Bank of America 2013 Annual Report Download - page 110

Download and view the complete annual report

Please find page 110 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

108 Bank of America 2013

The histogram below is a graphic depiction of trading volatility

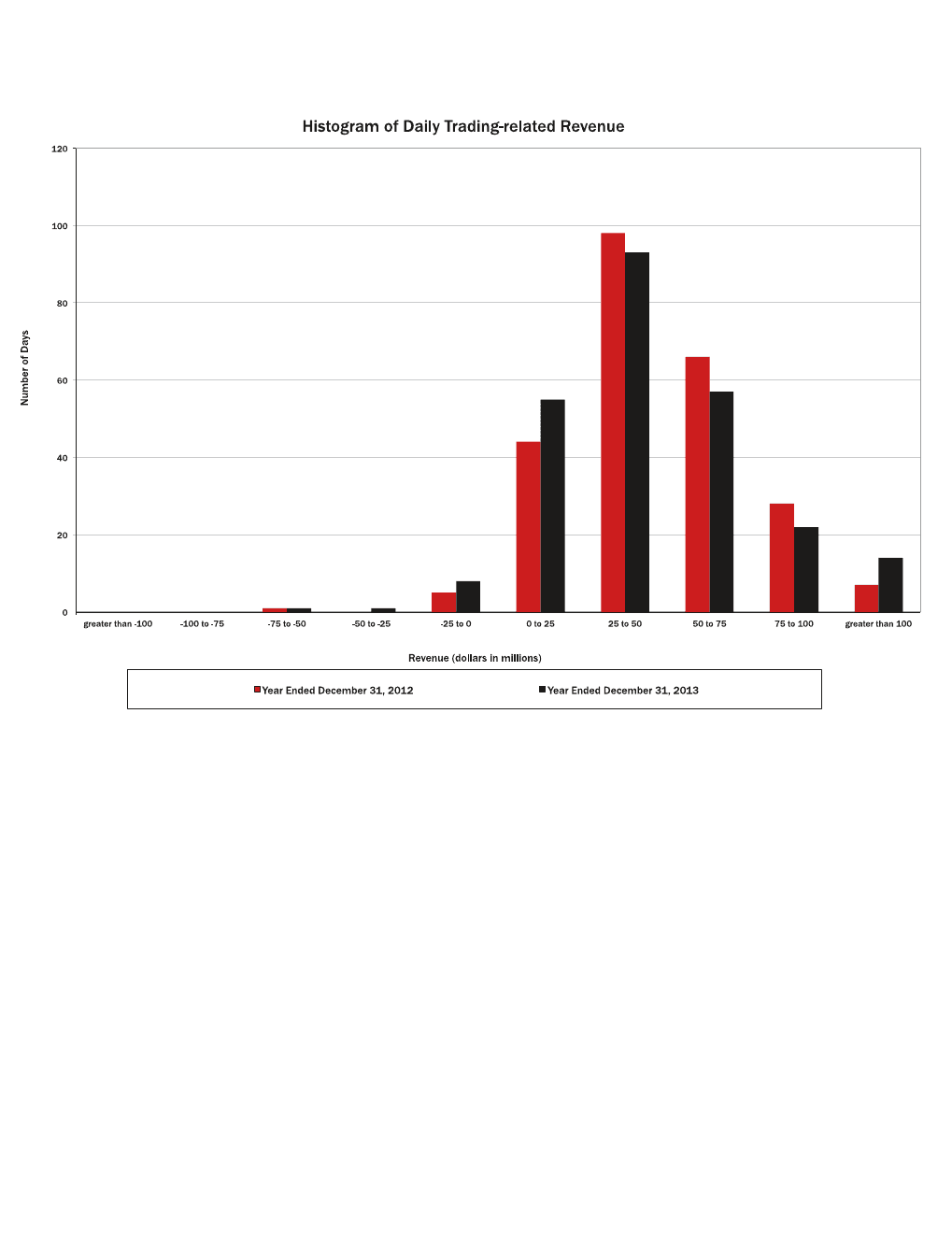

and illustrates the daily level of trading-related revenue for 2013

and 2012. During 2013, positive trading-related revenue was

recorded for 96 percent, or 241 of the 251 trading days, of which

74 percent (186 days) were daily trading gains of over $25 million

and the largest loss was $54 million. This compares to 2012

where positive trading-related revenue was recorded for 98

percent, or 243 of the 249 trading days, of which 80 percent (199

days) were daily trading gains of over $25 million and the largest

loss was $50 million.

Trading Portfolio Stress Testing

Because the very nature of a VaR model suggests results can

exceed our estimates and are dependent on a limited historical

window, we also stress test our portfolio using scenario analysis.

This analysis estimates the change in value of our trading portfolio

that may result from abnormal market movements.

A set of scenarios, categorized as either historical or

hypothetical, are computed daily for the overall trading portfolio

and individual businesses. These scenarios include shocks to

underlying market risk factors that may be well beyond the shocks

found in the historical data used to calculate VaR. Historical

scenarios simulate the impact of the market moves that occurred

during a period of extended historical market stress. Generally, a

10-business day window or longer representing the most severe

point during a crisis is selected for each historical scenario.

Hypothetical scenarios provide simulations of the estimated

portfolio impact from potential future market stress events.

Scenarios are reviewed and updated in response to changing

positions and new economic or political information. In addition,

new or adhoc scenarios are developed to address specific

potential market events. For example, a stress test was conducted

to estimate the impact of a significant increase in global interest

rates and the corresponding impact across other asset classes.

The stress tests are reviewed on a regular basis and the results

are presented to senior management.

Stress testing for the trading portfolio is integrated with

enterprise-wide stress testing and incorporated into the limits

framework. A process is in place to promote consistency between

the scenarios used for the trading portfolio and those used for

enterprise-wide stress testing. The scenarios used for enterprise-

wide stress testing purposes differ from the typical trading portfolio

scenarios in that they have a longer time horizon and the results

are forecasted over multiple periods for use in consolidated capital

and liquidity planning. For additional information, see Managing

Risk – Enterprise-wide Stress Testing on page 59.