Bank of America 2013 Annual Report Download - page 211

Download and view the complete annual report

Please find page 211 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

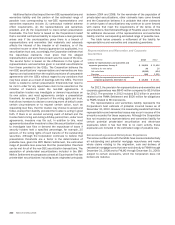

Bank of America 2013 209

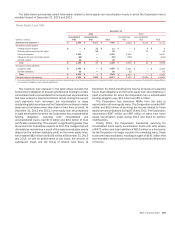

Private-label Securitizations and Whole-loan Sales

Experience

In private-label securitizations, certain presentation thresholds

need to be met in order for investors to direct a trustee to assert

repurchase claims. Continued high levels of new private-label

claims are primarily related to repurchase requests received from

trustees and third-party sponsors for private-label securitization

transactions not included in the BNY Mellon Settlement, including

claims related to first-lien third-party sponsored securitizations

that include monoline insurance. Over time, there has been an

increase in requests for loan files from certain private-label

securitization trustees, as well as requests for tolling agreements

to toll the applicable statute of limitations relating to

representations and warranties repurchase claims and the

Corporation believes it is likely that these requests will lead to an

increase in repurchase claims for private-label securitization

trustees with standing to bring such claims. In addition, private-

label securitization trustees may have obtained loan files through

other means, including litigation and administrative subpoenas,

which may increase the Corporation’s total exposure. A recent

decision by the New York intermediate appellate court held that,

under New York law, which governs many RMBS trusts, the six-year

statute of limitations starts to run at the time the representations

and warranties are made (i.e., the date the transaction closed and

not when the repurchase demand was denied). If upheld, this

decision may impact the timeliness of representations and

warranties claims and/or lawsuits, where these claims have not

already been tolled by agreement. The Corporation believes this

ruling may lead to an increase in requests for tolling agreements

as well as an increase in the pace of representations and

warranties claims and/or the filing of lawsuits by private-label

securitization trustees prior to the expiration of the statute of

limitations.

The representations and warranties, as governed by the private-

label securitization agreements, generally require that

counterparties have the ability to both assert a claim and actually

prove that a loan has an actionable defect under the applicable

contracts. While the Corporation believes the agreements for

private-label securitizations generally contain less rigorous

representations and warranties and place higher burdens on

claimants seeking repurchases than the express provisions of

comparable agreements with the GSEs, without regard to any

variations that may have arisen as a result of dealings with the

GSEs, the agreements generally include a representation that

underwriting practices were prudent and customary. In the case

of private-label securitization trustees and third-party sponsors,

there is currently no established process in place for the parties

to reach a conclusion on an individual loan if there is a

disagreement on the resolution of the claim. For more information

on repurchase demands, see Unresolved Repurchase Claims in

this Note.

The majority of the repurchase claims that the Corporation has

received and resolved outside of those from the GSEs and

monolines are from third-party whole-loan investors. The

Corporation provided representations and warranties and the

whole-loan investors may retain those rights even when the loans

were aggregated with other collateral into private-label

securitizations sponsored by the whole-loan investors. The

Corporation reviews properly presented repurchase claims for

these whole loans on a loan-by-loan basis. If, after the

Corporation’s review, it does not believe a claim is valid, it will deny

the claim and generally indicate a reason for the denial. When the

whole-loan investor agrees with the Corporation’s denial of the

claim, the whole-loan investor may rescind the claim. When there

is disagreement as to the resolution of the claim, meaningful

dialogue and negotiation between the parties are generally

necessary to reach a resolution on an individual claim. Generally,

a whole-loan investor is engaged in the repurchase process and

the Corporation and the whole-loan investor reach resolution,

either through loan-by-loan negotiation or at times, through a bulk

settlement. As of December 31, 2013, 16 percent of the whole-

loan claims that the Corporation initially denied have subsequently

been resolved through repurchase or make-whole payments and

44 percent have been resolved through rescission or repayment

in full by the borrower. Although the timeline for resolution varies,

once an actionable breach is identified on a given loan, settlement

is generally reached as to that loan within 60 days. When a claim

has been denied and the Corporation does not have

communication with the counterparty for six months, the

Corporation views these claims as inactive; however, they remain

in the outstanding claims balance until resolution.

At December 31, 2013, for loans originated between 2004 and

2008, the notional amount of unresolved repurchase claims

submitted by private-label securitization trustees, a financial

guarantee provider and whole-loan investors was $17.9 billion.

The Corporation has performed an initial review with respect to

$14.6 billion of these claims and does not believe a valid basis

for repurchase has been established by the claimant and is still

in the process of reviewing the remaining $3.3 billion of these

claims.

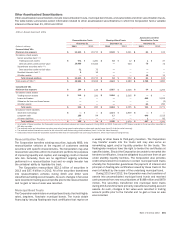

Monoline Insurers Experience

The Corporation has had limited representations and warranties

repurchase claims experience with the monoline insurers due to

ongoing litigation against Countrywide and/or Bank of America. To

the extent the Corporation received repurchase claims from the

monolines that are properly presented, it generally reviews them

on a loan-by-loan basis. Where a breach of representations and

warranties given by the Corporation or subsidiaries or legacy

companies is confirmed on a given loan, settlement is generally

reached as to that loan within 60 to 90 days. For more information

related to the monolines, see Note 12 – Commitments and

Contingencies.

The MBIA Settlement resolved outstanding and potential

claims between the parties to the settlement involving 31 first-

and 17 second-lien RMBS trusts for which MBIA provided financial

guarantee insurance, including $945 million of monoline

repurchase claims outstanding at December 31, 2012. The first-

and second-lien mortgages in the covered RMBS trusts had an

original principal balance of $29.3 billion and $25.5 billion, and

an unpaid principal balance of $9.8 billion and $9.3 billion at the

time of the settlement.

During 2013, there was minimal loan-level repurchase claim

activity with the monolines and the monolines did not request any

loan files for review through the representations and warranties

process.

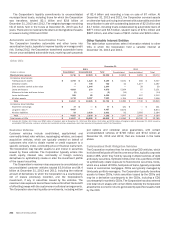

Open Mortgage Insurance Rescission Notices

In addition to repurchase claims, the Corporation receives notices

from mortgage insurance companies of claim denials,

cancellations or coverage rescission (collectively, MI rescission

notices). Although the number of such open notices has remained

elevated, they have decreased over the last several quarters as