Bank of America 2013 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2013 67

and leverage capital and stress test requirements. Also, a debt-

to-equity limit may be enacted for an individual BHC if determined

to pose a grave threat to the financial stability of the U.S., at the

discretion of the Financial Stability Oversight Council (FSOC) or

the Federal Reserve on behalf of the FSOC.

For more information regarding Basel 3 and other proposed

regulatory capital changes, see Note 16 – Regulatory Requirements

and Restrictions to the Consolidated Financial Statements.

Bank of America, N.A. and FIA Card Services, N.A.

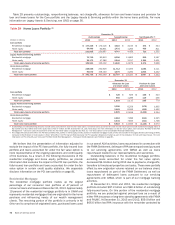

Regulatory Capital

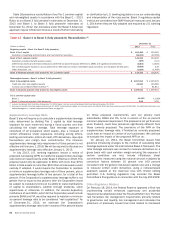

Table 19 presents regulatory capital information for BANA and FIA

at December 31, 2013 and 2012.

Table 19 Bank of America, N.A. and

FIA Card Services, N.A. Regulatory Capital (1)

December 31

2013 2012

(Dollars in millions) Ratio Amount Ratio Amount

Tier 1 capital

Bank of America, N.A. 12.34% $ 125,886 12.44% $ 118,431

FIA Card Services, N.A. 16.83 20,135 17.34 22,061

Total capital

Bank of America, N.A. 13.84 141,232 14.76 140,434

FIA Card Services, N.A. 18.12 21,672 18.64 23,707

Tier 1 leverage

Bank of America, N.A. 9.21 125,886 8.59 118,431

FIA Card Services, N.A. 12.91 20,135 13.67 22,061

(1) BANA regulatory capital information included the Basel 1 – 2013 Rules at December 31, 2013.

At December 31, 2012, BANA regulatory capital information did not include the Basel 1 – 2013

Rules. FIA is not impacted by the Basel 1 – 2013 Rules.

BANA’s Tier 1 capital ratio decreased 10 bps to 12.34 percent

and the Total capital ratio decreased 92 bps to 13.84 percent at

December 31, 2013 compared to December 31, 2012. The Tier

1 leverage ratio increased 62 bps to 9.21 percent at December 31,

2013 compared to December 31, 2012. The decrease in the Tier

1 capital ratio was driven by an increase in risk-weighted assets

of $68.5 billion compared to the prior year, dividends and returns

of capital to the Corporation of $8.5 billion and $2.2 billion during

2013, partially offset by earnings eligible to be included in capital

of $16.5 billion. The increase in risk-weighted assets was primarily

due to the impact of implementing the Basel 1 – 2013 Rules and

an increase in loans. The decrease in the Total capital ratio was

driven by the same factors as the Tier 1 capital ratio as well as a

$7.0 billion decrease in qualifying subordinated debt during 2013.

The increase in the Tier 1 leverage ratio was driven by an increase

in Tier 1 capital and a decrease in adjusted quarterly average total

assets of $11.6 billion.

FIA’s Tier 1 capital ratio decreased 51 bps to 16.83 percent

and the Total capital ratio decreased 52 bps to 18.12 percent at

December 31, 2013 compared to December 31, 2012. The Tier

1 leverage ratio decreased 76 bps to 12.91 percent at

December 31, 2013 compared to December 31, 2012. The

decrease in the Tier 1 capital and Total capital ratios was driven

by returns of capital of $6.5 billion to the Corporation during 2013,

partially offset by earnings eligible to be included in capital of $4.3

billion and a decrease in risk-weighted assets of $7.6 billion

primarily due to a decrease in loans. The decrease in the Tier 1

leverage ratio was driven by the decrease in Tier 1 capital, partially

offset by a decrease in adjusted quarterly average total assets of

$5.3 billion. FIA was not impacted by the implementation of the

Basel 1 – 2013 Rules.

Broker/Dealer Regulatory Capital and Securities

Regulation

The Corporation’s principal U.S. broker/dealer subsidiaries are

Merrill Lynch, Pierce, Fenner & Smith (MLPF&S) and Merrill Lynch

Professional Clearing Corp (MLPCC). MLPCC is a fully-guaranteed

subsidiary of MLPF&S and provides clearing and settlement

services. Both entities are subject to the net capital requirements

of SEC Rule 15c3-1. Both entities are also registered as futures

commission merchants and are subject to the Commodity Futures

Trading Commission Regulation 1.17.

MLPF&S has elected to compute the minimum capital

requirement in accordance with the Alternative Net Capital

Requirement as permitted by SEC Rule 15c3-1. At December 31,

2013, MLPF&S’s regulatory net capital as defined by Rule 15c3-1

was $10.0 billion and exceeded the minimum requirement of $951

million by $9.0 billion. MLPCC’s net capital of $2.2 billion exceeded

the minimum requirement of $366 million by $1.8 billion.

In accordance with the Alternative Net Capital Requirements,

MLPF&S is required to maintain tentative net capital in excess of

$1.0 billion, net capital in excess of $500 million and notify the

SEC in the event its tentative net capital is less than $5.0 billion.

At December 31, 2013, MLPF&S had tentative net capital and net

capital in excess of the minimum and notification requirements.

Merrill Lynch International (MLI), a U.K. investment firm, is

regulated by the PRA and the FCA and is subject to certain

regulatory capital requirements. Following an increase in capital

resources in advance of the implementation of Basel 3 in 2014,

at December 31, 2013, MLI’s capital resources were $28.2 billion

and exceeded the minimum requirement of $10.8 billion and had

enough excess to cover any additional requirements as set by the

regulators.

Common Stock Dividends

For a summary of our declared quarterly cash dividends on

common stock during 2013 and through February 25, 2014, see

Note 13 – Shareholders’ Equity to the Consolidated Financial

Statements.

Liquidity Risk

Funding and Liquidity Risk Management

We define liquidity risk as the potential inability to meet our

contractual and contingent financial obligations, on- or off-balance

sheet, as they come due. Our primary liquidity objective is to

provide adequate funding for our businesses throughout market

cycles, including periods of financial stress. To achieve that

objective, we analyze and monitor our liquidity risk, maintain excess

liquidity and access diverse funding sources including our stable

deposit base. We define excess liquidity as readily available

assets, limited to cash and high-quality, liquid, unencumbered

securities that we can use to meet our funding requirements as

those obligations arise.

Global funding and liquidity risk management activities are

centralized within Corporate Treasury. We believe that a centralized

approach to funding and liquidity risk management enhances our

ability to monitor liquidity requirements, maximizes access to

funding sources, minimizes borrowing costs and facilitates timely

responses to liquidity events.