Bank of America 2013 Annual Report Download - page 242

Download and view the complete annual report

Please find page 242 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

240 Bank of America 2013

In July 2013, U.S. banking regulators issued a notice of

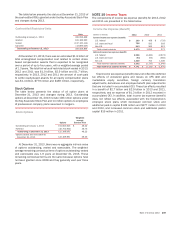

proposed rulemaking to modify the supplementary leverage ratio

minimum requirements under Basel 3 effective in 2018. This

proposal would only apply to BHCs with more than $700 billion in

total assets or more than $10 trillion in total assets under custody.

If adopted, it would require the Corporation to maintain a minimum

supplementary leverage ratio of three percent, plus a

supplementary leverage buffer of two percent, for a total of five

percent. If the Corporation’s supplementary leverage buffer is not

greater than or equal to two percent, then the Corporation would

be subject to mandatory limits on its ability to make distributions

of capital to shareholders, whether through dividends, stock

repurchases or otherwise. In addition, the insured depository

institutions of such BHCs, which for the Corporation would include

primarily BANA and FIA, would be required to maintain a minimum

six percent leverage ratio to be considered “well capitalized.” The

proposal is not yet final and, when finalized, could have provisions

significantly different from those currently proposed.

On January 12, 2014, the Basel Committee issued final

guidance introducing changes to the method of calculating total

leverage exposure under the international Basel 3 framework. The

total leverage exposure was revised to measure derivatives on a

gross basis with cash variation margin reducing the exposure if

certain conditions are met, include off-balance sheet

commitments measured using the notional amount multiplied by

conversion factors between 10 percent and 100 percent

consistent with the general risk-based capital rules and a change

to measure written credit derivatives using a notional-based

approach capped at the maximum loss with limited netting

permitted. U.S. banking regulators may consider the Basel

Committee’s final guidance in connection with the July 2013 NPR.

Basel 3 Liquidity Standards

The Basel Committee has issued two liquidity risk-related

standards that are considered part of the Basel 3 liquidity

standards: the Liquidity Coverage Ratio (LCR) and the Net Stable

Funding Ratio (NSFR). The LCR is calculated as the amount of a

financial institution’s unencumbered, high-quality, liquid assets

relative to the net cash outflows the institution could encounter

under a 30-day period of significant liquidity stress, expressed as

a percentage. The Basel Committee’s liquidity risk-related

standards do not directly apply to U.S. financial institutions

currently, and would only apply once U.S. rules are finalized by the

U.S. banking regulators.

On October 24, 2013, the U.S. banking regulators jointly

proposed regulations that would implement LCR requirements for

the largest U.S. financial institutions on a consolidated basis and

for their subsidiary depository institutions with total assets greater

than $10 billion. Under the proposal, an initial minimum LCR of

80 percent would be required in January 2015, and would

thereafter increase in 10 percentage point increments annually

through January 2017. These minimum requirements would be

applicable to the Corporation on a consolidated basis and at its

insured depository institutions, including BANA, FIA and Bank of

America California, N.A.

On January 12, 2014, the Basel Committee issued for

comment a revised NSFR, the standard that is intended to reduce

funding risk over a longer time horizon. The NSFR is designed to

ensure an appropriate amount of stable funding, generally capital

and liabilities maturing beyond one year, given the mix of assets

and off-balance sheet items. The revised proposal would align the

NSFR to some of the 2013 revisions to the LCR and give more

credit to a wider range of funding. The proposal also includes

adjustments to the stable funding required for certain types of

assets, some of which reduce the stable funding requirement and

some of which increase it. The Basel Committee expects to

complete the NSFR recalibration in 2014 and expects the minimum

standard to be in place by 2018.

Other Regulatory Matters

On February 18, 2014, the Federal Reserve approved a final rule

implementing certain enhanced supervisory and prudential

requirements established under the Dodd-Frank Wall Street

Reform and Consumer Protection Act. The final rule formalizes risk

management requirements primarily related to governance and

liquidity risk management and reiterates the provisions of

previously issued final rules related to risk-based and leverage

capital and stress test requirements. Also, a debt-to-equity limit

may be enacted for an individual BHC if determined to pose a grave

threat to the financial stability of the U.S., at the discretion of the

Financial Stability Oversight Council (FSOC) or the Federal Reserve

on behalf of the FSOC.

The Federal Reserve requires the Corporation’s banking

subsidiaries to maintain reserve balances based on a percentage

of certain deposits. Average daily reserve balance requirements

for the Corporation by the Federal Reserve were $16.6 billion and

$16.3 billion for 2013 and 2012. Currency and coin residing in

branches and cash vaults (vault cash) are used to partially satisfy

the reserve requirement. The average daily reserve balances, in

excess of vault cash, held with the Federal Reserve amounted to

$7.8 billion and $7.9 billion for 2013 and 2012. As of

December 31, 2013 and 2012, the Corporation had cash in the

amount of $6.0 billion and $8.5 billion, and securities with a fair

value of $8.4 billion and $5.9 billion that were segregated in

compliance with securities regulations or deposited with clearing

organizations.

The primary sources of funds for cash distributions by the

Corporation to its shareholders are capital distributions received

from its banking subsidiaries, BANA and FIA. In 2013, the

Corporation received $8.5 billion in dividends from BANA. BANA

and FIA returned capital of $8.7 billion to the Corporation in 2013.

In 2014, BANA can declare and pay dividends of $8.0 billion to

the Corporation plus an additional amount equal to its retained

net profits for 2014 up to the date of any dividend declaration.

The other subsidiary national banks returned capital of $1.4 billion

to the Corporation in 2013. Bank of America California, N.A. can

pay dividends of $396 million in 2014 plus an additional amount

equal to its retained net profits for 2014 up to the date of any

such dividend declaration. The amount of dividends that each

subsidiary bank may declare in a calendar year is the subsidiary

bank’s net profits for that year combined with its retained net

profits for the preceding two years. Retained net profits, as defined

by the OCC, consist of net income less dividends declared during

the period.