Bank of America 2013 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2013 109

Interest Rate Risk Management for Nontrading

Activities

The following discussion presents net interest income excluding

the impact of trading-related activities.

Interest rate risk represents the most significant market risk

exposure to our nontrading balance sheet. Interest rate risk is

measured as the potential change in net interest income caused

by movements in market interest rates. Client-facing activities,

primarily lending and deposit-taking, create interest rate sensitive

positions on our balance sheet.

We prepare forward-looking forecasts of net interest income.

The baseline forecast takes into consideration expected future

business growth, ALM positioning and the direction of interest rate

movements as implied by the market-based forward curve. We

then measure and evaluate the impact that alternative interest

rate scenarios have on the baseline forecast in order to assess

interest rate sensitivity under varied conditions. The net interest

income forecast is frequently updated for changing assumptions

and differing outlooks based on economic trends, market

conditions and business strategies. Thus, we continually monitor

our balance sheet position in an effort to maintain an acceptable

level of exposure to interest rate changes.

The interest rate scenarios that we analyze incorporate balance

sheet assumptions such as loan and deposit growth and pricing,

changes in funding mix, product repricing and maturity

characteristics. Our overall goal is to manage interest rate risk so

that movements in interest rates do not significantly adversely

affect earnings and capital.

Table 68 presents the spot and 12-month forward rates used

in our baseline forecasts at December 31, 2013 and 2012.

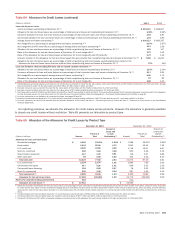

Table 68 Forward Rates

December 31, 2013

Federal

Funds

Three-

Month

LIBOR

10-Year

Swap

Spot rates 0.25% 0.25% 3.09%

12-month forward rates 0.25 0.43 3.52

December 31, 2012

Spot rates 0.25% 0.31% 1.84%

12-month forward rates 0.25 0.37 2.10

Table 69 shows the pre-tax dollar impact to forecasted net

interest income over the next 12 months from December 31, 2013

and 2012, resulting from instantaneous parallel and non-parallel

shocks to the market-based forward curve. Periodically, we

evaluate the scenarios presented to ensure that they are

meaningful in the context of the current rate environment. For

further discussion of net interest income excluding the impact of

trading-related activities, see page 30.

During 2013, the 10-year Treasury rate increased more than

120 bps. We continue to be asset sensitive to both a parallel move

in interest rates and to a lesser degree a long-end led steepening

of the yield curve. Additionally, rising interest rates impact the fair

value of debt securities and, accordingly, for debt securities

classified as AFS, may adversely affect accumulated OCI and thus

capital levels.

Table 69 Estimated Net Interest Income Excluding

Trading-related Net Interest Income

(Dollars in millions) Short

Rate (bps)

Long

Rate (bps)

December 31

Curve Change 2013 2012

Parallel Shifts

+100 bps

instantaneous shift +100 +100 $ 3,229 $ 4,350

-50 bps

instantaneous shift -50 -50 (1,616) (2,322)

Flatteners

Short end

instantaneous change +100 — 2,210 2,130

Long end

instantaneous change — -50 (641) (1,669)

Steepeners

Short end

instantaneous change -50 — (937) (648)

Long end

instantaneous change — +100 1,066 2,238

The sensitivity analysis in Table 69 assumes that we take no

action in response to these rate shocks. As part of our ALM

activities, we use securities, residential mortgages, and interest

rate and foreign exchange derivatives in managing interest rate

sensitivity.