Bank of America 2013 Annual Report Download - page 176

Download and view the complete annual report

Please find page 176 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

174 Bank of America 2013

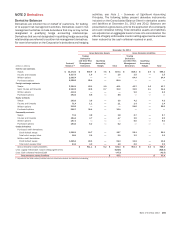

Valuation Adjustments on Derivatives

The Corporation records credit risk valuation adjustments on

derivatives in order to properly reflect the credit quality of the

counterparties and its own credit quality. The Corporation

calculates valuation adjustments on derivatives based on a

modeled expected exposure that incorporates current market risk

factors. The exposure also takes into consideration credit

mitigants such as enforceable master netting agreements and

collateral. CDS spread data is used to estimate the default

probabilities and severities that are applied to the exposures.

Where no observable credit default data is available for

counterparties, the Corporation uses proxies and other market

data to estimate default probabilities and severity.

Valuation adjustments on derivatives are affected by changes

in market spreads, non-credit related market factors such as

interest rate and currency changes that affect the expected

exposure, and other factors like changes in collateral

arrangements and partial payments. Credit spreads and non-credit

factors can move independently. For example, for an interest rate

swap, changes in interest rates may increase the expected

exposure which would increase the counterparty credit valuation

adjustment (CVA). Independently, counterparty credit spreads may

tighten, which would result in an offsetting decrease to CVA.

The Corporation may enter into risk management activities to

offset market driven exposures. The Corporation often hedges the

counterparty spread risk in CVA with CDS and often hedges the

other market risks in both CVA and DVA primarily with currency and

interest rate swaps. Since the components of the valuation

adjustments on derivatives move independently and the

Corporation may not hedge all of the market driven exposures, the

effect of a hedge may increase the gross valuation adjustments

on derivatives or may result in a gross positive valuation

adjustment on derivatives becoming a negative adjustment (or the

reverse).

In 2013, the Corporation refined its methodology for calculating

CVA and DVA on a prospective basis, to adjust the way it values

mutual termination clauses in derivatives contracts and to more

fully incorporate the potential for the counterparties to default prior

to a change in their credit ratings. This change in estimate

increased CVA by $361 million and DVA by $433 million resulting

in a net positive earnings impact of $72 million at the time of the

change and is included in the results for 2013. The net CVA and

DVA excluding the impact of these refinements was a gain of $265

million and a loss of $508 million for 2013.

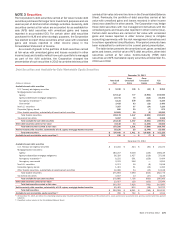

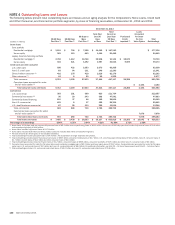

The table below presents CVA and DVA gains (losses), which

are recorded in trading account profits on a gross and net of hedge

basis.

Valuation Adjustments on Derivatives

2013 2012 2011

(Dollars in millions) Gross Net Gross Net Gross Net

Derivative assets (CVA) (1) $738 $(96)

$ 1,022 $ 291 $ (1,863) $ (606)

Derivative liabilities (DVA) (2) (39) (75) (2,212) (2,477) 1,385 1,000

(1) At December 31, 2013, 2012 and 2011, the cumulative CVA reduced the derivative assets balance by $1.6 billion, $2.4 billion and $2.8 billion, respectively.

(2) At December 31, 2013, 2012 and 2011, the cumulative DVA reduced the derivative liabilities balance by $803 million, $807 million and $2.4 billion, respectively.