Bank of America 2012 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2012 53

Open Mortgage Insurance Rescission Notices

In addition to repurchase claims, we receive notices from mortgage

insurance companies of claim denials, cancellations or coverage

rescission (collectively, MI rescission notices) and the number of

such notices has remained elevated. By way of background,

mortgage insurance compensates lenders or investors for certain

losses resulting from borrower default on a mortgage loan. When

there is disagreement with the mortgage insurer as to the

resolution of a MI rescission notice, meaningful dialogue and

negotiation between the mortgage insurance company and the

Corporation are generally necessary to reach a resolution on an

individual notice. The level of engagement of the mortgage

insurance companies varies and ongoing litigation involving some

of the mortgage insurance companies over individual and bulk

rescissions or claims for rescission limits our ability to engage in

constructive dialogue leading to resolution.

For loans sold to GSEs or private-label securitization trusts

(including those wrapped by the monoline bond insurers), when

we receive a MI rescission notice from a mortgage insurance

company, it may give rise to a claim for breach of the applicable

representations and warranties from the GSEs or private-label

securitization trusts, depending on the governing sales contracts.

In those cases where the governing contract contains MI-related

representations and warranties, which upon rescission require us

to repurchase the affected loan or indemnify the investor for the

related loss, we realize the loss without the benefit of MI. See

below for a discussion of the impact of the FNMA Settlement. In

addition, mortgage insurance companies have in some cases

asserted the ability to curtail MI payments as a result of alleged

foreclosure delays, which if successful, would reduce the MI

proceeds available to reduce the loss on the loan.

At December 31, 2012, we had approximately 110,000 open

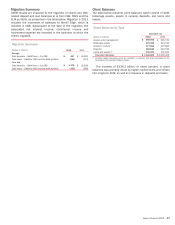

MI rescission notices compared to 90,000 at December 31, 2011,

including 49,000 pertaining principally to first-lien mortgages

serviced for others, 11,000 pertaining to loans held-for-investment

(HFI), and 50,000 pertaining to ongoing litigation for second-lien

mortgages. Approximately 27,000 of the open MI rescission

notices pertaining to first-lien mortgages serviced for others are

related to loans sold to FNMA. As of December 31, 2012, 32

percent of the MI rescission notices received have been resolved.

Of those resolved, 20 percent were resolved through our

acceptance of the MI rescission, 58 percent were resolved through

reinstatement of coverage or payment of the claim by the mortgage

insurance company, and 22 percent were resolved on an aggregate

basis through settlement, policy commutation or similar

arrangement. As of December 31, 2012, 68 percent of the MI

rescission notices we have received have not yet been resolved.

Of those not yet resolved, 46 percent are implicated by ongoing

litigation where no loan-level review is currently contemplated nor

required to preserve our legal rights. In this litigation, the litigating

mortgage insurance companies are also seeking bulk rescission

of certain policies, separate and apart from loan-by-loan denials

or rescissions. We are in the process of reviewing 37 percent of

the remaining open MI rescission notices, and we have reviewed

and are contesting the MI rescission with respect to 63 percent

of these remaining open MI rescission notices. Of the remaining

open MI rescission notices, 40 percent are also the subject of

ongoing litigation; although, at present, these MI rescissions are

being processed in a manner generally consistent with those not

affected by litigation.

In addition to the discussion above, the FNMA Settlement

resolved significant representations and warranties exposures

including unresolved and potential repurchase claims from FNMA

resulting solely from MI rescission notices relating to loans covered

by the FNMA Settlement. Our pipeline of unresolved repurchase

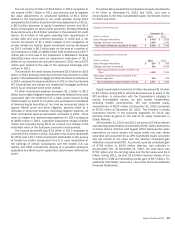

claims from the GSEs resulting solely from MI rescission notices

increased to $2.3 billion at December 31, 2012 from $1.2 billion

at December 31, 2011. The FNMA Settlement resolved

approximately $1.9 billion of such unresolved repurchase claims.

In 2011, FNMA issued an announcement requiring servicers to

report all MI rescission notices with respect to loans sold to FNMA

and confirmed FNMA’s view of its position that a mortgage

insurance company’s issuance of a MI rescission notice in and of

itself constitutes a breach of the lender’s representations and

warranties and permits FNMA to require the lender to repurchase

the mortgage loan or promptly remit a make-whole payment

covering FNMA’s loss even if the lender is contesting the MI

rescission notice. We had informed FNMA that we did not believe

that the new policy was valid under our contracts with FNMA. The

parties resolved this and other MI-related issues as part of the

FNMA Settlement, which clarified the parties’ obligations with

respect to MI including establishing timeframes for certain

payments and other actions, setting parameters for potential bulk

settlements and providing for cooperation in future dealings with

mortgage insurers. As a result, we will be required to remit to FNMA

the amount of certain MI coverage as a result of MI claims

rescissions in advance of collection from the mortgage insurance

companies and, in certain cases, we may not ultimately collect all

such amounts from the mortgage insurance companies. For

additional information, see Note 8 – Representations and

Warranties Obligations and Corporate Guarantees to the

Consolidated Financial Statements.

Representations and Warranties Liability

The liability for representations and warranties and corporate

guarantees is included in accrued expenses and other liabilities

on the Corporation’s Consolidated Balance Sheet and the related

provision is included in mortgage banking income (loss). Our

estimate of the liability for representations and warranties

exposure and the corresponding range of possible loss is based

on currently available information, significant judgment and a

number of factors and assumptions that are subject to change.

For additional information, see the Estimated Range of Possible

Loss section below and Note 8 – Representations and Warranties

Obligations and Corporate Guarantees to the Consolidated

Financial Statements and, for information related to the sensitivity

of the assumptions used to estimate our liability for obligations

under representations and warranties, see Complex Accounting

Estimates – Representations and Warranties on page 122.

The liability for obligations under representations and

warranties and the corresponding estimated range of possible loss

for these representations and warranties exposures do not

consider any losses related to litigation matters, including litigation

brought by monoline insurers, nor do they include any separate

foreclosure costs and related costs, assessments and

compensatory fees or any other possible losses related to

potential claims for breaches of performance of servicing

obligations, except as such losses are included as potential costs

of the BNY Mellon Settlement, potential securities law or fraud

claims or potential indemnity or other claims against us, including

claims related to loans insured by the FHA. We are not able to

reasonably estimate the amount of any possible loss with respect

to any such servicing, securities law, fraud or other claims against

us, except to the extent reflected in the aggregate range of possible