Bank of America 2013 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

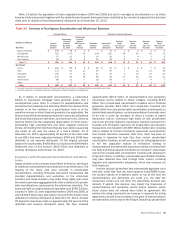

52 Bank of America 2013

securitization trustees prior the expiration of the statute of

limitations.

We have resolved $8.0 billion of the $25.9 billion of claims

received from whole-loan and private-label securitization

counterparties with losses of $1.9 billion. The majority of these

resolved claims were from third-party whole-loan investors.

Approximately $3.3 billion of these claims were resolved through

repurchase or indemnification and $4.7 billion were rescinded by

the investor. At December 31, 2013, for loans originated between

2004 and 2008, the notional amount of unresolved repurchase

claims submitted by private-label securitization trustees, whole-

loan investors and a financial guarantee provider was $17.9 billion.

We have performed an initial review with respect to $14.6 billion

of these claims and do not believe a valid basis for repurchase

has been established by the claimant and are still in the process

of reviewing the remaining $3.3 billion of these claims. Until we

receive a repurchase claim, we generally do not review loan files

related to private-label securitizations sponsored by third-party

whole-loan investors (and are not required by the governing

documents to do so).

Certain whole-loan investors have engaged with us in a

consistent repurchase process and we have used that and other

experience to record a liability related to existing and future claims

from such counterparties. The BNY Mellon Settlement and

subsequent activity with certain counterparties led to the

determination that we had sufficient experience to record a liability

related to our exposure on certain private-label securitizations,

including certain private-label securitizations sponsored by third-

party whole-loan investors, however, it did not provide sufficient

experience to record a liability related to other private-label

securitizations sponsored by third-party whole-loan investors. As

it relates to the other private-label securitizations sponsored by

third-party whole-loan investors and certain other whole-loan sales,

it is not possible to determine whether a loss has occurred or is

probable and, therefore, no representations and warranties liability

has been recorded in connection with these transactions. As

discussed below, our estimated range of possible loss related to

representations and warranties exposures as of December 31,

2013 included possible losses related to these whole-loan sales

and private-label securitizations sponsored by third-party whole-

loan investors.

The representations and warranties, as governed by the private-

label securitization agreements, generally require that

counterparties have the ability to both assert a claim and actually

prove that a loan has an actionable defect under the applicable

contracts. While the Corporation believes the agreements for

private-label securitizations generally contain less rigorous

representations and warranties and place higher burdens on

claimants seeking repurchases than the express provisions of

comparable agreements with the GSEs, without regard to any

variations that may have arisen as a result of dealings with the

GSEs, the agreements generally include a representation that

underwriting practices were prudent and customary. In the case

of private-label securitization trustees and third-party sponsors,

there is currently no established process in place for the parties

to reach a conclusion on an individual loan if there is a

disagreement on the resolution of the claim. Private-label

securitization investors generally do not have the contractual right

to demand repurchase of loans directly or the right to access loan

files.

Experience with Monoline Insurers

Legacy companies sold $184.5 billion of loans originated between

2004 and 2008 into monoline-insured securitizations, which are

included in Table 13. At December 31, 2013, for loans originated

between 2004 and 2008, the unpaid principal balance of loans

related to unresolved monoline repurchase claims was $1.5 billion

compared to $2.4 billion at December 31, 2012. The decrease in

unresolved monoline repurchase claims was driven by the

resolution of claims through the MBIA Settlement.

During 2013, there was minimal repurchase claim activity with

the monolines and the monolines did not request any loan files

for review through the representations and warranties process.

However, there may be additional claims or file requests in the

future.

The MBIA Settlement in 2013 resolved outstanding and

potential claims between the parties to the settlement involving

31 first- and 17 second-lien RMBS trusts for which MBIA provided

financial guarantee insurance, including $945 million of monoline

repurchase claims outstanding at December 31, 2012. For more

information on the MBIA Settlement, see Note 7 – Representations

and Warranties Obligations and Corporate Guarantees to the

Consolidated Financial Statements.

Open Mortgage Insurance Rescission Notices

In addition to repurchase claims, we receive notices from mortgage

insurance companies of claim denials, cancellations or coverage

rescission (collectively, MI rescission notices). Although the

number of such open notices has remained elevated, they have

decreased over the last several quarters as the resolution of open

notices exceeded new notices.

At December 31, 2013, we had approximately 101,000 open

MI rescission notices compared to 110,000 at December 31,

2012. Open MI rescission notices at December 31, 2013 included

39,000 pertaining principally to first-lien mortgages serviced for

others, 10,000 pertaining to loans held-for-investment (HFI) and

52,000 pertaining to ongoing litigation for second-lien mortgages.

For more information on open mortgage insurance rescission

notices, see Note 7 – Representations and Warranties Obligations

and Corporate Guarantees to the Consolidated Financial

Statements.

Estimated Range of Possible Loss

We currently estimate that the range of possible loss for

representations and warranties exposures could be up to $4 billion

over existing accruals at December 31, 2013. The estimated range

of possible loss reflects principally non-GSE exposures. It

represents a reasonably possible loss, but does not represent a

probable loss, and is based on currently available information,

significant judgment and a number of assumptions that are subject

to change.

The liability for representations and warranties exposures and

the corresponding estimated range of possible loss do not

consider any losses related to litigation matters, including RMBS

litigation or litigation brought by monoline insurers, nor do they

include any separate foreclosure costs and related costs,

assessments and compensatory fees or any other possible losses

related to potential claims for breaches of performance of servicing

obligations, except as such losses are included as potential costs

of the BNY Mellon Settlement, potential securities law or fraud

claims or potential indemnity or other claims against us, including

claims related to loans insured by the FHA. We are not able to