Bank of America 2013 Annual Report Download - page 22

Download and view the complete annual report

Please find page 22 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

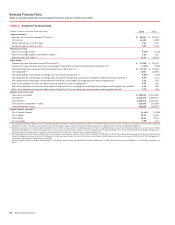

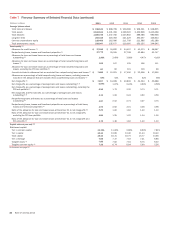

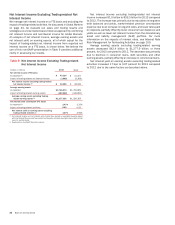

20 Bank of America 2013

Executive Summary

Business Overview

The Corporation is a Delaware corporation, a bank holding company

(BHC) and a financial holding company. When used in this report,

“the Corporation” may refer to Bank of America Corporation

individually, Bank of America Corporation and its subsidiaries, or

certain of Bank of America Corporation’s subsidiaries or affiliates.

Our principal executive offices are located in Charlotte, North

Carolina. Through our banking and various nonbanking

subsidiaries throughout the U.S. and in international markets, we

provide a diversified range of banking and nonbanking financial

services and products through five business segments: Consumer

& Business Banking (CBB), Consumer Real Estate Services (CRES),

Global Wealth & Investment Management (GWIM), Global Banking

and Global Markets, with the remaining operations recorded in All

Other. We operate our banking activities primarily under two

national bank charters: Bank of America, National Association

(Bank of America, N.A. or BANA) and FIA Card Services, National

Association (FIA Card Services, N.A. or FIA). On October 1, 2013,

we completed the merger of our Merrill Lynch & Co., Inc. (Merrill

Lynch) subsidiary into Bank of America Corporation. This merger

had no effect on the Merrill Lynch name or brand and is not

expected to have any effect on customers or clients. At

December 31, 2013, the Corporation had approximately $2.1

trillion in assets and approximately 242,000 full-time equivalent

employees.

As of December 31, 2013, we operated in all 50 states, the

District of Columbia and more than 40 countries. Our retail banking

footprint covers approximately 80 percent of the U.S. population

and we serve approximately 50 million consumer and small

business relationships with approximately 5,100 banking centers,

16,300 ATMs, nationwide call centers, and leading online

(www.bankofamerica.com) and mobile banking platforms. We offer

industry-leading support to more than three million small business

owners. We are a global leader in corporate and investment

banking and trading across a broad range of asset classes serving

corporations, governments, institutions and individuals around the

world.

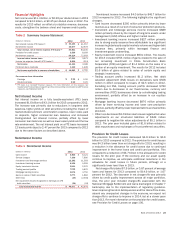

2013 Economic and Business Environment

In the U.S., economic growth continued in 2013, ending the year

in the midst of its fifth consecutive year of recovery. However, the

year ended amid uncertainty as to whether the upward trend in

economic performance would continue into 2014. Employment

gains were generally steady but moderate, and the unemployment

rate fell to 6.7 percent at year end, but with significant contribution

from a declining labor force participation rate. Retail sales grew

at a solid pace through most of 2013, and following extreme

weakness through mid-2013, service spending also displayed a

modest rebound late in the year. Core inflation fell in 2013 to

almost a full percentage point below the Board of Governors of

the Federal Reserve System’s (Federal Reserve) longer-term target

of two percent.

U.S. household net worth increased significantly in 2013.

Home prices rose approximately 12 percent in 2013, but showed

signs of deceleration late in the year, and equity markets surged.

U.S. Treasury yields rose over the course of the year amid

expectations that the Federal Reserve would adjust the pace of

its purchases of agency mortgage-backed securities (MBS) and

long-term U.S. Treasury securities if economic progress was

sustained.

Despite a partial federal government shutdown in October, the

impact on U.S. economic performance was minimal. The Federal

Reserve announced that it would begin to reduce its securities

purchases early in 2014, but would not raise its federal funds rate

target until significantly after the unemployment rate reached its

6.5 percent threshold. By year end, the U.S. Congress agreed on

a two-year budget framework that reduced fiscal uncertainty, and

pending implementation, restored some of the planned federal

sequester spending for 2014.

Internationally, Europe experienced significant economic

improvement in 2013. European financial anxieties eased,

reflected in sustained narrowing of bond spreads, following the

European Central Bank’s 2012 assertion of its role as lender of

last resort. Economic performance also improved, with the long

six-quarter recession in the European Union ending in the second

quarter of 2013, followed by modest growth and varied

performance in the second half of the year.

Monetary policies in Japan combined with the sharp

depreciation of the yen led to moderate economic expansion in

2013, but economic growth diminished in the second half of 2013.

In Japan, inflation rose gradually during the year, exceeding one

percent annualized by year end. However, doubts remained about

the sustainability of economic improvement in Japan in the

absence of clear plans for long-run economic reform. As China’s

government focused on issues beyond simply maximizing

economic growth, China’s gross domestic product growth in 2013

decelerated.

Additionally, growth rates in a number of emerging nations have

decreased, while select countries are also dealing with greater

social and political unrest and capital markets volatility. Following

the announcement of the Federal Reserve’s intent to reduce

securities purchases in mid-2013, investors increased

withdrawals of capital from certain emerging market countries,

impacting interest rates, foreign exchange rates and credit

spreads. These trends intensified as the Federal Reserve initiated

its securities purchases tapering actions in January 2014, and

investors became more concerned about the implications of a

slowing Chinese economy on its key trading partners. For more

information on our international exposure, see Non-U.S. Portfolio

on page 96.