Bank of America 2013 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2013 23

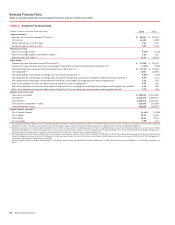

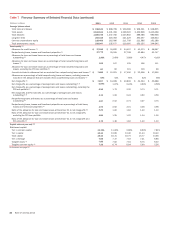

Financial Highlights

Net income was $11.4 billion, or $0.90 per diluted share in 2013

compared to $4.2 billion, or $0.25 per diluted share in 2012. The

results for 2013 reflect our efforts to stabilize revenue, decrease

costs, strengthen the balance sheet and improve credit quality.

Table 2 Summary Income Statement

(Dollars in millions) 2013 2012

Net interest income (FTE basis) (1) $ 43,124 $ 41,557

Noninterest income 46,677 42,678

Total revenue, net of interest expense (FTE basis) (1) 89,801 84,235

Provision for credit losses 3,556 8,169

Noninterest expense 69,214 72,093

Income before income taxes 17,031 3,973

Income tax expense (benefit) (FTE basis) (1) 5,600 (215)

Net income 11,431 4,188

Preferred stock dividends 1,349 1,428

Net income applicable to common shareholders $ 10,082 $ 2,760

Per common share information

Earnings $0.94

$0.26

Diluted earnings 0.90 0.25

(1) FTE basis is a non-GAAP financial measure. For more information on this measure, see

Supplemental Financial Data on page 29, and for a corresponding reconciliation to GAAP financial

measures, see Statistical Table XV.

Net Interest Income

Net interest income on a fully taxable-equivalent (FTE) basis

increased $1.6 billion to $43.1 billion for 2013 compared to 2012.

The increase was primarily due to reductions in long-term debt

balances, higher yields on debt securities including the impact of

market-related premium amortization expense, lower rates paid

on deposits, higher commercial loan balances and increased

trading-related net interest income, partially offset by lower

consumer loan balances as well as lower asset yields and the low

rate environment. The net interest yield on a FTE basis increased

12 basis points (bps) to 2.47 percent for 2013 compared to 2012

due to the same factors as described above.

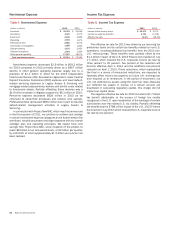

Noninterest Income

Table 3 Noninterest Income

(Dollars in millions) 2013 2012

Card income $ 5,826 $ 6,121

Service charges 7,390 7,600

Investment and brokerage services 12,282 11,393

Investment banking income 6,126 5,299

Equity investment income 2,901 2,070

Trading account profits 7,056 5,870

Mortgage banking income 3,874 4,750

Gains on sales of debt securities 1,271 1,662

Other loss (29) (2,034)

Net impairment losses recognized in earnings on AFS

debt securities (20) (53)

Total noninterest income $ 46,677 $ 42,678

Noninterest income increased $4.0 billion to $46.7 billion for

2013 compared to 2012. The following highlights the significant

changes.

Card income decreased $295 million primarily driven by lower

revenue as a result of our exit of consumer protection products.

Investment and brokerage services income increased $889

million primarily driven by the impact of long-term assets under

management (AUM) inflows and higher market levels.

Investment banking income increased $827 million primarily

due to strong equity issuance fees attributable to a significant

increase in global equity capital markets volume and higher debt

issuance fees, primarily within leveraged finance and

investment-grade underwriting.

Equity investment income increased $831 million. The results

for 2013 included $753 million of gains related to the sale of

our remaining investment in China Construction Bank

Corporation (CCB) and gains of $1.4 billion on the sales of a

portion of an equity investment. The results for 2012 included

$1.6 billion of gains related to sales of certain equity and

strategic investments.

Trading account profits increased $1.2 billion. Net debit

valuation adjustment (DVA) losses on derivatives were $508

million in 2013 compared to losses of $2.5 billion in 2012.

Excluding net DVA, trading account profits decreased $783

million due to decreases in our fixed-income, currency and

commodities (FICC) businesses driven by a challenging trading

environment, partially offset by an increase in our equities

businesses.

Mortgage banking income decreased $876 million primarily

driven by lower servicing income and lower core production

revenue, partially offset by lower representations and warranties

provision.

Other loss decreased $2.0 billion due to lower negative fair value

adjustments on our structured liabilities of $649 million

compared to negative fair value adjustments of $5.1 billion in

2012. The prior year included gains of $1.6 billion related to

debt repurchases and exchanges of trust preferred securities.

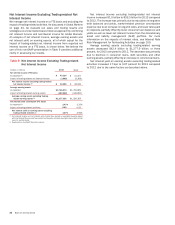

Provision for Credit Losses

The provision for credit losses decreased $4.6 billion to $3.6

billion for 2013 compared to 2012. The provision for credit losses

was $4.3 billion lower than net charge-offs for 2013, resulting in

a reduction in the allowance for credit losses due to continued

improvement in the home loans and credit card portfolios. This

compared to a reduction of $6.7 billion in the allowance for credit

losses for the prior year. If the economy and our asset quality

continue to improve, we anticipate additional reductions in the

allowance for credit losses in future periods, although at a

significantly lower level than in 2013.

Net charge-offs totaled $7.9 billion, or 0.87 percent of average

loans and leases for 2013 compared to $14.9 billion, or 1.67

percent for 2012. The decrease in net charge-offs was primarily

driven by credit quality improvement across all major portfolios.

Also, the prior year included charge-offs associated with the

National Mortgage Settlement and loans discharged in Chapter 7

bankruptcy due to the implementation of regulatory guidance.

Given improving trends in delinquencies and the Home Price Index,

absent any unexpected changes in the economy, we expect net

charge-offs to continue to improve in 2014, but at a slower pace

than 2013. For more information on the provision for credit losses,

see Provision for Credit Losses on page 100.