Bank of America 2013 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2013 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

84 Bank of America 2013

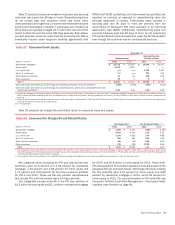

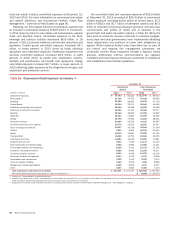

Table 38 presents certain state concentrations for the U.S. credit card portfolio.

Table 38 U.S. Credit Card State Concentrations

December 31

Outstandings

Accruing Past Due

90 Days or More Net Charge-offs

(Dollars in millions) 2013 2012 2013 2012 2013 2012

California $ 13,689 $ 14,101 $162 $ 235 $562 $ 840

Florida 7,339 7,469 105 149 359 512

Texas 6,405 6,448 72 92 217 290

New York 5,624 5,746 70 91 219 263

New Jersey 3,868 3,959 48 60 150 178

Other U.S. 55,413 57,112 596 810 1,869 2,549

Total U.S. credit card portfolio $ 92,338 $ 94,835 $ 1,053 $ 1,437 $ 3,376 $ 4,632

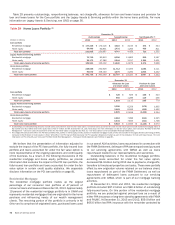

Non-U.S. Credit Card

Outstandings in the non-U.S. credit card portfolio, which are

recorded in All Other, decreased $156 million in 2013 due to higher

payment volumes as well as net charge-offs, partially offset by new

origination volume and a stronger foreign currency exchange rate.

Net charge-offs decreased $182 million to $399 million in 2013

due primarily to improvement in delinquencies as a result of higher

credit quality originations.

Unused lines of credit for non-U.S. credit card totaled $31.1

billion and $32.2 billion at December 31, 2013 and 2012. The

$1.1 billion decrease was driven by closure of accounts, partially

offset by new originations, credit line increases and a stronger

foreign currency exchange rate.

Table 39 presents certain key credit statistics for the non-U.S.

credit card portfolio.

Table 39 Non-U.S. Credit Card – Key Credit Statistics

December 31

(Dollars in millions) 2013 2012

Outstandings $ 11,541 $ 11,697

Accruing past due 30 days or more 248 403

Accruing past due 90 days or more 131 212

2013 2012

Net charge-offs $ 399 $ 581

Net charge-off ratios (1) 3.68% 4.29%

(1) Net charge-off ratios are calculated as net charge-offs divided by average outstanding loans.

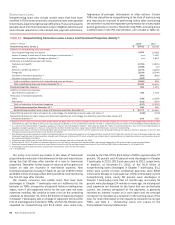

Direct/Indirect Consumer

At December 31, 2013, approximately 50 percent of the direct/

indirect portfolio was included in CBB (consumer dealer financial

services – automotive, marine, aircraft, recreational vehicle loans

and consumer personal loans), 43 percent was included in GWIM

(principally securities-based lending loans and other personal

loans) and the remainder was primarily in All Other (the GWIM

International Wealth Management (IWM) businesses based

outside of the U.S. and student loans).

Outstandings in the direct/indirect portfolio decreased $1.0

billion in 2013 as a loan sale in the securities-based lending

portfolio in connection with the Corporation’s agreement to sell

the IWM businesses and lower outstandings in the unsecured

consumer lending portfolio were partially offset by growth in the

consumer dealer financial services auto portfolio and the

securities-based lending portfolio. Net charge-offs decreased

$418 million to $345 million in 2013, or 0.42 percent of total

average direct/indirect loans, compared to $763 million, or 0.90

percent in 2012. This decrease was primarily driven by

improvements in delinquencies and bankruptcies in the unsecured

consumer lending portfolio as a result of an improved economic

environment as well as reduced outstandings in this portfolio.

Net charge-offs in the unsecured consumer lending portfolio

decreased $295 million to $190 million in 2013, or 5.26 percent

of total average unsecured consumer lending loans compared to

7.68 percent in 2012. Direct/indirect loans that were past due

30 days or more and still accruing interest declined $339 million

to $1.0 billion in 2013 due to improvements in the unsecured

consumer lending, dealer financial services and student lending

portfolios.