Bank of America 2013 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2013 85

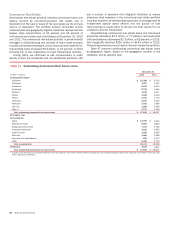

Table 40 presents certain state concentrations for the direct/indirect consumer loan portfolio.

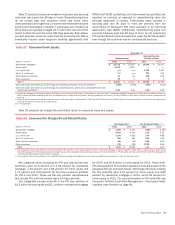

Table 40 Direct/Indirect State Concentrations

December 31

Outstandings

Accruing Past Due

90 Days or More Net Charge-offs

(Dollars in millions) 2013 2012 2013 2012 2013 2012

California $ 10,041 $ 10,793 $57

$53

$42 $ 102

Texas 7,850 7,239 66 41 32 64

Florida 7,634 7,363 25 37 41 88

New York 4,611 4,794 33 28 20 43

Georgia 2,564 2,491 16 31 14 30

Other U.S./Non-U.S. 49,492 50,525 211 355 196 436

Total direct/indirect loan portfolio $ 82,192 $ 83,205 $408 $ 545 $345 $ 763

Other Consumer

At December 31, 2013, approximately 60 percent of the $2.0

billion other consumer portfolio was associated with certain

consumer finance businesses that we previously exited. The

remainder is primarily leases within the consumer dealer financial

services portfolio included in CBB.

Consumer Loans Accounted for Under the Fair Value

Option

Outstanding consumer loans accounted for under the fair value

option totaled $2.2 billion at December 31, 2013 and were

comprised of residential mortgage loans that were previously

classified as held-for-sale, residential mortgage loans held in

consolidated variable interest entities (VIEs) and repurchases of

home equity loans. The loans that were previously classified as

held-for-sale were transferred to the residential mortgage portfolio

in connection with the decision to retain the loans. The fair value

option had been elected at the time of origination and the loans

continue to be measured at fair value after the reclassification. In

2013, we recorded net losses of $2 million resulting from changes

in the fair value of these loans, including gains of $41 million on

loans held in consolidated VIEs that were offset by losses recorded

on related long-term debt.

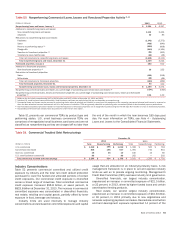

Nonperforming Consumer Loans, Leases and Foreclosed

Properties Activity

Table 41 presents nonperforming consumer loans, leases and

foreclosed properties activity during 2013 and 2012.

Nonperforming LHFS are excluded from nonperforming loans as

they are recorded at either fair value or the lower of cost or fair

value. Nonperforming loans do not include past due consumer

credit card loans, other unsecured loans and in general, consumer

non-real estate-secured loans (loans discharged in Chapter 7

bankruptcy are included) as these loans are typically charged off

no later than the end of the month in which the loan becomes

180 days past due. The charge-offs on these loans have no impact

on nonperforming activity and, accordingly, are excluded from this

table. The fully-insured loan portfolio is not reported as

nonperforming as principal repayment is insured. Additionally,

nonperforming loans do not include the PCI loan portfolio or loans

accounted for under the fair value option. For more information on

nonperforming loans, see Note 1 – Summary of Significant

Accounting Principles to the Consolidated Financial Statements.

During 2013, nonperforming consumer loans declined $3.6 billion

to $15.8 billion as outflows, including the impact of loan sales,

outpaced new inflows which continued to improve due to favorable

delinquency trends.

The outstanding balance of a real estate-secured loan that is

in excess of the estimated property value less costs to sell is

charged off no later than the end of the month in which the loan

becomes 180 days past due unless repayment of the loan is fully

insured. At December 31, 2013, $7.7 billion, or 47 percent of

nonperforming consumer real estate loans and foreclosed

properties had been written down to their estimated property value

less costs to sell, including $7.2 billion of nonperforming loans

180 days or more past due and $533 million of foreclosed

properties. In addition, at December 31, 2013, $5.9 billion, or 37

percent of nonperforming consumer loans were modified and are

now current after successful trial periods, or are current loans

classified as nonperforming loans in accordance with applicable

policies.

Foreclosed properties decreased $117 million in 2013 as

liquidations outpaced additions. PCI loans are excluded from

nonperforming loans as these loans were written down to fair value

at the acquisition date; however, once the underlying real estate

is acquired by the Corporation upon foreclosure of the delinquent

PCI loan, it is included in foreclosed properties. PCI-related

foreclosed properties increased $165 million in 2013. Not

included in foreclosed properties at December 31, 2013 was $1.4

billion of real estate that was acquired upon foreclosure of

delinquent FHA-insured loans. We hold this real estate on our

balance sheet until we convey these properties to the FHA. We

exclude these amounts from our nonperforming loans and

foreclosed properties activity as we expect we will be reimbursed

once the property is conveyed to the FHA for principal and, up to

certain limits, costs incurred during the foreclosure process and

interest incurred during the holding period. For more information

on the review of our foreclosure processes, see Off-Balance Sheet

Arrangements and Contractual Obligations – Servicing,

Foreclosure and Other Mortgage Matters on page 53.