Bank of America 2012 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2012 37

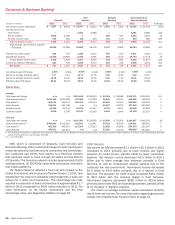

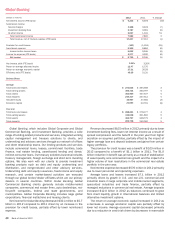

Consumer Real Estate Services

Home Loans

Legacy Assets &

Servicing

Total Consumer Real

Estate Services

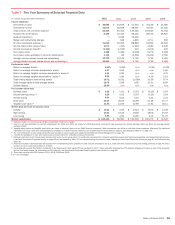

(Dollars in millions) 2012 2011 2012 2011 2012 2011 % Change

Net interest income (FTE basis) $ 1,361 $ 1,828 $ 1,598 $ 1,379 $ 2,959 $ 3,207 (8)%

Noninterest income:

Mortgage banking income (loss) 3,284 2,312 2,247 (10,505) 5,531 (8,193) (168)

Insurance income 6750 ——6750 (99)

All other income (loss) (5) 971 268 111 263 1,082 (76)

Total noninterest income (loss) 3,285 4,033 2,515 (10,394) 5,800 (6,361) (191)

Total revenue, net of interest expense (FTE basis) 4,646 5,861 4,113 (9,015) 8,759 (3,154) n/m

Provision for credit losses 72 233 1,370 4,291 1,442 4,524 (68)

Goodwill impairment ———2,603 —2,603 (100)

All other noninterest expense 3,171 4,563 14,135 14,625 17,306 19,188 (10)

Income (loss) before income taxes 1,403 1,065 (11,392) (30,534) (9,989)(29,469) (66)

Income tax expense (benefit) (FTE basis) 511 396 (3,993)(10,400) (3,482)(10,004) (65)

Net income (loss) $ 892 $ 669 $(7,399)$ (20,134) $(6,507)$ (19,465) (67)

Net interest yield (FTE basis) 2.41% 2.59% 2.45%1.63% 2.43%2.07%

Efficiency ratio (FTE basis) 68.25 77.85 n/m n/m n/m n/m

Balance Sheet

Average

Total loans and leases $ 50,023 $ 54,663 $ 54,731 $ 65,157 $ 104,754 $119,820 (13)

Total earning assets 56,581 70,488 65,288 84,402 121,869 154,890 (21)

Total assets 57,550 71,508 89,055 118,859 146,605 190,367 (23)

Allocated equity n/a n/a n/a n/a 13,687 16,202 (16)

Economic capital n/a n/a n/a n/a 13,687 14,852 (8)

Year end

Total loans and leases $ 47,742 $ 52,371 $ 48,230 $ 59,988 $95,972 $112,359 (15)

Total earning assets 54,394 58,819 53,892 73,562 108,286 132,381 (18)

Total assets 55,463 59,647 76,925 104,065 132,388 163,712 (19)

n/m = not meaningful

n/a = not applicable

CRES operations include Home Loans and Legacy Assets &

Servicing. Home Loans is responsible for ongoing loan production

activities and the CRES home equity loan portfolio not selected

for inclusion in the Legacy Assets & Servicing owned portfolio.

Legacy Assets & Servicing is responsible for all of our mortgage

servicing activities related to loans serviced for others and loans

held by the Corporation, including loans that have been designated

as the Legacy Assets & Servicing Portfolios. The Legacy Assets

& Servicing Portfolios (both owned and serviced), herein referred

to as the Legacy Owned and Legacy Serviced Portfolios,

respectively, (together, the Legacy Portfolios), and as further

defined below, include those loans that would not have been

originated under our underwriting standards as of December 31,

2010. For additional information on our Legacy Portfolios, see

page 39. In addition, Legacy Assets & Servicing is responsible for

managing legacy exposures related to CRES (e.g., representations

and warranties). This alignment allows CRES management to lead

the ongoing Home Loans business while also providing greater

focus on legacy mortgage issues and servicing activities.

CRES, primarily through Home Loans operations, generates

revenue by providing an extensive line of consumer real estate

products and services to customers nationwide. CRES products

offered by Home Loans include fixed- and adjustable-rate first-lien

mortgage loans for home purchase and refinancing needs, home

equity lines of credit (HELOCs) and home equity loans. First

mortgage products are either sold into the secondary mortgage

market to investors, while we generally retain MSRs and the Bank

of America customer relationships, or are held on the balance

sheet in All Other for ALM purposes. Home Loans is compensated

for loans held for ALM purposes on a management accounting

basis with the corresponding offset in All Other. Newly originated

HELOCs and home equity loans are retained on the CRES balance

sheet in Home Loans.

CRES includes the impact of transferring customers and their

related loan balances between GWIM and CRES. For more

information on the migration of customer balances, see GWIM on

page 46.

CRES Results

The net loss for CRES decreased $13.0 billion to $6.5 billion for

2012 compared to 2011 primarily driven by mortgage banking

income of $5.5 billion in 2012 compared to a loss of $8.2 billion

in 2011. Also contributing to the decrease in the net loss was

lower provision for credit losses and a decline in noninterest

expense, partially offset by lower insurance income and other

income. Mortgage banking income increased $13.7 billion due to

an $11.7 billion decrease in representations and warranties

provision, and higher servicing income and core production

revenue. The provision for credit losses decreased $3.1 billion

driven by improved portfolio trends and increasing home prices in