Bank of America 2012 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

82 Bank of America 2012

downs on loans greater than 180 days past due which were written

down to the estimated fair value of the collateral less estimated

costs to sell, and favorable delinquency trends. In addition, 2012

included $75 million in net charge-offs related to loans discharged

in Chapter 7 bankruptcy that were written down to the underlying

collateral value as a result of new regulatory guidance. For more

information on the new regulatory guidance on loans discharged

in Chapter 7 bankruptcy, see Consumer Portfolio Credit Risk

Management on page 76 and Table 21. Net charge-off ratios were

further impacted by lower loan balances primarily due to paydowns

and charge-offs outpacing new originations.

Loans in the residential mortgage portfolio with certain

characteristics have greater risk of loss than others. These

characteristics include loans with a high refreshed LTV, loans

originated at the peak of home prices in 2006 and 2007, interest-

only loans and loans to borrowers located in California and Florida

where we have concentrations and where significant declines in

home prices have been experienced. Although the disclosures in

this section address each of these risk characteristics separately,

there is significant overlap in loans with these characteristics,

which contributed to a disproportionate share of the losses in the

portfolio. The residential mortgage loans with all of these higher

risk characteristics comprised four percent and six percent of the

residential mortgage portfolio at December 31, 2012 and 2011,

and accounted for 20 percent of the residential mortgage net

charge-offs in 2012, and 23 percent in 2011.

Residential mortgage loans with a greater than 90 percent but

less than 100 percent refreshed LTV represented 10 percent and

11 percent of the residential mortgage portfolio at December 31,

2012 and 2011. Loans with a refreshed LTV greater than

100 percent represented 20 percent and 26 percent of the

residential mortgage loan portfolio at December 31, 2012 and

2011. Of the loans with a refreshed LTV greater than 100 percent,

92 percent were performing at both December 31, 2012 and 2011.

Loans with a refreshed LTV greater than 100 percent reflect loans

where the outstanding carrying value of the loan is greater than

the most recent valuation of the property securing the loan. The

majority of these loans have a refreshed LTV greater than 100

percent primarily due to home price deterioration over the past

several years. Loans to borrowers with refreshed FICO scores

below 620 represented 14 percent and 15 percent of the

residential mortgage portfolio at December 31, 2012 and 2011.

Of the $143.6 billion and $158.5 billion in total residential

mortgage loans outstanding at December 31, 2012 and 2011, as

shown in Table 26, 41 percent and 40 percent were originated as

interest-only loans. The outstanding balance of interest-only

residential mortgage loans that have entered the amortization

period was $13.7 billion, or 23 percent, at December 31, 2012.

Residential mortgage loans that have entered the amortization

period have experienced a higher rate of early stage delinquencies

and nonperforming status compared to the residential mortgage

portfolio as a whole. As of December 31, 2012, $368 million, or

three percent of outstanding interest-only residential mortgages

that had entered the amortization period were accruing past due

30 days or more compared to $3.1 billion, or two percent of

accruing past due 30 days or more for the entire residential

mortgage portfolio. In addition, at December 31, 2012, $2.1

billion, or 16 percent of outstanding interest-only residential

mortgages that had entered the amortization period were

nonperforming compared to $14.8 billion, or 10 percent of

nonperforming loans for the entire residential mortgage portfolio.

Loans in our interest-only residential mortgage portfolio have an

interest-only period of three to 10 years and more than 85 percent

of these loans will not be required to make a fully-amortizing

payment until 2015 or later.

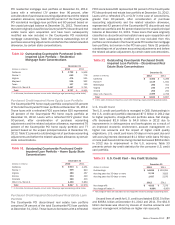

Table 26 presents outstandings, nonperforming loans and net

charge-offs by certain state concentrations for the residential

mortgage portfolio. The Los Angeles-Long Beach-Santa Ana

Metropolitan Statistical Area (MSA) within California represented

12 percent of outstandings at both December 31, 2012 and 2011.

Loans within this MSA comprised only eight percent and seven

percent of net charge-offs for 2012 and 2011.

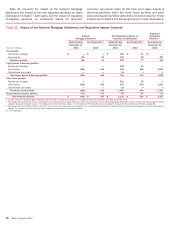

Table 26 Residential Mortgage State Concentrations

December 31

Outstandings (1) Nonperforming (1) Net Charge-offs

(Dollars in millions) 2012 2011 2012 (2) 2011 2012 (2) 2011

California $ 48,281 $ 54,203 $ 4,510 $ 5,606 $ 1,117 $ 1,326

New York (3) 11,240 11,539 956 838 79 106

Florida (3) 10,994 12,338 1,729 1,900 372 595

Texas 6,885 7,525 488 425 51 55

Virginia 5,067 5,709 404 399 50 64

Other U.S./Non-U.S. 61,123 67,156 6,721 6,802 1,384 1,686

Residential mortgage loans (4) $ 143,590 $158,470 $ 14,808 $ 15,970 $ 3,053 $ 3,832

Fully-insured loan portfolio 90,854 93,854

Countrywide purchased credit-impaired residential mortgage loan portfolio 8,737 9,966

Total residential mortgage loan portfolio $ 243,181 $262,290

(1) Outstandings and nonperforming amounts exclude loans accounted for under the fair value option. There were $147 million and $906 million of residential mortgage loans accounted for under the

fair value option at December 31, 2012 and 2011. See Consumer Portfolio Credit Risk Management – Consumer Loans Accounted for Under the Fair Value Option on page 89 and Note 22 – Fair

Value Option to the Consolidated Financial Statements for additional information on the fair value option.

(2) Nonperforming loans and net charge-offs include the impact of new regulatory guidance on loans discharged in Chapter 7 bankruptcy. For more information, see Consumer Portfolio Credit Risk

Management on page 76 and Table 21.

(3) In these states, foreclosure requires a court order following a legal proceeding (judicial states).

(4) Amount excludes the Countrywide PCI residential mortgage and fully-insured loan portfolios.

The Community Reinvestment Act (CRA) encourages banks to

meet the credit needs of their communities for housing and other

purposes, particularly in neighborhoods with low or moderate

incomes. At December 31, 2012 and 2011, our CRA portfolio was

$11.3 billion and $12.5 billion, or eight percent of the residential

mortgage loan balances for both periods. The CRA portfolio

included $2.5 billion of nonperforming loans at both December

31, 2012 and 2011 representing 17 percent and 15 percent of