Bank of America 2013 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

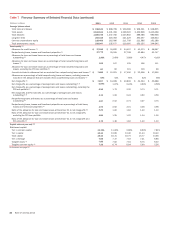

Bank of America 2013 33

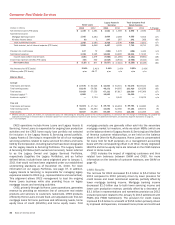

Consumer & Business Banking

Deposits

Consumer

Lending

Total Consumer &

Business Banking

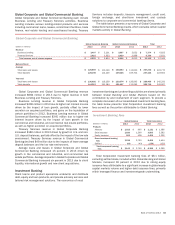

(Dollars in millions) 2013 2012 2013 2012 2013 2012 % Change

Net interest income (FTE basis) $ 9,808 $ 9,046 $ 10,243 $ 10,807 $20,051 $ 19,853 1%

Noninterest income:

Card income 60 62 4,744 5,253 4,804 5,315 (10)

Service charges 4,208 4,277 ——4,208 4,277 (2)

All other income (loss) 509 397 295 (52) 804 345 133

Total noninterest income 4,777 4,736 5,039 5,201 9,816 9,937 (1)

Total revenue, net of interest expense (FTE basis) 14,585 13,782 15,282 16,008 29,867 29,790 —

Provision for credit losses 299 488 2,808 3,660 3,107 4,148 (25)

Noninterest expense 10,927 11,310 5,430 5,685 16,357 16,995 (4)

Income before income taxes 3,359 1,984 7,044 6,663 10,403 8,647 20

Income tax expense (FTE basis) 1,232 723 2,583 2,378 3,815 3,101 23

Net income $ 2,127 $ 1,261 $ 4,461 $ 4,285 $ 6,588 $ 5,546 19

Net interest yield (FTE basis) 1.88% 1.90% 7.18%7.18% 3.72%4.04%

Return on average allocated capital (1) 13.82 —30.60 —21.98 —

Return on average economic capital (1) —9.72 —38.83 —23.12

Efficiency ratio (FTE basis) 74.92 82.07 35.53 35.51 54.76 57.05

Balance Sheet

Average

Total loans and leases $ 22,437 $ 23,369 $ 142,133 $149,667 $ 164,570 $173,036 (5)

Total earning assets (2) 522,870 477,142 142,725 150,515 539,213 491,767 10

Total assets (2) 555,653 510,384 151,443 158,333 580,714 532,827 9

Total deposits 518,470 474,822 n/m n/m 518,980 475,180 9

Allocated capital (1) 15,400 —14,600 —30,000 — n/m

Economic capital (1) —12,985 —11,066 —24,051 n/m

Year end

Total loans and leases $ 22,574 $ 22,907 $ 142,516 $146,359 $ 165,090 $169,266 (2)

Total earning assets (2) 534,946 498,147 143,917 146,809 550,610 513,109 7

Total assets (2) 567,837 531,354 153,394 155,408 592,978 554,915 7

Total deposits 530,947 495,711 n/m n/m 531,707 496,159 7

(1) Effective January 1, 2013, we revised, on a prospective basis, the methodology for allocating capital to the business segments. In connection with the change in methodology, we updated the

applicable terminology in the above table to allocated capital from economic capital as reported in prior periods. For additional information, see Business Segment Operations on page 31.

(2) For presentation purposes, in segments and businesses where the total of liabilities and equity exceeds assets, we allocate assets from All Other to match the segments’ and businesses’ liabilities

and allocated shareholders’ equity. As a result, total earning assets and total assets of the businesses may not equal total CBB.

n/m = not meaningful

CBB, which is comprised of Deposits and Consumer Lending,

offers a diversified range of credit, banking and investment

products and services to consumers and businesses. Our

customers and clients have access to a franchise network that

stretches coast to coast through 31 states and the District of

Columbia. The franchise network includes approximately 5,100

banking centers, 16,300 ATMs, nationwide call centers, and online

and mobile platforms. During 2013, Business Banking results

were moved into Deposits as we continue to integrate these

businesses. Also during 2013, consumer Dealer Financial

Services (DFS) results were moved into CBB from Global Banking

to align this business more closely with our consumer lending

activity and better serve the needs of our customers. As a result,

Card Services was renamed Consumer Lending. Prior periods were

reclassified to conform to current period presentation.

CBB Results

Net income for CBB increased $1.0 billion to $6.6 billion in 2013

compared to 2012 primarily driven by lower provision for credit

losses and noninterest expense. Net interest income of $20.1

billion remained relatively unchanged as the impact of higher

deposit balances was offset by the impact of lower average loan

balances. Noninterest income of $9.8 billion remained relatively

unchanged as the allocation of certain card revenue to GWIM for

clients with a credit card, as described below, and lower deposit

service charges were offset by the net impact of consumer

protection products, primarily due to charges recorded in 2012.

The provision for credit losses decreased $1.0 billion to $3.1

billion in 2013 primarily as a result of improvements in credit

quality. Noninterest expense decreased $638 million to $16.4

billion driven by lower operating, personnel and FDIC expenses.