Bank of America 2012 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

76 Bank of America 2012

Consumer Portfolio Credit Risk Management

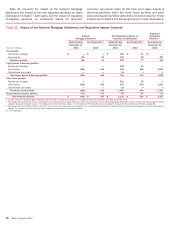

Credit risk management for the consumer portfolio begins with

initial underwriting and continues throughout a borrower’s credit

cycle. Statistical techniques in conjunction with experiential

judgment are used in all aspects of portfolio management

including underwriting, product pricing, risk appetite, setting credit

limits, and establishing operating processes and metrics to

quantify and balance risks and returns. Statistical models are built

using detailed behavioral information from external sources such

as credit bureaus and/or internal historical experience. These

models are a component of our consumer credit risk management

process and are used in part to help make both new and existing

credit decisions, as well as portfolio management strategies,

including authorizations and line management, collection practices

and strategies, determination of the allowance for loan and lease

losses, and economic capital allocations for credit risk.

Since January 2008, and through 2012, Bank of America and

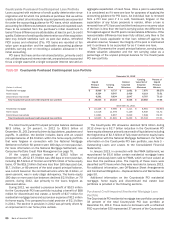

Countrywide have completed approximately 1.2 million loan

modifications with customers. During 2012, we completed more

than 156,000 customer loan modifications with a total unpaid

principal balance of approximately $34 billion, including

approximately 41,400 permanent modifications under the

government’s Making Home Affordable Program. Of the loan

modifications completed in 2012, in terms of both the volume of

modifications and the unpaid principal balance associated with

the underlying loans, most were in the portfolio serviced for

investors and were not on our balance sheet. The most common

types of modifications include a combination of rate reduction

and/or capitalization of past due amounts which represented 54

percent of the volume of modifications completed in 2012, while

principal forbearance represented 18 percent, principal reductions

and forgiveness represented 17 percent and capitalization of past

due amounts represented seven percent. For modified loans on

our balance sheet, these modification types are generally

considered TDRs. For more information on TDRs and portfolio

impacts, see Nonperforming Consumer Loans and Foreclosed

Properties Activity on page 89 and Note 5 – Outstanding Loans

and Leases to the Consolidated Financial Statements.

Consumer Credit Portfolio

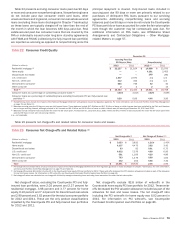

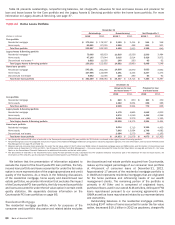

Improvement in the U.S. economy, labor markets and home prices

during 2012 resulted in lower credit losses across all major

consumer portfolios. Although home prices have shown signs of

improvement, the declines over the past several years continued

to adversely impact the home loans portfolio.

Improved credit quality across the consumer portfolio and the

impact of the National Mortgage Settlement, as discussed in the

following section, drove an $8.6 billion decrease in the consumer

allowance for loan and lease losses to $21.1 billion at

December 31, 2012. For more information, see Allowance for

Credit Losses on page 105.

As a result of the National Mortgage Settlement in 2012, which

among other things provided for borrower assistance, we recorded

charge-offs of $435 million related to fully forgiven non-PCI loans

in the home equity portfolio, which resulted in reductions of the

same amount in nonperforming loans. Associated with the

National Mortgage Settlement in 2012, we also fully forgave home

equity loans in the Countrywide PCI portfolio with a carrying value

before reserves of $2.5 billion and an unpaid principal balance of

$2.9 billion which resulted in a decrease in the corresponding

allowance for loan and lease losses. These items had no impact

on the provision for credit losses as these loans were fully

reserved. For more information on the National Mortgage

Settlement, see Off-Balance Sheet Arrangements and Contractual

Obligations – Other Mortgage-related Matters on page 57.

In 2012, new regulatory guidance was issued addressing

consumer real estate loans that have been discharged in Chapter

7 bankruptcy. In accordance with this new guidance, we now

classify consumer real estate and other secured consumer loans

that have been discharged in Chapter 7 bankruptcy and not

reaffirmed by the borrower, as TDRs, irrespective of payment

history or delinquency status, even if the repayment terms for the

loan have not been otherwise modified. We continue to have a lien

on the underlying collateral. Previously, such loans were classified

as TDRs only if there had been a change in contractual payment

terms that represented a concession to the borrower. The net

impact upon implementation to the consumer real estate and other

secured consumer portfolios of adopting this new regulatory

guidance was a $551 million increase in net charge-offs as these

loans were written-down to collateral value, and the full-year impact

was a $596 million increase in net charge-offs in 2012. This also

resulted in an increase of $3.6 billion in TDRs and $1.2 billion in

net new nonperforming loans upon implementation, of which $1.1

billion of such loans were included in nonperforming loans at

December 31, 2012. Of the $1.1 billion, $1.0 billion, or 92

percent, were current on their contractual payments. Of these

contractually current nonperforming loans, more than 70 percent

were discharged in Chapter 7 bankruptcy more than 12 months

ago, and more than 40 percent were discharged 24 months or

more ago. As subsequent cash payments are received, the interest

component of the payments is generally recorded as interest

income on a cash basis and the principal component is generally

recorded as a reduction in the carrying value of the loan. For more

information on the impacts to consumer loans as a result of this

new regulatory guidance, see Note 5 – Outstanding Loans and

Leases to the Consolidated Financial Statements.

In 2012, the bank regulatory agencies jointly issued

interagency supervisory guidance on nonaccrual status for junior-

lien consumer real estate loans. In accordance with this regulatory

interagency guidance, we now classify junior-lien home equity loans

as nonperforming when the first-lien loan becomes 90 days past

due even if the junior-lien loan is performing, and as a result, we

reclassified $1.9 billion of performing home equity loans to

nonperforming upon implementation, and $1.5 billion of such

loans were included in nonperforming loans at December 31,

2012. The regulatory interagency guidance had no impact on our

allowance for loan and lease losses or provision for credit losses

as the delinquency status of the underlying first-lien was already

considered in our reserving process. For more information, see

Consumer Portfolio Credit Risk Management – Home Equity on

page 83 and Table 21.

For further information on our accounting policies regarding

delinquencies, nonperforming status, charge-offs and TDRs for the

consumer portfolio, see Note 1 – Summary of Significant

Accounting Principles to the Consolidated Financial Statements.