Bank of America 2013 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2013 65

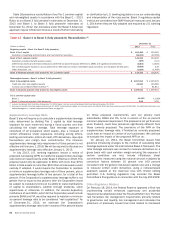

Changes to the composition of regulatory capital under Basel

3, such as recognizing the impact of unrealized gains or losses

on AFS debt securities in Tier 1 common capital, are subject to a

transition period where the impact is recognized in 20 percent

annual increments. These regulatory capital adjustments and

deductions will be fully implemented in 2018. The phase-in period

for the new minimum capital ratio requirements and related buffers

under Basel 3 is from January 1, 2014 through December 31,

2018. When presented on a fully phased-in basis, capital, risk-

weighted assets and the capital ratios assume all regulatory

capital adjustments and deductions are fully recognized.

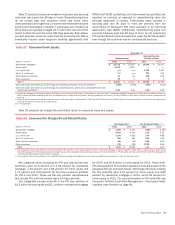

Table 17 summarizes how certain regulatory capital deductions

and adjustments will be transitioned from 2014 through 2018 for

Tier 1 common and Tier 1 capital.

Table 17 Summary of Certain Basel 3 Regulatory Capital Transition Provisions

Beginning on January 1 of each year 2014 2015 2016 2017 2018

Tier 1 common capital

Percent of total amount deducted from Tier 1 common capital includes: 20% 40% 60% 80% 100%

Deferred tax assets arising from net operating loss and tax credit carryforwards; intangibles, other than mortgage servicing rights and goodwill; defined benefit pension

fund net assets; net gains (losses) related to changes in own credit risk on liabilities, including derivatives, measured at fair value; direct and indirect investments

in own Tier 1 common capital instruments; certain amounts exceeding the threshold by 10 percent individually and 15 percent in aggregate

Percent of total amount used to adjust Tier 1 common capital includes (1): 80% 60% 40% 20% 0%

Net unrealized gains (losses) on AFS debt and certain marketable equity securities recorded in accumulated OCI; employee benefit plan adjustments recorded in

accumulated OCI

Tier 1 capital

Percent of total amount deducted from Tier 1 capital includes: 80% 60% 40% 20% 0%

Deferred tax assets arising from net operating loss and tax credit carryforwards; defined benefit pension fund net assets; net gains (losses) related to changes in own

credit risk on liabilities, including derivatives, measured at fair value

(1) Represents the phase-out percentage of the exclusion by year (e.g., 20 percent of net unrealized gains (losses) on AFS debt and certain marketable equity securities recorded in accumulated OCI

will be included in 2014).

In addition, Basel 3 revised the regulatory capital treatment for

Trust Securities, requiring them to be partially transitioned from

Tier 1 capital into Tier 2 capital in 2014 and 2015, until fully

excluded from Tier 1 capital in 2016, and partially transitioned

and excluded from Tier 2 capital beginning in 2016. The exclusion

from Tier 2 capital starts at 40 percent on January 1, 2016,

increasing 10 percent each year until the full amount is excluded

from Tier 2 capital beginning on January 1, 2022. As of

December 31, 2013, our qualifying Trust Securities were $5.8

billion (approximately 45 bps of Tier 1 capital) and will no longer

qualify as Tier 1 capital or Tier 2 capital beginning in 2016, subject

to the transition provisions previously described.

Standardized Approach

The Basel 3 Standardized approach measures risk-weighted

assets primarily for market risk and credit risk exposures.

Exposures subject to market risk, as defined under the rules, are

measured on the same basis as the Market Risk Final Rule,

described previously. Credit risk exposures are measured by

applying fixed risk weights to the exposure, determined based on

the characteristics of the exposure, such as type of obligor,

Organization for Economic Cooperation and Development (OECD)

country risk code and maturity, among others. Under the

Standardized approach, no distinction is made for variations in

credit quality for corporate exposures, and the economic benefit

of collateral is restricted to a limited list of eligible securities and

cash. Some key differences between the Standardized and

Advanced approaches are that the Advanced approach includes a

measure of operational risk and a credit valuation adjustment

(CVA) capital charge in credit risk and relies on internal analytical

models to measure credit risk-weighted assets, as more fully

described below. Under the Basel 3 Standardized approach, we

estimate our Tier 1 common capital ratio, on a fully phased-in

basis, to be just above nine percent at December 31, 2013.

Advanced Approach

Under the Basel 3 Advanced approach, risk-weighted assets are

determined primarily for market risk, credit risk and operational

risk. Market risk capital measurements are consistent with the

Standardized approach, except for securitization exposures, where

the Supervisory Formula Approach is also permitted, and certain

differences arising from the inclusion of the CVA capital charge in

the credit risk capital measurement. Credit risk exposures are

measured using advanced internal ratings-based models to

determine the applicable risk weight by estimating the probability

of default, loss-given default (LGD) and, in certain instances,

exposure at default (EAD). The analytical models primarily rely on

internal historical default and loss experience. Operational risk is

measured using advanced internal models which rely on both

internal and external operational loss experience and data. The

Basel 3 Advanced approach requires approval by the U.S.

regulatory agencies of our internal analytical models used to

calculate risk-weighted assets. If these models are not approved,

it would likely lead to an increase in our risk-weighted assets, which

in some cases could be significant.

Prior to calculating and assessing capital adequacy and

reporting regulatory capital ratios using Basel 3 Advanced

approach risk-weighted assets, we must receive notification of

approval to do so from the U.S banking regulators. Under the Basel

3 Advanced approach, we estimated our Tier 1 common capital

ratio, on a fully phased-in basis, to be 9.96 percent at

December 31, 2013. As of December 31, 2013, we estimated

that our Tier 1 common capital would be $132.3 billion and total

risk-weighted assets would be $1,329 billion, on a fully phased-

in basis. This assumes approval by U.S. banking regulators of our

internal analytical models, but does not include the benefit of the

removal of the surcharge applicable to the Comprehensive Risk

Measure (CRM). The calculations under Basel 3 require

management to make estimates, assumptions and interpre-

tations, including the probability of future events based on

historical experience. Realized results could differ from those

estimates and assumptions.