Bank of America 2012 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

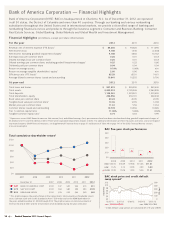

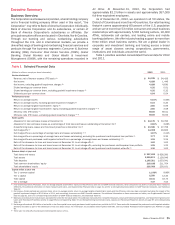

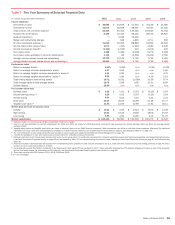

Bank of America 2012 19

Management’s Discussion and Analysis of Financial Condition and Results of Operations

This report, the documents that it incorporates by reference and

the documents into which it may be incorporated by reference may

contain, and from time to time Bank of America Corporation

(collectively with its subsidiaries, the Corporation) and its

management may make certain statements that constitute forward-

looking statements within the meaning of the Private Securities

Litigation Reform Act of 1995. These statements can be identified

by the fact that they do not relate strictly to historical or current

facts. Forward-looking statements often use words such as

“expects,” “anticipates,” “believes,” “estimates,” “targets,” “intends,”

“plans,” “goal” and other similar expressions or future or conditional

verbs such as “will,” “may,” “might,” “should,” “would” and “could.” The

forward-looking statements made represent the current

expectations, plans or forecasts of the Corporation regarding the

Corporation’s future results and revenues, and future business and

economic conditions more generally, including statements

concerning: expectations regarding actions to be taken by the

Federal Reserve; transfers of servicing rights scheduled to occur in

stages over the course of 2013 with the delinquent loans scheduled

to be transferred after the current loans; that the criteria for

inclusion in the Legacy Assets & Servicing portfolios will continue

to be evaluated over time; the expectation that approximately $200

million in servicing fees recognized per quarter related to servicing

transferred will decrease throughout 2013 as the servicing is

transferred and that over time the impact on earnings will be

negligible as expenses are expected to also decrease after servicing

is transferred, especially the loans which are 60 days or more past

due; the expectation that liability management actions taken in the

fourth quarter of 2012 will result in pre-tax net interest income

benefit of approximately $350 million in 2013; effects of the FNMA

Settlement and 2013 IFR Acceleration Agreement; the achievement

of cost savings in certain noninterest expense categories as

workflows continue to be streamlined, processes simplified and

expenses aligned with the overall strategic plan and operating

principles; projected New BAC Phase 1 annualized cost savings of

more than $5 billion by the fourth quarter of 2013 with the full

impact expected to be realized in 2014; the expectation that New

BAC Phase 2 will result in an additional $3 billion of annualized cost

savings by mid-2015; that the Corporation may conduct additional

redemptions, tender offers, exercises and other transactions in the

future depending on prevailing market conditions, liquidity,

regulatory and other factors; the expectation that the Corporation

would record a charge to income tax expense of approximately $800

million if the income tax rate were reduced to 21 percent by 2014

as suggested in U.K. Treasury announcements and assuming no

change in the deferred tax asset balance; the goal to manage

interest rate sensitivity so that movements in interest rates do not

significantly adversely affect earnings and capital; that the sale of

the GWIM international wealth management business and the

Japanese brokerage joint venture are not expected to have a

significant impact on the Corporation’s balance sheet, results of

operations or capital ratios; the expectation that the Corporation

will make at least $319 million of contributions to pension plans

during 2013; the expectation that unresolved repurchase claims

related to private-label securitization trustees and third-party

securitization sponsors will continue to increase; the resolution of

representations and warranties repurchase and other claims; the

final resolution of the BNY Mellon Settlement; the estimates of

liability and range of possible loss for representations and

warranties repurchase claims; the possibility that future

representations and warranties losses may occur in excess of the

amounts recorded for those exposures; that the expiration and

mutual non-renewal of certain contractual delivery commitments

and variances with Fannie Mae will not have a material impact on

our CRES business, as the Corporation expects to rely on other

sources of liquidity to actively extend mortgage credit to customers

including continuing to deliver such products into Freddie Mac

mortgage-backed securities pools; that there will likely be additional

requests from monolines for loan files in the future leading to

repurchase claims; the belief that increases in requests for loan

files from certain private-label securitization trustees and requests

for tolling agreements to toll the applicable statutes of limitation

related to representations and warranties repurchase claims will

likely lead to an increase in repurchase claims from private-label

securitization trustees with standing to bring such claims; the

disposition and resolution of servicing matters; that implementation

of uniform servicing standards is expected to contribute to elevated

costs associated with the servicing process but is not expected to

result in material delays or dislocation in the performance of the

mortgage servicing obligations including the completion of

foreclosures; beliefs and expectations concerning the impact of the

National Mortgage Settlement; the Corporation’s belief that the

decline in default-related servicing costs will continue to accelerate

in 2013; that swap dealers will continue to become subject to

additional CFTC rules as and when such rules take effect; that the

proposed rule regarding credit risk retention would likely have an

adverse impact on the Corporation’s ability to engage in many types

of the MBS and ABS securitizations conducted in CRES, Global

Markets and other business segments, impose additional

operational and compliance costs and negatively influence the

value, liquidity and transferability of ABS or MBS, loans and other

assets; that the Dodd-Frank Wall Street Reform and Consumer

Protection Act (Financial Reform Act) will continue to have a

significant and negative impact on earnings through fee reductions,

higher costs and new restrictions as well as reductions to available

capital; the substance and timing of the final rules implementing

Basel 3; the expectation that the Corporation will comply with the

final Basel 3 rules when issued and effective; that estimates under

the Basel 3 Advanced Approach will be refined over time as a result

of further rulemaking or clarification by U.S. banking regulators and

as its understanding and interpretation of the rules evolve; that the

final rules when adopted and fully implemented are likely to

influence regulatory capital and liquidity planning processes and

may impose additional operational and compliance costs on the

Corporation; the expectation that the Liquidity Coverage Ratio

requirement will be implemented in January 2015 and the Net

Stable Funding Ratio requirement in January 2018, following an

observation period that began in 2011; the goal to seek to maintain

safety and soundness at all times, including under adverse

conditions, to take advantage of organic growth opportunities,

maintain ready access to financial markets, continue to serve as a

credit intermediary, remain a source of strength for the Corporation’s

subsidiaries, and satisfy current and future regulatory capital

requirements; the goal of mitigating refinancing risk by actively

managing the amount of borrowings that will likely mature within

any month or quarter; the objective of maintaining high-quality credit

ratings; that, if the Corporation’s analytical models for capital

measurement under Basel 3 are not approved by the U.S. regulatory