Bank of America 2013 Annual Report Download - page 272

Download and view the complete annual report

Please find page 272 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

280 -

281

281 -

282

282 -

283

-

284

|

|

270 Bank of America 2013

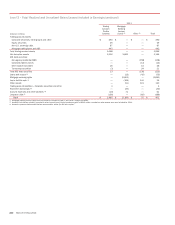

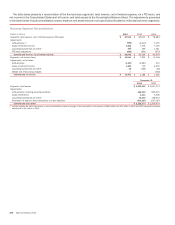

NOTE 23 Mortgage Servicing Rights

The Corporation accounts for consumer MSRs at fair value with

changes in fair value recorded in mortgage banking income (loss)

in the Consolidated Statement of Income. The Corporation

manages the risk in these MSRs with securities including MBS

and U.S. Treasuries, as well as certain derivatives such as options

and interest rate swaps, which are not designated as accounting

hedges. The securities used to manage the risk in the MSRs are

classified in other assets with changes in the fair value of the

securities and the related interest income recorded in mortgage

banking income (loss).

The table below presents activity for residential mortgage and

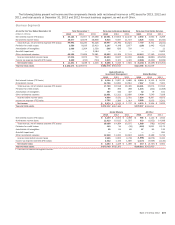

home equity MSRs for 2013 and 2012. Commercial and

residential reverse MSRs, which are carried at the lower of cost

or market value and accounted for using the amortization method,

totaled $10 million and $135 million at December 31, 2013 and

2012, and are not included in the tables in this Note.

Rollforward of Mortgage Servicing Rights

(Dollars in millions) 2013 2012

Balance, January 1 $ 5,716 $ 7,378

Additions 472 374

Sales (2,044) (122)

Amortization of expected cash flows (1) (1,043) (1,484)

Impact of changes in interest rates and other market

factors (2) 1,524 (867)

Model and other cash flow assumption changes: (3)

Projected cash flows, primarily due to (increases)

decreases in costs to service loans (27) 443

Impact of changes in the Home Price Index (398) (112)

Impact of changes to the prepayment model 609 435

Other model changes (4) 233 (329)

Balance, December 31 $ 5,042 $ 5,716

Mortgage loans serviced for investors (in billions) $ 550 $ 1,045

(1) Represents the net change in fair value of the MSR asset due to the recognition of modeled

cash flows.

(2) These amounts reflect the changes in modeled MSR fair value primarily due to observed changes

in interest rates, volatility, spreads and the shape of the forward swap curve.

(3) These amounts reflect periodic adjustments to the valuation model to reflect changes in the

modeled relationship between inputs and their impact on projected cash flows as well as

changes in certain cash flow assumptions such as cost to service and ancillary income per

loan.

(4) These amounts include the impact of periodic recalibrations of the model to reflect changes in

the relationship between market interest rate spreads and projected cash flows. Also included

is a decrease of $497 million for 2012 due to changes in OAS rate inputs.

The Corporation primarily uses an OAS valuation approach

which factors in prepayment risk to determine the fair value of

MSRs. This approach consists of projecting servicing cash flows

under multiple interest rate scenarios and discounting these cash

flows using risk-adjusted discount rates. In addition to updating

the valuation model for interest, discount and prepayment rates,

periodic adjustments are made to recalibrate the valuation model

for factors used to project cash flows. The changes to the factors

capture the effect of variances related to actual versus estimated

servicing proceeds.

The $2.0 billion of MSR sales during 2013 primarily relate to

transfers completed under definitive agreements the Corporation

entered into during the year to sell certain MSRs. The transfers

of the MSRs occurred in stages throughout 2013, and all of the

servicing encompassed by these agreements had been

transferred as of December 31, 2013.

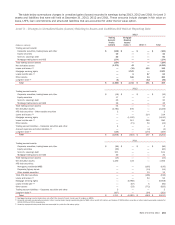

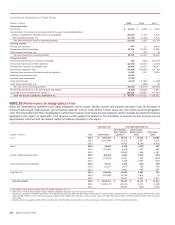

Significant economic assumptions in estimating the fair value

of MSRs at December 31, 2013 and 2012 are presented below.

The change in fair value as a result of changes in OAS rates is

included within “Model and other cash flow assumption changes”

in the Rollforward of Mortgage Servicing Rights table. The weighted-

average life is not an input in the valuation model but is a product

of both changes in market rates of interest and changes in model

and other cash flow assumptions. The weighted-average life

represents the average period of time that the MSRs’ cash flows

are expected to be received. Absent other changes, an increase

(decrease) to the weighted-average life would generally result in

an increase (decrease) in the fair value of the MSRs.

Significant Economic Assumptions

December 31

2013 2012

Fixed Adjustable Fixed Adjustable

Weighted-average OAS 3.97% 7.61% 4.00% 6.63%

Weighted-average life, in years 5.70 2.86 3.65 2.10

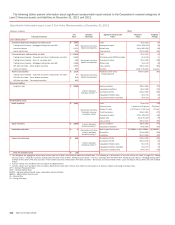

The table below presents the sensitivity of the weighted-

average lives and fair value of MSRs to changes in modeled

assumptions. These sensitivities are hypothetical and should be

used with caution. As the amounts indicate, changes in fair value

based on variations in assumptions generally cannot be

extrapolated because the relationship of the change in assumption

to the change in fair value may not be linear. Also, the effect of a

variation in a particular assumption on the fair value of MSRs that

continue to be held by the Corporation is calculated without

changing any other assumption. In reality, changes in one factor

may result in changes in another, which might magnify or counteract

the sensitivities. The below sensitivities do not reflect any hedge

strategies that may be undertaken to mitigate such risk.

Sensitivity Impacts

December 31, 2013

Change in

Weighted-average Lives

(Dollars in millions) Fixed Adjustable

Change in

Fair Value

Prepayment rates

Impact of 10% decrease 0.24 years 0.20 years $ 266

Impact of 20% decrease 0.51 0.42 558

Impact of 10% increase (0.22) (0.17) (244)

Impact of 20% increase (0.42) (0.32) (469)

OAS level

Impact of 100 bps decrease $ 268

Impact of 200 bps decrease 561

Impact of 100 bps increase (247)

Impact of 200 bps increase (474)