transactions related to legacy entity originations.

As it relates to private-label securitizations, a contractual

liability to repurchase mortgage loans generally arises only if

counterparties prove there is a breach of representations and

warranties that materially and adversely affects the interest of the

investor or all the investors in a securitization trust or of the

monoline insurer or other financial guarantor (as applicable). We

believe many of the loan defaults observed in these securitizations

and whole-loan balances have been, and continue to be, driven by

external factors like the substantial depreciation in home prices,

persistently high unemployment and other negative economic

trends, diminishing the likelihood that any loan defect (assuming

one exists at all) was the cause of a loan’s default. As of

December 31, 2013, approximately 25 percent of the loans sold

to non-GSEs that were originated between 2004 and 2008 have

defaulted or are severely delinquent. Of the original principal

balance for Countrywide, $409 billion is included in the BNY Mellon

Settlement and, of this amount, $109 billion was defaulted or

severely delinquent at December 31, 2013.

Experience with Private-label Securitizations and Whole

Loans

Legacy entities, and to a lesser extent Bank of America, sold loans

to investors via private-label securitizations or as whole loans. The

majority of the loans sold were included in private-label

securitizations, including third-party sponsored transactions. We

provided representations and warranties to the whole-loan

investors and these investors may retain those rights even when

the whole loans were aggregated with other collateral into private-

label securitizations sponsored by the whole-loan investors. The

loans sold with an original total principal balance of $780.5 billion,

included in Table 13, were originated between 2004 and 2008, of

which $449.9 billion have been paid in full and $191.3 billion were

defaulted or severely delinquent at December 31, 2013. At least

25 payments have been made on approximately 64 percent of the

defaulted and severely delinquent loans. We have received

approximately $25.9 billion of representations and warranties

repurchase claims related to these vintages, including $16.9

billion from private-label securitization trustees and a financial

guarantee provider, $8.2 billion from whole-loan investors and

$809 million from one private-label securitization counterparty. In

private-label securitizations, certain presentation thresholds need

to be met in order for investors to direct a trustee to assert

repurchase claims. Continued high levels of new private-label

claims are primarily related to repurchase requests received from

trustees and third-party sponsors for private-label securitization

transactions not included in the BNY Mellon Settlement, including

claims related to first-lien third-party sponsored securitizations

that include monoline insurance. Over time, there has been an

increase in requests for loan files from certain private-label

securitization trustees, as well as requests for tolling agreements

to toll the applicable statute of limitations relating to

representations and warranties repurchase claims, and we believe

it is likely that these requests will lead to an increase in repurchase

claims from private-label securitization trustees with standing to

bring such claims. In addition, private-label securitization trustees

may have obtained loan files through other means, including

litigation and administrative subpoenas, which may increase our

total exposure.

A recent decision by the New York intermediate appellate court

held that, under New York law, which governs many RMBS trusts,

the six-year statute of limitations starts to run at the time the

representations and warranties are made (i.e., the date the

transaction closed and not when the repurchase demand was

denied). If upheld, this decision may impact the timeliness of

representations and warranties claims and/or lawsuits, where

these claims have not already been tolled by agreement. We

believe this ruling may lead to an increase in requests for tolling

agreements as well as an increase in the pace of representations

and warranties claims and/or the filing of lawsuits by private-label