Bank of America 2013 Annual Report Download - page 266

Download and view the complete annual report

Please find page 266 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

264 Bank of America 2013

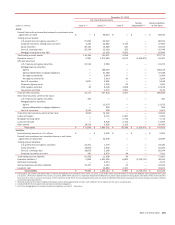

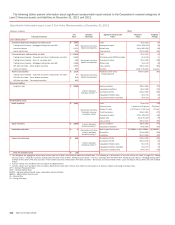

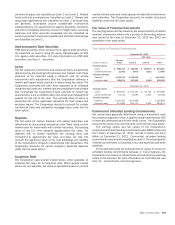

In the tables above, instruments backed by residential and

commercial real estate assets include RMBS, CMBS, whole loans,

mortgage CDOs and net monoline exposure. Commercial loans,

debt securities and other includes corporate CLOs and CDOs,

commercial loans and bonds, and securities backed by non-real

estate assets. Structured liabilities primarily include equity-linked

notes that are accounted for under the fair value option.

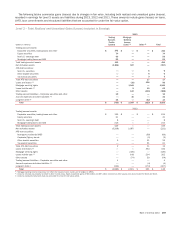

In addition to the instruments in the tables above, the

Corporation held $767 million and $1.2 billion of instruments at

December 31, 2013 and 2012 consisting primarily of certain direct

private equity investments and private equity funds that were

classified as Level 3 and reported within other assets. Valuations

of direct private equity investments are based on the most recent

company financial information. Inputs generally include market

and acquisition comparables, entry level multiples, as well as other

variables. The Corporation selects a valuation methodology (e.g.,

market comparables) for each investment and, in certain

instances, multiple inputs are weighted to derive the most

representative value. Discounts are applied as appropriate to

consider the lack of liquidity and marketability versus publicly-

traded companies. For private equity funds, fair value is determined

using the net asset value as provided by the individual fund’s

general partner.

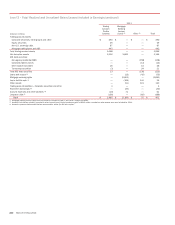

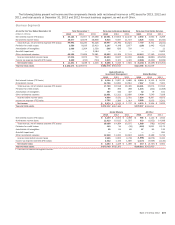

The Corporation uses multiple market approaches in valuing

certain of its Level 3 financial instruments. For example, market

comparables and discounted cash flows are used together. For a

given product, such as corporate debt securities, market

comparables may be used to estimate some of the unobservable

inputs and then these inputs are incorporated into a discounted

cash flow model. Therefore, the balances disclosed encompass

both of these techniques.

The level of aggregation and diversity within the products

disclosed in the tables result in certain ranges of inputs being

wide and unevenly distributed across asset and liability categories.

At December 31, 2013, weighted averages are disclosed for all

loans, securities, structured liabilities and net derivative assets.

At December 31, 2012, weighted averages were disclosed for all

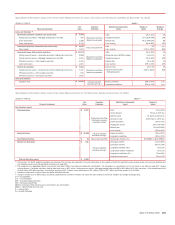

loans and securities.

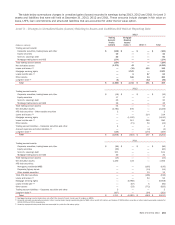

For credit derivatives, the range of credit spreads represented

positions with varying levels of default risk to the underlying

instruments. The lower end of the credit spread range typically

represented shorter-dated instruments and those with better

perceived credit risk. The higher end of the range represented

longer-dated instruments and those referencing debt issuances

that were more likely to be impaired or nonperforming. At

December 31, 2012, the majority of inputs were concentrated in

the lower end of the range. Similarly, the spread to index could

vary significantly based on the risk of the instrument. The spread

will be positive for instruments that have a higher risk of default

than the index (which is based on a weighted average of its

components) and negative for instruments that have a lower risk

of default than the index. At December 31, 2012, inputs were

distributed evenly throughout the range for spread to index. In

addition, for yield and credit correlation, the majority of the inputs

were concentrated in the center of the range. Inputs were

concentrated in the middle to lower end of the range for upfront

points. The range for loss severity reflected exposures that were

concentrated in the middle to upper end of the range while the

ranges for prepayment speed and default rates reflected

exposures that were concentrated in the lower end of the range.

For equity derivatives at December 31, 2012, including those

embedded in long-term debt, the range for equity correlation

represented exposure primarily concentrated toward the upper end

of the range. The range for long-dated volatilities represented

exposure primarily concentrated toward the lower end of the range.

For interest rate derivatives, the diversity in the portfolio was

reflected in wide ranges of inputs because the variety of currencies

and tenors of the transactions required the use of numerous

foreign exchange and interest rate curves. Since foreign exchange

and interest rate correlations were measured between curves and

across the various tenors on the same curve, the range of potential

values could include both negative and positive values. For the

correlation (IR/IR) range, the exposure represented the valuation

of interest rate correlations on less liquid pairings and was

concentrated at the upper end of the range at December 31, 2012.

For the correlation (FX/IR) range, the exposure was the sensitivity

to a broad mix of interest rate and foreign exchange correlations

and was distributed evenly throughout the range at December 31,

2012. For long-dated inflation rates and volatilities as well as long-

dated volatilities (FX), the inputs were concentrated in the middle

of the range.

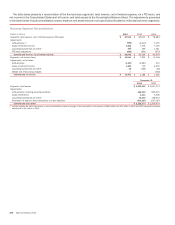

For more information on the inputs and techniques used in the

valuation of MSRs, see Note 23 – Mortgage Servicing Rights.