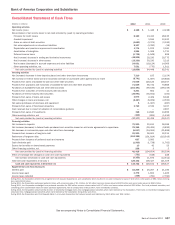

Bank of America 2012 Annual Report Download - page 165

Download and view the complete annual report

Please find page 165 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

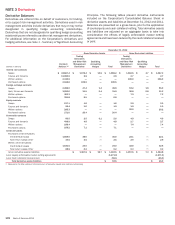

Bank of America 2012 163

to default over a twelve-month period. On home equity loans where

the Corporation holds only a second-lien position and foreclosure

is not the best alternative, the loss severity is estimated at 100

percent.

The allowance on certain commercial loans (except business

card and certain small business loans) is calculated using loss

rates delineated by risk rating and product type. Factors considered

when assessing loss rates include the value of the underlying

collateral, if applicable, the industry of the obligor, and the obligor’s

liquidity and other financial indicators along with certain qualitative

factors. These statistical models are updated regularly for changes

in economic and business conditions. Included in the analysis of

consumer and commercial loan portfolios are reserves which are

maintained to cover uncertainties that affect the Corporation’s

estimate of probable losses including domestic and global

economic uncertainty and large single name defaults.

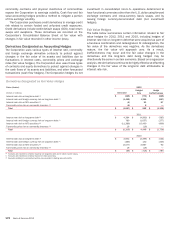

The remaining portfolios, including nonperforming commercial

loans, as well as consumer and commercial loans modified in a

troubled debt restructuring (TDR) are reviewed in accordance with

applicable accounting guidance on impaired loans and TDRs. If

necessary, a specific allowance is established for these loans if

they are deemed to be impaired. A loan is considered impaired

when, based on current information and events, it is probable that

the Corporation will be unable to collect all amounts due, including

principal and/or interest, in accordance with the contractual terms

of the agreement, and once a loan has been identified as impaired,

management measures impairment. Impaired loans and TDRs are

primarily measured based on the present value of payments

expected to be received, discounted at the loans’ original effective

contractual interest rates, or discounted at the portfolio average

contractual annual percentage rate, excluding promotionally priced

loans, in effect prior to restructuring. Impaired loans and TDRs

may also be measured based on observable market prices, or for

loans that are solely dependent on the collateral for repayment,

the estimated fair value of the collateral less estimated costs to

sell. If the recorded investment in impaired loans exceeds this

amount, a specific allowance is established as a component of

the allowance for loan and lease losses unless these are secured

consumer loans that are solely dependent on the collateral for

repayment, in which case the initial amount that exceeds the fair

value of the collateral is charged off.

Generally, when determining the fair value of the collateral

securing consumer real estate-secured loans that are solely

dependent on the collateral for repayment, prior to performing a

detailed property valuation including a walk-through of a property,

the Corporation initially estimates the fair value of the collateral

securing these consumer loans using an automated valuation

method (AVM). An AVM is a tool that estimates the value of a

property by reference to market data including sales of comparable

properties and price trends specific to the Metropolitan Statistical

Area in which the property being valued is located. In the event

that an AVM value is not available, the Corporation utilizes

publicized indices or if these methods provide less reliable

valuations, the Corporation uses appraisals or broker price

opinions to estimate the fair value of the collateral. While there is

inherent imprecision in these valuations, the Corporation believes

that they are representative of the portfolio in the aggregate.

In addition to the allowance for loan and lease losses, the

Corporation also estimates probable losses related to unfunded

lending commitments, such as letters of credit and financial

guarantees, and binding unfunded loan commitments. The reserve

for unfunded lending commitments excludes commitments

accounted for under the fair value option. Unfunded lending

commitments are subject to individual reviews and are analyzed

and segregated by risk according to the Corporation’s internal risk

rating scale. These risk classifications, in conjunction with an

analysis of historical loss experience, utilization assumptions,

current economic conditions, performance trends within the

portfolio and any other pertinent information, result in the

estimation of the reserve for unfunded lending commitments.

The allowance for credit losses related to the loan and lease

portfolio is reported separately on the Consolidated Balance Sheet

whereas the reserve for unfunded lending commitments is

reported on the Consolidated Balance Sheet in accrued expenses

and other liabilities. The provision for credit losses related to the

loan and lease portfolio and unfunded lending commitments is

reported in the Consolidated Statement of Income.

Nonperforming Loans and Leases, Charge-offs and

Delinquencies

Nonperforming loans and leases generally include loans and

leases that have been placed on nonaccrual status, including

nonaccruing loans whose contractual terms have been

restructured in a manner that grants a concession to a borrower

experiencing financial difficulties. Loans accounted for under the

fair value option, PCI loans and LHFS are not reported as

nonperforming loans and leases.

In accordance with the Corporation’s policies, consumer real

estate-secured loans, including residential mortgages and home

equity loans, are generally placed on nonaccrual status and

classified as nonperforming at 90 days past due unless repayment

of the loan is insured by the Federal Housing Administration (FHA)

or through individually insured long-term standby agreements with

Fannie Mae (FNMA) or Freddie Mac (FHLMC) (the fully-insured

portfolio). Residential mortgage loans in the fully-insured portfolio

are not placed on nonaccrual status and, therefore, are not

reported as nonperforming loans. Junior-lien home equity loans

are placed on nonaccrual status and classified as nonperforming

when the underlying first-lien mortgage loan becomes 90 days

past due even if the junior-lien loan is current. Accrued interest

receivable is reversed when a consumer loan is placed on

nonaccrual status. Interest collections on nonaccruing consumer

loans for which the ultimate collectability of principal is uncertain

are generally applied as principal reductions; otherwise, such

collections are credited to interest income when received. These

loans may be restored to accrual status when all principal and

interest is current and full repayment of the remaining contractual

principal and interest is expected, or when the loan otherwise

becomes well-secured and is in the process of collection. The

outstanding balance of real estate-secured loans that is in excess

of the estimated property value, less estimated costs to sell, is

charged off no later than the end of the month in which the account

becomes 180 days past due unless the loan is fully insured. The

estimated property value, less estimated costs to sell, is

determined using the same process as described for impaired

loans in the Allowance for Credit Losses section of this Note.

Consumer loans secured by personal property, credit card loans

and other unsecured consumer loans are not placed on nonaccrual

status prior to charge-off and, therefore, are not reported as

nonperforming loans, except for certain secured consumer loans,

including those that have been modified in a TDR. Personal

property-secured loans are charged off to collateral value no later

than the end of the month in which the account becomes 120