Bank of America 2012 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

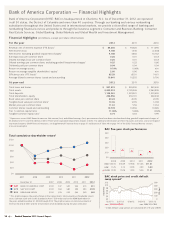

24 Bank of America 2012

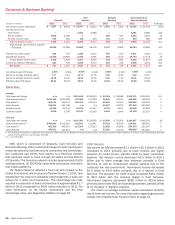

Noninterest income decreased $6.2 billion to $42.7 billion for

2012 compared to 2011. The following highlights the significant

changes.

Card income decreased $1.1 billion primarily driven by the

implementation of interchange fee rules under the Durbin

Amendment, which became effective on October 1, 2011.

Service charges decreased $494 million primarily due to the

impact of lower accretion on acquired portfolios and reduced

reimbursed merchant processing fees.

Investment and brokerage services income decreased $433

million primarily driven by lower transactional volumes.

Equity investment income decreased $5.3 billion. The results

for 2012 included $1.6 billion of gains which primarily related

to the sales of certain equity and strategic investments. The

results for 2011 included $6.5 billion of gains on the sale of

China Construction Bank (CCB) shares, $836 million of CCB

dividends and a $377 million gain on the sale of our investment

in BlackRock, Inc. (BlackRock), partially offset by $1.1 billion of

impairment charges on our merchant services joint venture.

Trading account profits decreased $827 million. Net DVA losses

on derivatives were $2.5 billion in 2012 compared to net DVA

gains of $1.0 billion in 2011. Excluding net DVA, trading account

profits increased $2.7 billion in 2012 compared to 2011 due

to an improved market environment.

Mortgage banking income increased $13.6 billion primarily due

to an $11.7 billion decrease in the representations and

warranties provision. The 2012 results included $2.5 billion in

provision related to the FNMA Settlement, a $500 million

provision for obligations to FNMA related to mortgage insurance

rescissions, partially offset by an increase in servicing income

of $1.1 billion due to improved MSR results. The 2011 results

included $15.6 billion in representations and warranties

provision related to the agreement to resolve nearly all legacy

Countrywide-issued first-lien non-government-sponsored

enterprise (GSE) residential mortgage-backed securities

(RMBS) repurchase exposures and other non-GSE exposures.

Insurance income decreased $1.5 billion driven by the impact

of the sale of the Balboa Insurance Company’s lender-placed

insurance business (Balboa) in 2011 and an increase to the

provision related to payment protection insurance in the U.K. in

2012.

Other income decreased $8.7 billion due to negative fair value

adjustments on our structured liabilities of $5.1 billion

compared to positive fair value adjustments of $3.3 billion in

2011. In addition, 2012 included $1.6 billion of gains related

to debt repurchases and exchanges of trust preferred securities

compared to gains of $1.2 billion in the prior year. The prior year

also included a net gain of $752 million on the sale of Balboa.

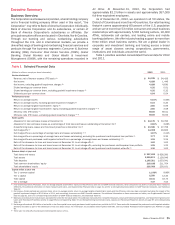

Provision for Credit Losses

The provision for credit losses decreased $5.2 billion to $8.2

billion for 2012 compared to 2011. The provision for credit losses

was $6.7 billion lower than net charge-offs for 2012, resulting in

a reduction in the allowance for credit losses driven by improved

portfolio trends and increasing home prices in consumer real

estate products, lower bankruptcy filings and delinquencies

affecting the Card Services portfolio, and improvement in overall

credit quality within the core commercial portfolio (total

commercial products excluding U.S. small business). Absent

unexpected deterioration in the economy, we expect reductions in

the allowance for credit losses, excluding the valuation allowance

for purchase credit-impaired (PCI) loans, to continue in the near

term, though at a slower pace than in 2012. For more information

on the provision for credit losses, see Provision for Credit Losses

on page 105.

Net charge-offs totaled $14.9 billion, or 1.67 percent of average

loans and leases for 2012 compared to $20.8 billion, or 2.24

percent for 2011. Included in 2012 net charge-offs was $596

million related to the impact of new regulatory guidance regarding

the treatment of loans discharged in Chapter 7 bankruptcy and

$435 million related to loans forgiven as a part of the National

Mortgage Settlement. The decrease in net charge-offs was

primarily driven by fewer delinquent loans and lower bankruptcy

filings in the Card Services portfolio, as well as lower net charge-

offs in the consumer real estate and core commercial portfolios

in 2012.

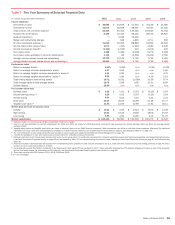

Noninterest Expense

Table 4 Noninterest Expense

(Dollars in millions) 2012 2011

Personnel $ 35,648 $ 36,965

Occupancy 4,570 4,748

Equipment 2,269 2,340

Marketing 1,873 2,203

Professional fees 3,574 3,381

Amortization of intangibles 1,264 1,509

Data processing 2,961 2,652

Telecommunications 1,660 1,553

Other general operating 18,274 21,101

Goodwill impairment —3,184

Merger and restructuring charges —638

Total noninterest expense $ 72,093 $ 80,274

Noninterest expense decreased $8.2 billion to $72.1 billion

for 2012 compared to 2011 with the decrease primarily driven by

the absence of goodwill impairment charges in 2012 compared

to $3.2 billion in 2011, a $2.8 billion decrease in other general

operating expense primarily related to lower litigation expense and

mortgage-related assessments, waivers and similar costs related

to foreclosure delays, partially offset by a provision of $1.1 billion

in 2012 related to the 2013 IFR Acceleration Agreement.

Personnel expense decreased $1.3 billion in 2012 as we

continued to streamline processes and achieve cost savings.

Partially offsetting the decreases were increases in professional

fees and data processing expenses due to continuing default

management activities in Legacy Assets & Servicing. The prior

year also included $638 million in merger and restructuring

charges.

In connection with Project New BAC, we expect to continue to

achieve cost savings in certain noninterest expense categories as

we continue to further streamline workflows, simplify processes

and align expenses with our overall strategic plan and operating

principles. During 2012, we continued implementation of Phase

1 initiatives, completed Phase 2 evaluations and began

implementation of certain Phase 2 initiatives. With regard to Phase

1, we expect to realize more than $5 billion of annualized cost

savings by the fourth quarter of 2013 with the full impact expected

to be realized in 2014. We expect that Phase 2 will result in an

additional $3 billion of annualized cost savings by mid-2015.