Bank of America 2012 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

114 Bank of America 2012

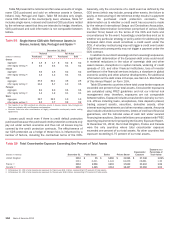

Table 64 shows the pre-tax dollar impact to forecasted net

interest income over the next 12 months from December 31, 2012

and 2011, resulting from instantaneous parallel and non-parallel

shocks to the market-based forward curve. Periodically we evaluate

the scenarios presented to ensure that they are meaningful in the

context of the current rate environment. For more information, see

Net Interest Income Excluding Trading-related Net Interest Income

on page 32.

Table 64 Estimated Net Interest Income Excluding

Trading-related Net Interest Income

(Dollars in millions) Short

Rate (bps)

Long

Rate (bps)

December 31

Curve Change 2012 2011

Parallel Shifts

+100 bps

instantaneous shift +100 +100 $ 4,232 $ 2,883

-50 bps

instantaneous shift -50 -50 (2,250) (1,795)

Flatteners

Short end

instantaneous change +100 — 2,159 979

Long end

instantaneous change — -50 (1,597) (1,319)

Steepeners

Short end

instantaneous change -50 — (655) (464)

Long end

instantaneous change — +100 2,091 1,935

The sensitivity analysis in Table 64 assumes that we take no

action in response to these rate shocks. Our net interest income

was asset sensitive to a parallel move in interest rates at both

December 31, 2012 and 2011. As part of our ALM activities, we

use securities, residential mortgages, and interest rate and foreign

exchange derivatives in managing interest rate sensitivity.

Securities

The securities portfolio is an integral part of our ALM positioning

and is primarily comprised of debt securities including MBS and

to a lesser extent U.S. Treasury, corporate, municipal and other

debt securities. At December 31, 2012 and 2011, we held AFS

debt securities with a fair value of $286.9 billion and $276.2

billion. During 2012 and 2011, we purchased AFS debt and other

securities of $164.5 billion and $99.5 billion, sold $72.4 billion

and $116.8 billion, and had maturities and received paydowns of

$71.5 billion and $56.7 billion. We realized $1.7 billion and $3.4

billion in net gains on sales of debt securities during 2012 and

2011. At December 31, 2012 and 2011, we held $49.5 billion

and $35.3 billion of held-to-maturity securities and $14.5 billion

of other securities classified as other assets. There were no

securities classified as other assets during 2011.

Accumulated OCI included after-tax net unrealized gains of $4.4

billion and $3.1 billion on AFS debt securities and $462 million

and $3 million on AFS marketable equity securities at December

31, 2012 and 2011. For additional information on accumulated

OCI, see Note 15 – Accumulated Other Comprehensive Income

(Loss) to the Consolidated Financial Statements. The amount of

pre-tax net unrealized gains on AFS debt securities increased $2.1

billion during 2012 to $7.0 billion, primarily due to the impact of

lower rates. For additional information on our securities portfolio,

see Note 4 – Securities to the Consolidated Financial Statements.

We recognized $53 million of other-than-temporary impairment

(OTTI) losses in earnings on AFS debt securities in 2012 compared

to $299 million in 2011. The recognition of OTTI is based on a

variety of factors, including the length of time and extent to which

the market value has been less than amortized cost, the financial

condition of the issuer of the security including credit ratings and

any specific events affecting the operations of the issuer,

underlying assets that collateralize the debt security, other industry

and macroeconomic conditions, and our intent and ability to hold

the security to recovery.

Residential Mortgage Portfolio

At December 31, 2012 and 2011, our residential mortgage

portfolio was $243.2 billion and $262.3 billion which excluded

$9.9 billion and $11.1 billion of discontinued real estate loans

and $1.0 billion and $2.2 billion of consumer loans accounted for

under the fair value option. For more information on consumer fair

value option loans, see Consumer Portfolio Credit Risk

Management – Consumer Loans Accounted for Under the Fair

Value Option on page 89. The $19.1 billion decrease in 2012 was

due to paydowns, charge-offs and transfers to foreclosed

properties which more than offset new origination volume and

repurchases of delinquent FHA loans pursuant to our servicing

agreements with GNMA.

During 2012, CRES and GWIM originated $35.4 billion in first-

lien mortgages that we retained compared to $45.5 billion in 2011.

Additionally, we repurchased $8.2 billion of delinquent FHA loans

pursuant to our servicing agreements with GNMA compared to

repurchases of $7.8 billion in 2011. We received paydowns of

$53.0 billion in 2012 compared to paydowns of $42.3 billion in

2011. There were no purchases of residential mortgages related

to ALM activities in 2012 compared to $72 million in 2011. We

sold $305 million of residential mortgages in 2012 compared to

$109 million in 2011, all of which were originated residential

mortgages. Gains recognized on the sales of residential

mortgages in both periods were minimal.

Interest Rate and Foreign Exchange Derivative

Contracts

Interest rate and foreign exchange derivative contracts are utilized

in our ALM activities and serve as an efficient tool to manage our

interest rate and foreign exchange risk. We use derivatives to

hedge the variability in cash flows or changes in fair value on our

balance sheet due to interest rate and foreign exchange

components. For additional information on our hedging activities,

see Note 3 – Derivatives to the Consolidated Financial Statements.

Our interest rate contracts are generally non-leveraged generic

interest rate and foreign exchange basis swaps, options, futures

and forwards. In addition, we use foreign exchange contracts,

including cross-currency interest rate swaps, foreign currency

forward contracts and options to mitigate the foreign exchange

risk associated with foreign currency-denominated assets and

liabilities.

Changes to the composition of our derivatives portfolio during

2012 reflect actions taken for interest rate and foreign exchange

rate risk management. The decisions to reposition our derivatives

portfolio are based on the current assessment of economic and

financial conditions including the interest rate and foreign currency

environments, balance sheet composition and trends, the asset

sensitivity of our balance sheet and the relative mix of our cash

and derivative positions.