Bank of America 2012 Annual Report Download - page 125

Download and view the complete annual report

Please find page 125 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2012 123

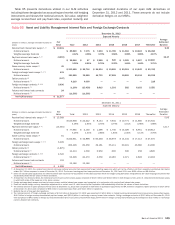

Litigation Reserve

In accordance with applicable accounting guidance, the

Corporation establishes an accrued liability for litigation and

regulatory matters when those matters present loss contingencies

that are both probable and estimable. In such cases, there may

be an exposure to loss in excess of any amounts accrued. When

a loss contingency is not both probable and estimable, the

Corporation does not establish an accrued liability. As a litigation

or regulatory matter develops, the Corporation, in conjunction with

any outside counsel handling the matter, evaluates on an ongoing

basis whether such matter presents a loss contingency that is

both probable and estimable. If, at the time of evaluation, the loss

contingency related to a litigation or regulatory matter is not both

probable and estimable, the matter will continue to be monitored

for further developments that would make such loss contingency

both probable and estimable. Once the loss contingency related

to a litigation or regulatory matter is deemed to be both probable

and estimable, the Corporation will establish an accrued liability

with respect to such loss contingency and record a corresponding

amount of litigation-related expense. The Corporation will continue

to monitor the matter for further developments that could affect

the amount of the accrued liability that has been previously

established.

For a limited number of the matters disclosed in Note 13 –

Commitments and Contingencies to the Consolidated Financial

Statements for which a loss is probable or reasonably possible in

future periods, whether in excess of a related accrued liability or

where there is no accrued liability, we are able to estimate a range

of possible loss. In determining whether it is possible to provide

an estimate of loss or range of possible loss, the Corporation

reviews and evaluates its material litigation and regulatory matters

on an ongoing basis, in conjunction with any outside counsel

handling the matter, in light of potentially relevant factual and legal

developments. These may include information learned through the

discovery process, rulings on dispositive motions, settlement

discussions, and other rulings by courts, arbitrators or others. In

cases in which the Corporation possesses sufficient information

to develop an estimate of loss or range of possible loss, that

estimate is aggregated and disclosed in Note 13 – Commitments

and Contingencies to the Consolidated Financial Statements. For

other disclosed matters for which a loss is probable or reasonably

possible, such an estimate is not possible. Those matters for

which an estimate is not possible are not included within this

estimated range. Therefore, the estimated range of possible loss

represents what we believe to be an estimate of possible loss only

for certain matters meeting these criteria. It does not represent

the Corporation’s maximum loss exposure. Information is provided

in Note 13 – Commitments and Contingencies to the Consolidated

Financial Statements regarding the nature of all of these

contingencies and, where specified, the amount of the claim

associated with these loss contingencies.

Consolidation and Accounting for Variable Interest

Entities

In accordance with applicable accounting guidance, an entity that

has a controlling financial interest in a VIE is referred to as the

primary beneficiary and consolidates the VIE. The Corporation is

deemed to have a controlling financial interest and is the primary

beneficiary of a VIE if it has both the power to direct the activities

of the VIE that most significantly impact the VIE’s economic

performance and an obligation to absorb losses or the right to

receive benefits that could potentially be significant to the VIE.

Determining whether an entity has a controlling financial

interest in a VIE requires significant judgment. An entity must

assess the purpose and design of the VIE, including explicit and

implicit contractual arrangements, and the entity’s involvement in

both the design of the VIE and its ongoing activities. The entity

must then determine which activities have the most significant

impact on the economic performance of the VIE and whether the

entity has the power to direct such activities. For VIEs that hold

financial assets, the party that services the assets or makes

investment management decisions may have the power to direct

the most significant activities of a VIE. Alternatively, a third party

that has the unilateral right to replace the servicer or investment

manager or to liquidate the VIE may be deemed to be the party

with power. If there are no significant ongoing activities, the party

that was responsible for the design of the VIE may be deemed to

have power. If the entity determines that it has the power to direct

the most significant activities of the VIE, then the entity must

determine if it has either an obligation to absorb losses or the

right to receive benefits that could potentially be significant to the

VIE. Such economic interests may include investments in debt or

equity instruments issued by the VIE, liquidity commitments, and

explicit and implicit guarantees.

On a quarterly basis, we reassess whether we have a controlling

financial interest and are the primary beneficiary of a VIE. The

quarterly reassessment process considers whether we have

acquired or divested the power to direct the activities of the VIE

through changes in governing documents or other circumstances.

The reassessment also considers whether we have acquired or

disposed of a financial interest that could be significant to the VIE,

or whether an interest in the VIE has become significant or is no

longer significant. The consolidation status of the VIEs with which

we are involved may change as a result of such reassessments.

Changes in consolidation status are applied prospectively, with

assets and liabilities of a newly consolidated VIE initially recorded

at fair value. A gain or loss may be recognized upon deconsolidation

of a VIE depending on the carrying amounts of deconsolidated

assets and liabilities compared to the fair value of retained

interests and ongoing contractual arrangements.