Bank of America 2013 Annual Report Download - page 160

Download and view the complete annual report

Please find page 160 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

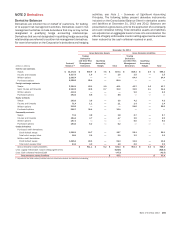

158 Bank of America 2013

equity and Legacy Assets & Servicing home equity. The classes

within the Credit Card and Other Consumer portfolio segment are

U.S. credit card, non-U.S. credit card, direct/indirect consumer and

other consumer. The classes within the Commercial portfolio

segment are U.S. commercial, commercial real estate, commercial

lease financing, non-U.S. commercial and U.S. small business

commercial.

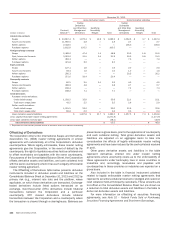

Purchased Credit-impaired Loans

The Corporation purchases loans with and without evidence of

credit quality deterioration since origination. Evidence of credit

quality deterioration as of the purchase date may include statistics

such as past due status, refreshed borrower credit scores and

refreshed loan-to-value (LTV) ratios, some of which are not

immediately available as of the purchase date. Purchased loans

with evidence of credit quality deterioration for which it is probable

that the Corporation will not receive all contractually required

payments receivable are accounted for as purchased credit-

impaired (PCI) loans. The excess of the cash flows expected to be

collected on PCI loans, measured as of the acquisition date, over

the estimated fair value is referred to as the accretable yield and

is recognized in interest income over the remaining life of the loan

using a level yield methodology. The difference between

contractually required payments as of the acquisition date and the

cash flows expected to be collected is referred to as the

nonaccretable difference. PCI loans that have similar risk

characteristics, primarily credit risk, collateral type and interest

rate risk, are pooled and accounted for as a single asset with a

single composite interest rate and an aggregate expectation of

cash flows. Once a pool is assembled, it is treated as if it was one

loan for purposes of applying the accounting guidance for PCI

loans. An individual loan is removed from a PCI loan pool if it is

sold, foreclosed, forgiven or the expectation of any future proceeds

is remote. When a loan is removed from a PCI loan pool and the

foreclosure or recovery value of the loan is less than the loan’s

carrying value, the difference is first applied against the PCI pool’s

nonaccretable difference. If the nonaccretable difference has been

fully utilized, only then is the PCI pool’s basis applicable to that

loan written-off against its valuation reserve; however, the integrity

of the pool is maintained and it continues to be accounted for as

if it was one loan.

The Corporation continues to estimate cash flows expected to

be collected over the life of the PCI loans using internal credit risk,

interest rate and prepayment risk models that incorporate

management’s best estimate of current key assumptions such as

default rates, loss severity and payment speeds. If, upon

subsequent evaluation, the Corporation determines it is probable

that the present value of the expected cash flows has decreased,

the PCI loan is considered to be further impaired resulting in a

charge to the provision for credit losses and a corresponding

increase to a valuation allowance included in the allowance for

loan and lease losses. The present value of the expected cash

flows is then recalculated each period, which may result in

additional impairment or a reduction of the valuation allowance.

If there is no valuation allowance and it is probable that there is

a significant increase in the present value of the expected cash

flows, the Corporation recalculates the amount of accretable yield

as the excess of the revised expected cash flows over the current

carrying value resulting in a reclassification from nonaccretable

difference to accretable yield. Reclassifications from

nonaccretable difference can also occur if there is a change in the

expected lives of the loans. The present value of the expected

cash flows is determined using the PCI loans’ effective interest

rate, adjusted for changes in the PCI loans’ interest rate indices.

Leases

The Corporation provides equipment financing to its customers

through a variety of lease arrangements. Direct financing leases

are carried at the aggregate of lease payments receivable plus

estimated residual value of the leased property less unearned

income. Leveraged leases, which are a form of financing leases,

are reported net of non-recourse debt. Unearned income on

leveraged and direct financing leases is accreted to interest

income over the lease terms using methods that approximate the

interest method.

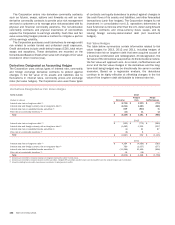

Allowance for Credit Losses

The allowance for credit losses, which includes the allowance for

loan and lease losses and the reserve for unfunded lending

commitments, represents management’s estimate of probable

losses inherent in the Corporation’s lending activities. The

allowance for loan and lease losses and the reserve for unfunded

lending commitments exclude amounts for loans and unfunded

lending commitments accounted for under the fair value option as

the fair values of these instruments reflect a credit component.

The allowance for loan and lease losses does not include amounts

related to accrued interest receivable, other than billed interest

and fees on credit card receivables, as accrued interest receivable

is reversed when a loan is placed on nonaccrual status. The

allowance for loan and lease losses represents the estimated

probable credit losses on funded consumer and commercial loans

and leases while the reserve for unfunded lending commitments,

including standby letters of credit and binding unfunded loan

commitments, represents estimated probable credit losses on

these unfunded credit instruments based on utilization

assumptions. Lending-related credit exposures deemed to be

uncollectible, excluding loans carried at fair value, are charged off

against these accounts. Write-offs on PCI loans on which there is

a valuation allowance are written-off against the valuation

allowance. For additional information, see the Purchased Credit-

impaired Loans in this Note. Cash recovered on previously charged

off amounts is recorded as a recovery to these accounts.

Management evaluates the adequacy of the allowance for credit

losses based on the combined total of the allowance for loan and

lease losses and the reserve for unfunded lending commitments.

The Corporation performs periodic and systematic detailed

reviews of its lending portfolios to identify credit risks and to

assess the overall collectability of those portfolios. The allowance

on certain homogeneous consumer loan portfolios, which

generally consist of consumer real estate within the Home Loans

portfolio segment and credit card loans within the Credit Card and

Other Consumer portfolio segment, is based on aggregated

portfolio segment evaluations generally by product type. Loss

forecast models are utilized for these portfolios which consider a

variety of factors including, but not limited to, historical loss

experience, estimated defaults or foreclosures based on portfolio

trends, delinquencies, bankruptcies, economic conditions and

credit scores.

The Corporation’s Home Loans portfolio segment is comprised

primarily of large groups of homogeneous consumer loans secured

by residential real estate. The amount of losses incurred in the

homogeneous loan pools is estimated based on the number of

loans that will default and the loss in the event of default. Using