Bank of America 2013 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2013 83

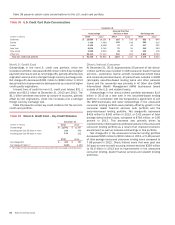

At December 31, 2013, the unpaid principal balance of pay

option loans was $4.5 billion, with a carrying value of $4.4 billion,

including $4.0 billion of loans that were credit-impaired upon

acquisition and, accordingly, the reserve is based on a life-of-loan

loss estimate. The total unpaid principal balance of pay option

loans with accumulated negative amortization was $2.2 billion

including $137 million of negative amortization. For those

borrowers who are making payments in accordance with their

contractual terms, five percent and 10 percent at December 31,

2013 and 2012 elected to make only the minimum payment on

pay option ARMs. We believe the majority of borrowers are now

making scheduled payments primarily because the low rate

environment has caused the fully indexed rates to be affordable

to more borrowers. We continue to evaluate our exposure to

payment resets on the acquired negative-amortizing loans

including the PCI pay option loan portfolio and have taken into

consideration in the evaluation several assumptions including

prepayment and default rates. Of the loans in the pay option

portfolio at December 31, 2013 that have not already experienced

a payment reset, less than one percent are expected to reset

before 2016, 26 percent are expected to reset in 2016 and

approximately 10 percent are expected to reset thereafter. In

addition, 10 percent are expected to prepay and approximately 53

percent are expected to default prior to being reset, most of which

were severely delinquent as of December 31, 2013.

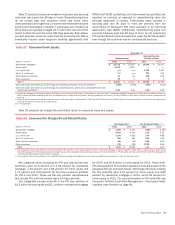

Purchased Credit-impaired Home Equity Loan Portfolio

The PCI home equity portfolio represented 26 percent of the total

PCI loan portfolio at December 31, 2013. Those loans with a

refreshed FICO score below 620 represented 16 percent of the

PCI home equity portfolio at December 31, 2013. Loans with a

refreshed CLTV greater than 90 percent, after consideration of

purchase accounting adjustments and the related valuation

allowance, represented 69 percent of the PCI home equity portfolio

and 71 percent based on the unpaid principal balance at

December 31, 2013. Table 36 presents outstandings net of

purchase accounting adjustments and before the related valuation

allowance, by certain state concentrations.

Table 36 Outstanding Purchased Credit-impaired Loan

Portfolio – Home Equity State Concentrations

December 31

(Dollars in millions) 2013 2012

California $ 1,921 $ 2,629

Florida (1) 356 524

Virginia 310 383

Arizona 214 297

Colorado 199 264

Other U.S./Non-U.S. 3,593 4,570

Total $ 6,593 $ 8,667

(1) In this state, foreclosure requires a court order following a legal proceeding (judicial state).

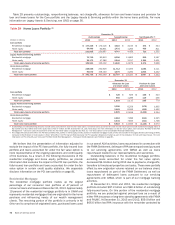

U.S. Credit Card

At December 31, 2013, 96 percent of the U.S. credit card portfolio

was managed in CBB with the remainder managed in GWIM.

Outstandings in the U.S. credit card portfolio decreased $2.5

billion in 2013 primarily due to higher payment volumes as well

as net charge-offs and the transfer of loans to LHFS, partially offset

by new originations. Net charge-offs decreased $1.3 billion to $3.4

billion in 2013 due to improvements in delinquencies and

bankruptcies as a result of an improved economic environment,

account management on higher risk accounts and the impact of

higher credit quality originations. U.S. credit card loans 30 days

or more past due and still accruing interest decreased $675 million

while loans 90 days or more past due and still accruing interest

declined $384 million in 2013 as a result of the factors mentioned

above that contributed to lower net charge-offs.

Table 37 presents certain key credit statistics for the U.S. credit

card portfolio.

Table 37 U.S. Credit Card – Key Credit Statistics

December 31

(Dollars in millions) 2013 2012

Outstandings $ 92,338 $ 94,835

Accruing past due 30 days or more 2,073 2,748

Accruing past due 90 days or more 1,053 1,437

2013 2012

Net charge-offs $ 3,376 $ 4,632

Net charge-off ratios (1) 3.74% 4.88%

(1) Net charge-off ratios are calculated as net charge-offs divided by average outstanding loans.

Unused lines of credit for U.S. credit card totaled $315.1 billion

and $335.5 billion at December 31, 2013 and 2012. The $20.4

billion decrease was driven by closure of inactive accounts,

partially offset by new originations and credit line increases.