Bank of America 2012 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2012 101

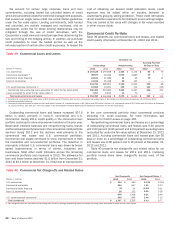

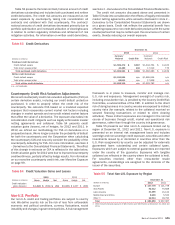

Table 53 presents the total contract/notional amount of credit

derivatives outstanding and includes both purchased and written

credit derivatives. The credit risk amounts are measured as net

asset exposure by counterparty, taking into consideration all

contracts and collateral with that counterparty. The contract/

notional amounts of credit derivatives decreased primarily due to

portfolio optimization and increased utilization of clearinghouses

in relation to certain regulatory initiatives and refinement of risk

mitigation activities. For information on written credit derivatives,

see Note 3 – Derivatives to the Consolidated Financial Statements.

The credit risk amounts discussed above and presented in

Table 53 take into consideration the effects of legally enforceable

master netting agreements, while amounts disclosed in Note 3 –

Derivatives to the Consolidated Financial Statements are shown

on a gross basis. Credit risk reflects the potential benefit from

offsetting exposure to non-credit derivative products with the same

counterparties that may be netted upon the occurrence of certain

events, thereby reducing our overall exposure.

Table 53 Credit Derivatives

December 31

2012 2011

(Dollars in millions)

Contract/

Notional Credit Risk

Contract/

Notional Credit Risk

Purchased credit derivatives:

Credit default swaps $ 1,559,472 $ 8,987 $ 1,944,764 $ 14,163

Total return swaps/other 43,489 402 17,519 776

Total purchased credit derivatives $ 1,602,961 $ 9,389 $ 1,962,283 $ 14,939

Written credit derivatives:

Credit default swaps $ 1,531,504 n/a $ 1,885,944 n/a

Total return swaps/other 68,811 n/a 17,838 n/a

Total written credit derivatives $ 1,600,315 n/a $ 1,903,782 n/a

n/a = not applicable

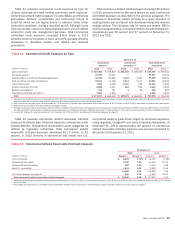

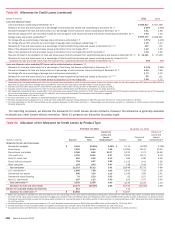

Counterparty Credit Risk Valuation Adjustments

We record counterparty credit risk valuation adjustments (CVA) on

certain derivative assets, including our credit default protection

purchased, in order to properly reflect the credit risk of the

counterparty. We calculate CVA based on a modeled expected

exposure that incorporates current market risk factors including

changes in market spreads and non-credit related market factors

that affect the value of a derivative. The exposure also takes into

consideration credit mitigants such as legally enforceable master

netting agreements and collateral. Table 54 presents credit

valuation gains (losses), net of hedges, for 2012 and 2011. In

2012, we refined our methodology for CVA on derivatives on a

prospective basis. We no longer consider the probability of default

for both the counterparty and the Corporation when calculating

the counterparty CVA and now only consider the probability of the

counterparty defaulting for CVA. For more information, see Note 3

– Derivatives to the Consolidated Financial Statements. The effect

of this change in estimate on CVA is reflected in the table below.

Credit valuation gains for 2012 were due to improved counterparty

creditworthiness, partially offset by hedge results. For information

on our monoline counterparty credit risk, see Monoline Exposure

on page 99.

Table 54 Credit Valuation Gains and Losses

2012 2011

(Dollars in millions) Gross Hedge Net Gross Hedge Net

Credit valuation

gains (losses) $ 1,022 $ (731) $ 291 $(1,863) $ 1,257 $ (606)

Non-U.S. Portfolio

Our non-U.S. credit and trading portfolios are subject to country

risk. We define country risk as the risk of loss from unfavorable

economic and political conditions, currency fluctuations, social

instability and changes in government policies. A risk management

framework is in place to measure, monitor and manage non-

U.S. risk and exposures. Management oversight of country risk,

including cross-border risk, is provided by the Country Credit Risk

Committee, a subcommittee of the CRC. In addition to the direct

risk of doing business in a country, we also are exposed to indirect

country risks (for example, related to the collateral received on

secured financing transactions or related to client clearing

activities). These indirect exposures are managed in the normal

course of business through credit, market and operational risk

governance, rather than through the country risk governance.

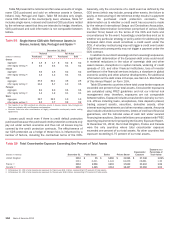

Table 55 presents our total non-U.S. exposure broken out by

region at December 31, 2012 and 2011. Non-U.S. exposure is

presented on an internal risk management basis and includes

sovereign and non-sovereign credit exposure, securities and other

investments issued by or domiciled in countries other than the

U.S. Risk assignments by country can be adjusted for externally

guaranteed loans outstanding and certain collateral types.

Exposures which are subject to external guarantees are reported

under the country of the guarantor. Exposures with tangible

collateral are reflected in the country where the collateral is held.

For securities received, other than cross-border resale

agreements, outstandings are assigned to the domicile of the

issuer of the securities.

Table 55 Total Non-U.S. Exposure by Region

December 31

(Dollars in millions) 2012 2011

Europe $ 137,778 $ 121,778

Asia Pacific 92,412 75,828

Latin America 21,246 15,133

Middle East and Africa 8,200 5,533

Other (1) 22,014 18,795

Total $ 281,650 $ 237,067

(1) Other includes Canada exposure of $20.3 billion and $16.9 billion at December 31, 2012 and

2011.