Bank of America 2012 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

96 Bank of America 2012

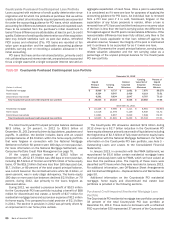

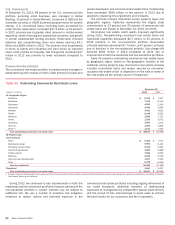

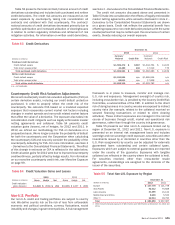

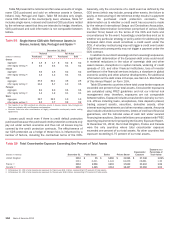

At December 31, 2012 and 2011, the commercial real estate

loan portfolio included $6.7 billion and $10.9 billion of funded

construction and land development loans that were originated to

fund the construction and/or rehabilitation of commercial

properties. The decline in construction and land development

loans was driven by repayments, net charge-offs, continued risk

mitigation initiatives and a reduced emphasis on new originations.

This portfolio is mostly secured and diversified across property

types and geographic regions but faces continuing challenges in

the housing markets. Reservable criticized construction and land

development loans totaled $1.5 billion and $4.9 billion, and

nonperforming construction and land development loans and

foreclosed properties totaled $730 million and $2.1 billion at

December 31, 2012 and 2011. During a property’s construction

phase, interest income is typically paid from interest reserves that

are established at the inception of the loan. As construction is

completed and the property is put into service, these interest

reserves are depleted and interest payments from operating cash

flows begin. Loans generally continue to be classified as

construction loans until operating cash flows reach appropriate

levels or the loans are refinanced. We do not recognize interest

income on nonperforming loans regardless of the existence of an

interest reserve.

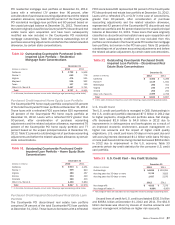

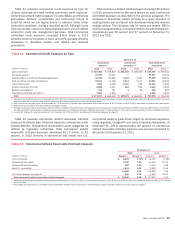

Non-U.S. Commercial

At December 31, 2012, 72 percent of the non-U.S. commercial

loan portfolio was managed in Global Banking and 28 percent in

Global Markets. Outstanding loans, excluding loans accounted for

under the fair value option, increased $18.8 billion in 2012

primarily due to increased client financing activity, structured

lending and trade finance exposures. Net charge-offs decreased

$124 million in 2012 compared to 2011. For additional

information on the non-U.S. commercial portfolio, see Non-U.S.

Portfolio on page 101.

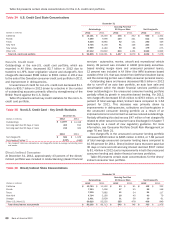

U.S. Small Business Commercial

The U.S. small business commercial loan portfolio is comprised

of small business card and small business loans managed in CBB.

Card-related products were 45 percent and 46 percent of the U.S.

small business commercial portfolio at December 31, 2012 and

2011. U.S. small business commercial net charge-offs decreased

$296 million in 2012 compared to 2011 driven by improvements

in delinquencies, collections and bankruptcies resulting from an

improved economic environment as well as the reduction of higher

risk vintages and the impact of higher credit quality originations.

Of the U.S. small business commercial net charge-offs, 58 percent

were credit card-related products in 2012 compared to 74 percent

in 2011.

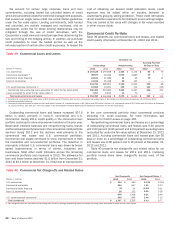

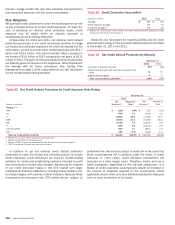

Commercial Loans Accounted for Under the Fair Value

Option

The portfolio of commercial loans accounted for under the fair

value option is managed primarily in Global Banking. Outstanding

commercial loans accounted for under the fair value option

increased $1.4 billion to an aggregate fair value of $8.0 billion at

December 31, 2012 primarily due to increased corporate

borrowings under bank credit facilities. We recorded net gains of

$213 million in 2012 compared to net losses of $174 million in

2011 resulting from changes in the fair value of the loan portfolio.

These amounts were primarily attributable to changes in

instrument-specific credit risk, were recorded in other income

(loss) and do not reflect the results of hedging activities.

In addition, unfunded lending commitments and letters of credit

accounted for under the fair value option had an aggregate fair

value of $528 million and $1.2 billion at December 31, 2012 and

2011 which was recorded in accrued expenses and other

liabilities. The associated aggregate notional amount of unfunded

lending commitments and letters of credit accounted for under the

fair value option was $18.3 billion and $25.7 billion at

December 31, 2012 and 2011. We recorded net gains of $704

million from changes in the fair value of commitments and letters

of credit during 2012 compared to net losses of $429 million in

2011 resulting from maturities and terminations at par value and

changes in the fair value of the loan portfolio. These amounts were

primarily attributable to changes in instrument-specific credit risk,

were recorded in other income (loss) and do not reflect the results

of hedging activities.