Bank of America 2013 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

70 Bank of America 2013

We fund a substantial portion of our lending activities through

our deposits, which were $1.12 trillion and $1.11 trillion at

December 31, 2013 and 2012. Deposits are primarily generated

by our CBB, GWIM and Global Banking segments. These deposits

are diversified by clients, product type and geography, and the

majority of our U.S. deposits are insured by the FDIC. We consider

a substantial portion of our deposits to be a stable, low-cost and

consistent source of funding. We believe this deposit funding is

generally less sensitive to interest rate changes, market volatility

or changes in our credit ratings than wholesale funding sources.

Our lending activities may also be financed through secured

borrowings, including credit card securitizations and

securitizations with GSEs, the FHA and private-label investors, as

well as FHLB loans.

Our trading activities in other regulated entities are primarily

funded on a secured basis through securities lending and

repurchase agreements and these amounts will vary based on

customer activity and market conditions. We believe funding these

activities in the secured financing markets is more cost-efficient

and less sensitive to changes in our credit ratings than unsecured

financing. Repurchase agreements are generally short-term and

often overnight. Disruptions in secured financing markets for

financial institutions have occurred in prior market cycles which

resulted in adverse changes in terms or significant reductions in

the availability of such financing. We manage the liquidity risks

arising from secured funding by sourcing funding globally from a

diverse group of counterparties, providing a range of securities

collateral and pursuing longer durations, when appropriate. For

more information on secured financing agreements, see Note 10

– Federal Funds Sold or Purchased, Securities Financing

Agreements and Short-term Borrowings to the Consolidated

Financial Statements.

We issue the majority of our long-term unsecured debt at the

parent company. During 2013, we issued $31.4 billion of long-

term unsecured debt, including structured liabilities of $8.4 billion.

We may also issue long-term unsecured debt through BANA in a

variety of maturities and currencies to achieve cost-efficient

funding and to maintain an appropriate maturity profile. During

2013, we issued $2.5 billion of unsecured long-term debt through

BANA. While the cost and availability of unsecured funding may be

negatively impacted by general market conditions or by matters

specific to the financial services industry or the Corporation, we

seek to mitigate refinancing risk by actively managing the amount

of our borrowings that we anticipate will mature within any month

or quarter.

In 2013, we redeemed $9.0 billion of certain senior notes

maturing in 2014 through tender offers. In January 2014, we

issued $1.25 billion of 2.6% notes due January 2019, $400 million

of floating-rate notes due January 2019, $2.5 billion of 4.125%

notes due January 2024 and $2.0 billion of 5.0% notes due

January 2044. The Corporation converted substantially all of this

newly issued fixed-rate debt to floating-rate exposure with

derivative transactions.

Table 22 presents our long-term debt by major currency at

December 31, 2013 and 2012.

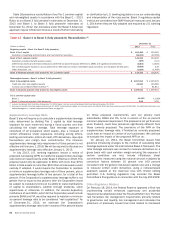

Table 22 Long-term Debt by Major Currency

December 31

(Dollars in millions) 2013 2012

U.S. Dollar $ 176,294 $ 180,329

Euro 46,029 58,985

British Pound 9,772 11,126

Japanese Yen 9,115 12,749

Canadian Dollar 2,402 3,560

Australian Dollar 1,870 2,760

Swiss Franc 1,274 1,917

Other 2,918 4,159

Total long-term debt $ 249,674 $ 275,585

Total long-term debt decreased $25.9 billion, or nine percent,

in 2013, primarily driven by maturities outpacing new issuances.

This reflects our ongoing initiative to reduce our debt balances

over time and we anticipate that debt levels will continue to decline

through 2014, although at a slower pace than 2013. We may, from

time to time, purchase outstanding debt instruments in various

transactions, depending on prevailing market conditions, liquidity

and other factors. In addition, our other regulated entities may

make markets in our debt instruments to provide liquidity for

investors. For more information on long-term debt funding, see

Note 11 – Long-term Debt to the Consolidated Financial

Statements.

We use derivative transactions to manage the duration, interest

rate and currency risks of our borrowings, considering the

characteristics of the assets they are funding. For further details

on our ALM activities, see Interest Rate Risk Management for

Nontrading Activities on page 109.

We also diversify our unsecured funding sources by issuing

various types of debt instruments including structured liabilities,

which are debt obligations that pay investors returns linked to other

debt or equity securities, indices, currencies or commodities. We

typically hedge the returns we are obligated to pay on these

liabilities with derivative positions and/or investments in the

underlying instruments, so that from a funding perspective, the

cost is similar to our other unsecured long-term debt. We could

be required to settle certain structured liability obligations for cash

or other securities prior to maturity under certain circumstances,

which we consider for liquidity planning purposes. We believe,

however, that a portion of such borrowings will remain outstanding

beyond the earliest put or redemption date. We had outstanding

structured liabilities with a carrying value of $48.4 billion and

$51.7 billion at December 31, 2013 and 2012.

Substantially all of our senior and subordinated debt

obligations contain no provisions that could trigger a requirement

for an early repayment, require additional collateral support, result

in changes to terms, accelerate maturity or create additional

financial obligations upon an adverse change in our credit ratings,

financial ratios, earnings, cash flows or stock price.