Bank of America 2013 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

82 Bank of America 2013

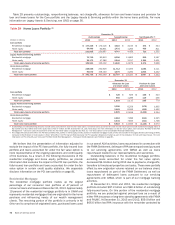

Table 34 presents the unpaid principal balance, carrying value, related valuation allowance and the net carrying value as a percentage

of the unpaid principal balance for the PCI loan portfolio.

Table 34 Purchased Credit-impaired Loan Portfolio

December 31, 2013

(Dollars in millions)

Unpaid

Principal

Balance

Carrying

Value

Related

Valuation

Allowance

Carrying

Value Net of

Valuation

Allowance

Percent of

Unpaid

Principal

Balance

Residential mortgage $ 19,558 $ 18,672 $ 1,446 $ 17,226 88.08%

Home equity 6,523 6,593 1,047 5,546 85.02

Total purchased credit-impaired loan portfolio $ 26,081 $ 25,265 $ 2,493 $ 22,772 87.31

December 31, 2012

Residential mortgage $ 18,069 $ 17,451 $ 3,108 $ 14,343 79.38%

Home equity 8,434 8,667 2,428 6,239 73.97

Total purchased credit-impaired loan portfolio $ 26,503 $ 26,118 $ 5,536 $ 20,582 77.66

The total PCI unpaid principal balance decreased $422 million,

or two percent, in 2013 primarily driven by liquidations, including

sales, payoffs, paydowns and write-offs, partially offset by the $5.3

billion of loans repurchased in connection with the FNMA

Settlement.

Of the unpaid principal balance of $26.1 billion at

December 31, 2013, $4.7 billion was 180 days or more past due,

including $4.6 billion of first-lien mortgages and $91 million of

home equity loans. Of the $21.4 billion that was less than 180

days past due, $18.4 billion, or 86 percent of the total unpaid

principal balance was current based on the contractual terms while

$2.0 billion, or nine percent, was in early stage delinquency.

During 2013, we recorded a provision benefit of $707 million

for the PCI loan portfolio including a provision benefit of $552

million for residential mortgage and a provision benefit of $155

million for home equity. This compared to a provision benefit of

$103 million in 2012. The provision benefit in 2013 was primarily

driven by an improvement in our home price outlook.

The PCI valuation allowance declined $3.0 billion during 2013

due to write-offs in the PCI loan portfolio of $1.2 billion in home

equity and $1.1 billion in residential mortgage, and a provision

benefit of $707 million for the PCI loan portfolio. Write-offs during

2013 included certain home equity PCI loans that were ineligible

for the National Mortgage Settlement, but had similar

characteristics as the eligible loans and the expectation of future

cash proceeds was considered remote.

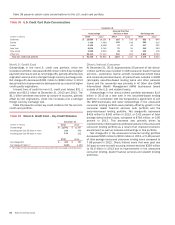

Purchased Credit-impaired Residential Mortgage Loan

Portfolio

The PCI residential mortgage loan portfolio represented 74 percent

of the total PCI loan portfolio at December 31, 2013. Those loans

to borrowers with a refreshed FICO score below 620 represented

52 percent of the PCI residential mortgage loan portfolio at

December 31, 2013. Loans with a refreshed LTV greater than

90 percent, after consideration of purchase accounting

adjustments and the related valuation allowance, represented 39

percent of the PCI residential mortgage loan portfolio and 51

percent based on the unpaid principal balance at December 31,

2013. Table 35 presents outstandings net of purchase accounting

adjustments and before the related valuation allowance, by certain

state concentrations.

Table 35 Outstanding Purchased Credit-impaired Loan

Portfolio – Residential Mortgage State

Concentrations

December 31

(Dollars in millions) 2013 2012

California $ 8,180 $ 9,238

Florida (1) 1,750 1,797

Virginia 760 715

Maryland 728 417

Texas 433 192

Other U.S./Non-U.S. 6,821 5,092

Total $ 18,672 $ 17,451

(1) In this state, foreclosure requires a court order following a legal proceeding (judicial state).

Pay option adjustable-rate mortgages (ARMs), which are

included in the PCI residential mortgage portfolio, have interest

rates that adjust monthly and minimum required payments that

adjust annually, subject to resetting if minimum payments are

made and deferred interest limits are reached. Annual payment

adjustments are subject to a 7.5 percent maximum change. To

ensure that contractual loan payments are adequate to repay a

loan, the fully-amortizing loan payment amount is re-established

after the initial five- or ten-year period and again every five years

thereafter. These payment adjustments are not subject to the 7.5

percent limit and may be substantial due to changes in interest

rates and the addition of unpaid interest to the loan balance.

Payment advantage ARMs have interest rates that are fixed for an

initial period of five years. Payments are subject to reset if the

minimum payments are made and deferred interest limits are

reached. If interest deferrals cause a loan’s principal balance to

reach a certain level within the first 10 years of the life of the loan,

the payment is reset to the interest-only payment; then at the 10-

year point, the fully-amortizing payment is required.

The difference between the frequency of changes in a loan’s

interest rates and payments along with a limitation on changes in

the minimum monthly payments of 7.5 percent per year can result

in payments that are not sufficient to pay all of the monthly interest

charges (i.e., negative amortization). Unpaid interest is added to

the loan balance until the loan balance increases to a specified

limit, which can be no more than 115 percent of the original loan

amount, at which time a new monthly payment amount adequate

to repay the loan over its remaining contractual life is established.