Bank of America 2013 Annual Report Download - page 268

Download and view the complete annual report

Please find page 268 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

-

280

-

281

-

282

-

283

-

284

|

|

266 Bank of America 2013

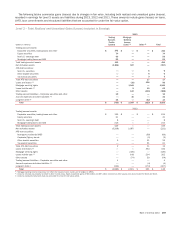

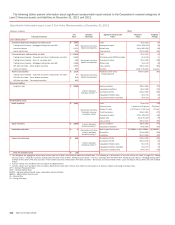

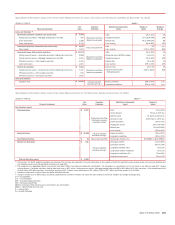

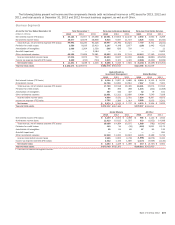

The table below presents information about significant unobservable inputs related to the Corporation’s nonrecurring Level 3 financial

assets and liabilities at December 31, 2013 and 2012.

Quantitative Information about Nonrecurring Level 3 Fair Value Measurements

December 31, 2013

(Dollars in millions) Inputs

Financial Instrument

Fair

Value

Valuation

Technique

Significant Unobservable

Inputs

Ranges of

Inputs

Weighted

Average

Instruments backed by residential real estate assets $ 5,240 Market comparables OREO discount 0% to 19% 8%

Loans and leases 5,240 Cost to sell 8% n/a

December 31, 2012

Instruments backed by residential real estate assets $ 9,932

Discounted cash

flow, Market

comparables

Yield 3% to 5% 3%

Loans held-for-sale 748 Prepayment speed 3% to 30% 15%

Loans and leases 9,184 Default rate 0% to 55% 7%

Loss severity 6% to 66% 48%

OREO discount 0% to 28% 15%

Cost to sell 8% n/a

Instruments backed by commercial real estate assets $ 388 Discounted cash

flow

Yield 4% to 13% 6%

Loans held-for-sale 388 Loss severity 24% to 88% 53%

n/a = not applicable

Instruments backed by residential real estate assets represent

residential mortgages where the loan has been written down to

the fair value of the underlying collateral or, in the case of LHFS,

are carried at the lower of cost or fair value. In addition to the

instruments disclosed in the table above, the Corporation holds

foreclosed residential properties where the fair value is based on

unadjusted third-party appraisals or broker price opinions.

Appraisals are generally conducted every 90 days. Factors

considered in determining the fair value include geographic sales

trends, the value of comparable surrounding properties as well as

the condition of the property.

NOTE 21 Fair Value Option

Loans and Loan Commitments

The Corporation elects to account for certain commercial loans

and loan commitments that exceed the Corporation’s single name

credit risk concentration guidelines under the fair value option.

Lending commitments, both funded and unfunded, are actively

managed and monitored and, as appropriate, credit risk for these

lending relationships may be mitigated through the use of credit

derivatives, with the Corporation’s public side credit view and

market perspectives determining the size and timing of the hedging

activity. These credit derivatives do not meet the requirements for

designation as accounting hedges and therefore are carried at fair

value with changes in fair value recorded in other income (loss).

Electing the fair value option allows the Corporation to carry these

loans and loan commitments at fair value, which is more consistent

with management’s view of the underlying economics and the

manner in which they are managed. In addition, election of the fair

value option allows the Corporation to reduce the accounting

volatility that would otherwise result from the asymmetry created

by accounting for the financial instruments at historical cost and

the credit derivatives at fair value. The Corporation also elected

the fair value option for certain residential mortgage loans that

were classified as held-for-sale and certain loans held in

consolidated VIEs. Of the changes in fair value of these loans,

gains of $315 million and $1.2 billion were attributable to changes

in borrower-specific credit risk in 2013 and 2012.

Loans Held-for-sale

The Corporation elects to account for residential mortgage LHFS,

commercial mortgage LHFS and other LHFS under the fair value

option with interest income on these LHFS recorded in other

interest income. These loans are actively managed and monitored

and, as appropriate, certain market risks of the loans may be

mitigated through the use of derivatives. The Corporation has

elected not to designate the derivatives as qualifying accounting

hedges and therefore they are carried at fair value with changes

in fair value recorded in other income (loss). The changes in fair

value of the loans are largely offset by changes in the fair value

of the derivatives. Of the changes in fair value of these loans,

gains of $225 million and $425 million were attributable to

changes in borrower-specific credit risk in 2013 and 2012. Election

of the fair value option allows the Corporation to reduce the

accounting volatility that would otherwise result from the

asymmetry created by accounting for the financial instruments at

the lower of cost or fair value and the derivatives at fair value. The

Corporation has not elected to account for other LHFS under the

fair value option primarily because these loans are floating-rate

loans that are not hedged using derivative instruments.

Loans Reported as Trading Account Assets

The Corporation elects to account for certain loans that are held

for the purpose of trading and risk-managed on a fair value basis

under the fair value option. An immaterial portion of the changes

in fair value of these loans was attributable to changes in borrower-

specific credit risk in 2013 and 2012.