Bank of America 2013 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2013 39

Core production revenue decreased $1.2 billion due to

industry-wide margin compression combined with lower loan

application volumes as described below.

The representations and warranties provision decreased $3.1

billion in 2013 to $840 million as 2012 included $2.5 billion in

provision related to the FNMA Settlement and $500 million for

obligations to FNMA related to MI rescissions. Net servicing

income decreased $2.9 billion to $2.9 billion driven by lower

servicing fees due to a smaller servicing portfolio, less favorable

MSR net-of-hedge performance and lower ancillary income due to

the divestiture of an ancillary business in 2012. The decline in

the size of our servicing portfolio was driven by strategic sales of

MSRs as well as loan prepayment activity, which exceeded new

originations primarily due to our exit from non-retail channels. For

more information on sales of MSRs, see Sales of Mortgage

Servicing Rights on page 39.

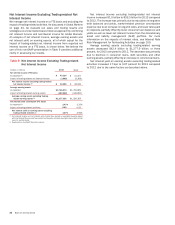

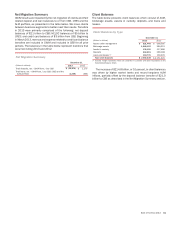

Key Statistics

(Dollars in millions, except as noted) 2013 2012

Loan production

Total Corporation (1):

First mortgage $ 83,421 $ 75,074

Home equity 6,355 3,585

CRES:

First mortgage $ 66,914 $ 55,518

Home equity 5,498 2,832

Year end

Mortgage serviced portfolio (in billions) (2, 3) $ 810 $ 1,332

Mortgage loans serviced for investors

(in billions) 550 1,045

Mortgage servicing rights:

Balance 5,042 5,716

Capitalized mortgage servicing rights

(% of loans serviced for investors) 92 bps 55 bps

(1) In addition to loan production in CRES, the remaining first mortgage and home equity loan

production is primarily in GWIM.

(2) Servicing of residential mortgage loans, HELOCs and home equity loans.

(3) Excludes loans for which servicing transferred to third parties as of December 31, 2013, with

an effective MSR sale date of January 2, 2014, totaling $220 million.

Despite a decline in the overall mortgage market because of

higher interest rates during the second half of 2013, first mortgage

loan originations in CRES increased $11.4 billion, or 21 percent,

to $66.9 billion in 2013, and for the total Corporation, increased

$8.3 billion to $83.4 billion as we increased market share due to

higher fulfillment capacity. The increase in interest rates also had

an adverse impact on our mortgage loan applications, particularly

for refinance mortgage loans. Our volume of mortgage applications

decreased 15 percent in 2013 corresponding to a decline in the

estimated overall U.S. demand for mortgages.

During 2013, 82 percent of our first mortgage production

volume was for refinance originations and 18 percent was for

purchase originations compared to 84 percent and 16 percent in

2012. HARP refinance originations were 23 percent of all refinance

originations compared to 31 percent in 2012. Making Home

Affordable non-HARP refinance originations were 19 percent of all

refinance originations as compared to 12 percent in 2012. The

remaining 58 percent of refinance originations was conventional

refinances, and remained relatively unchanged from 2012.

Home equity production was $6.4 billion for 2013 compared

to $3.6 billion for 2012 with the increase due to a higher demand

in the market based on improving housing trends, and increased

market share driven by improved banking center engagement with

customers and more competitive pricing.

Mortgage Servicing Rights

At December 31, 2013, the consumer MSR balance was $5.0

billion, which represented 92 bps of the related unpaid principal

balance compared to $5.7 billion, or 55 bps of the related unpaid

principal balance at December 31, 2012. The consumer MSR

balance decreased $674 million during 2013 primarily driven by

MSR sales and the recognition of modeled cash flows. These

declines were partially offset by the increase in value driven by

higher mortgage rates, which resulted in lower forecasted

prepayment speeds and was the primary driver for the increase in

the MSRs as a percentage of unpaid principal balance. For more

information on our servicing activities, see Off-Balance Sheet

Arrangements and Contractual Obligations – Servicing,

Foreclosure and Other Mortgage Matters on page 53. For more

information on MSRs, see Note 23 – Mortgage Servicing Rights to

the Consolidated Financial Statements.

Sales of Mortgage Servicing Rights

As previously disclosed, during 2013, we entered into definitive

agreements with certain counterparties to sell the servicing rights

on certain residential mortgage loans serviced for others, with an

aggregate unpaid principal balance of approximately $301 billion.

The sales involved approximately two million loans serviced by us

as of the applicable contract dates, including approximately

180,000 residential mortgage loans and 11,700 home equity

loans that were 60 days or more past due based upon current

estimates.

The transfers of servicing rights were substantially completed

in the first nine months of 2013. These sales led to a reduction

in servicing revenue in the fourth quarter of 2013 of approximately

$150 million compared to the fourth quarter of 2012.