Bank of America 2013 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

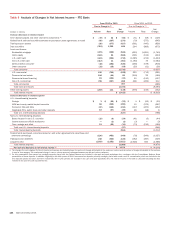

114 Bank of America 2013

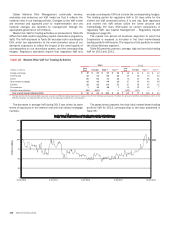

assumption affects the allowance for credit losses depends on

the severity of the change and its relationship to the other

assumptions.

Key judgments used in determining the allowance for credit

losses include risk ratings for pools of commercial loans and

leases, market and collateral values and discount rates for

individually evaluated loans, product type classifications for

consumer and commercial loans and leases, loss rates used for

consumer and commercial loans and leases, adjustments made

to address current events and conditions, considerations

regarding domestic and global economic uncertainty, and overall

credit conditions.

Our estimate for the allowance for loan and lease losses is

sensitive to the loss rates and expected cash flows from our Home

Loans and Credit Card and Other Consumer portfolio segments,

as well as our U.S. small business commercial portfolio within the

Commercial portfolio segment. For each one percent increase in

the loss rates on loans collectively evaluated for impairment in

our Home Loans portfolio segment, excluding PCI loans, coupled

with a one percent decrease in the discounted cash flows on those

loans individually evaluated for impairment within this portfolio

segment, the allowance for loan and lease losses at December 31,

2013 would have increased by $127 million. PCI loans within our

Home Loans portfolio segment are initially recorded at fair value.

Applicable accounting guidance prohibits carry-over or creation of

valuation allowances in the initial accounting. However,

subsequent decreases in the expected cash flows from the date

of acquisition result in a charge to the provision for credit losses

and a corresponding increase to the allowance for loan and lease

losses. We subject our PCI portfolio to stress scenarios to evaluate

the potential impact given certain events. A one percent decrease

in the expected cash flows could result in a $205 million

impairment of the portfolio. For each one percent increase in the

loss rates on loans collectively evaluated for impairment within

our Credit Card and Other Consumer portfolio segment and U.S.

small business commercial portfolio coupled with a one percent

decrease in the expected cash flows on those loans individually

evaluated for impairment within the portfolio segment and the U.S.

small business commercial portfolio, the allowance for loan and

lease losses at December 31, 2013 would have increased by $59

million.

Our allowance for loan and lease losses is sensitive to the risk

ratings assigned to loans and leases within the Commercial

portfolio segment (excluding the U.S. small business commercial

portfolio). Assuming a downgrade of one level in the internal risk

ratings for commercial loans and leases, except loans and leases

already risk-rated Doubtful as defined by regulatory authorities,

the allowance for loan and lease losses would have increased by

$2.2 billion at December 31, 2013.

The allowance for loan and lease losses as a percentage of

total loans and leases at December 31, 2013 was 1.90 percent

and these hypothetical increases in the allowance would raise the

ratio to 2.18 percent.

These sensitivity analyses do not represent management’s

expectations of the deterioration in risk ratings or the increases

in loss rates but are provided as hypothetical scenarios to assess

the sensitivity of the allowance for loan and lease losses to

changes in key inputs. We believe the risk ratings and loss

severities currently in use are appropriate and that the probability

of the alternative scenarios outlined above occurring within a short

period of time is remote.

The process of determining the level of the allowance for credit

losses requires a high degree of judgment. It is possible that

others, given the same information, may at any point in time reach

different reasonable conclusions.

For a discussion of the Financial Accounting Standards Board’s

proposed standard on accounting for credit losses, see Note 1 –

Summary of Significant Accounting Principles to the Consolidated

Financial Statements.

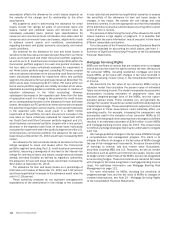

Mortgage Servicing Rights

MSRs are nonfinancial assets that are created when a mortgage

loan is sold and we retain the right to service the loan. We account

for consumer MSRs, including residential mortgage and home

equity MSRs, at fair value with changes in fair value recorded in

mortgage banking income (loss) in the Consolidated Statement

of Income.

We determine the fair value of our consumer MSRs using a

valuation model that calculates the present value of estimated

future net servicing income. The model incorporates key economic

assumptions including estimates of prepayment rates and

resultant weighted-average lives of the MSRs, and the option-

adjusted spread levels. These variables can, and generally do,

change from quarter to quarter as market conditions and projected

interest rates change. These assumptions are subjective in nature

and changes in these assumptions could materially affect our

operating results. For example, increasing the prepayment rate

assumption used in the valuation of our consumer MSRs by 10

percent while keeping all other assumptions unchanged could have

resulted in an estimated decrease of $244 million in both MSRs

and mortgage banking income (loss) for 2013. This impact does

not reflect any hedge strategies that may be undertaken to mitigate

such risk.

We manage potential changes in the fair value of MSRs through

a comprehensive risk management program. The intent is to

mitigate the effects of changes in the fair value of MSRs through

the use of risk management instruments. To reduce the sensitivity

of earnings to interest rate and market value fluctuations,

securities including MBS and U.S. Treasuries, as well as certain

derivatives such as options and interest rate swaps, may be used

to hedge certain market risks of the MSRs, but are not designated

as accounting hedges. These instruments are carried at fair value

with changes in fair value recognized in mortgage banking income

(loss). For additional information, see Mortgage Banking Risk

Management on page 112.

For more information on MSRs, including the sensitivity of

weighted-average lives and the fair value of MSRs to changes in

modeled assumptions, see Note 23 – Mortgage Servicing Rights

to the Consolidated Financial Statements.