Bank of America 2012 Annual Report Download - page 243

Download and view the complete annual report

Please find page 243 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

Bank of America 2012 241

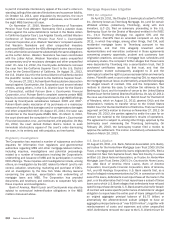

Rule. The Corporation measures and reports its capital ratios and

related information under Basel 2 on a confidential basis to U.S.

banking regulators during the required parallel period which will

continue until the Corporation receives regulatory approval to exit

parallel reporting and subsequently begin publicly reporting Basel

2 regulatory capital results and related disclosures.

In June 2012, U.S. banking regulators issued three notices of

proposed rulemaking (collectively, the Basel 3 NPRs), which, if

adopted as proposed, would materially change Tier 1 common,

Tier 1 and Total capital calculations, introduce new minimum

capital ratios and buffer requirements, expand and modify the

calculation of risk-weighted assets for credit and market risk (the

Advanced Approach) and introduce a Standardized Approach for

the calculation of risk-weighted assets, which would replace Basel

1 and provide a floor for minimum, adequately capitalized

regulatory capital requirements under the Prompt Corrective Action

framework. The Prompt Corrective Action framework establishes

categories of capitalization, including “well-capitalized,” based on

regulatory ratio requirements. U.S. banking regulators are required

to take certain mandatory actions depending on the category of

capitalization. No mandatory actions are required under the

Prompt Corrective Action framework for “well-capitalized” banking

entities.

Under the Basel 3 NPRs, Trust Securities will be phased out

of Tier 1 capital in equal annual installments over a three-year

transition period. Many of the changes to the composition of

regulatory capital are subject to a transition period where the

impact is recognized in 20 percent increments, phased in

incrementally each year over a five-year period. The majority of the

other aspects of the Advanced Approach were proposed to become

effective on January 1, 2013. The phase-in period for the new

minimum capital requirements and related buffers is proposed to

occur from the effective date of the Basel 3 NPRs through 2019.

U.S. banking regulators announced that they did not expect any

of the Basel 3 NPRs to become effective January 1, 2013. Final

rules for Basel 3 have not yet been issued by U.S. banking

regulators.

Under the Basel 3 NPRs the Corporation will be subject to the

Advanced Approach for measuring risk-weighted assets (Basel 3

Advanced Approach) when finalized and implemented. The Basel

3 Advanced Approach also requires approval by the U.S. regulatory

agencies of analytical models used as part of capital

measurement. If these models are not approved, it would likely

lead to an increase in the Corporation’s risk-weighted assets, which

in some cases could be significant. The Basel 3 Advanced

Approach, if adopted as proposed, is expected to substantially

increase the Corporation’s capital requirements.

In 2011, the Basel Committee on Banking Supervision issued

guidance on capital requirements for global, systemically

important financial institutions, including the methodology for

measuring systemic importance (the SIFI buffer), and the

arrangements by which the guidance will be phased in. As

proposed, the SIFI buffer would increase minimum capital

requirements for Tier 1 common capital from one percent to 2.5

percent, and in certain circumstances, 3.5 percent. U.S. banking

regulators have not yet issued proposed or final rules related to

the SIFI buffer.

On December 20, 2011, the Federal Reserve issued proposed

rules to implement enhanced supervisory and prudential

requirements and the early remediation requirements established

under the Dodd-Frank Wall Street Reform and Consumer Protection

Act. The enhanced standards include risk-based capital and

leverage requirements, liquidity standards, requirements for

overall risk management, single-counterparty credit limits, stress

test requirements and a debt-to-equity limit for certain companies

determined to pose a threat to financial stability. The final rules

are likely to influence regulatory capital and liquidity planning

processes, and may impose additional operational and compliance

costs on the Corporation.

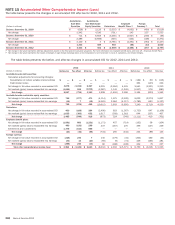

Other Regulatory Requirements

The Federal Reserve requires the Corporation’s banking

subsidiaries to maintain reserve balances based on a percentage

of certain deposits. Average daily reserve balances required by

the Federal Reserve were $16.3 billion and $14.6 billion for 2012

and 2011. Currency and coin residing in branches and cash vaults

(vault cash) are used to partially satisfy the reserve requirement.

The average daily reserve balances, in excess of vault cash, held

with the Federal Reserve amounted to $7.9 billion and $6.5 billion

for 2012 and 2011. As of December 31, 2012, the Corporation

had cash in the amount of $8.5 billion and securities with a fair

value of $5.9 billion that were segregated in compliance with

securities regulations or deposited with clearing organizations.

The primary sources of funds for cash distributions by the

Corporation to its shareholders are capital distributions received

from its banking subsidiaries, BANA and FIA. In 2012, the

Corporation received $14.1 billion in dividends from BANA and FIA,

and returned capital of $6.6 billion to the Corporation. In 2013,

BANA can declare and pay dividends to the Corporation equal to

their retained net profits for 2013 up to the date of any dividend

declaration. The other subsidiary national banks paid $1.6 billion

in dividends to the Corporation in 2012 and can pay dividends in

aggregate of $203 million in 2013 plus an additional amount equal

to their retained net profits for 2013 up to the date of any such

dividend declaration. The amount of dividends that each subsidiary

bank may declare in a calendar year is the subsidiary bank’s net

profits for that year combined with its retained net profits for the

preceding two years. Retained net profits, as defined by the OCC,

consist of net income less dividends declared during the period.

NOTE 18 Employee Benefit Plans

Pension and Postretirement Plans

The Corporation sponsors noncontributory trusteed pension plans,

a number of noncontributory nonqualified pension plans, and

postretirement health and life plans that cover eligible employees.

As discussed below, certain of the pension plans were amended,

effective June 30, 2012, to freeze benefits earned. The plans

provide defined benefits based on an employee’s compensation

and years of service. The Bank of America Pension Plan (the

Pension Plan) provides participants with compensation credits,

generally based on years of service. For account balances based

on compensation credits prior to January 1, 2008, the Pension

Plan allows participants to select from various earnings measures,

which are based on the returns of certain funds or common stock

of the Corporation. The participant-selected earnings measures

determine the earnings rate on the individual participant account

balances in the Pension Plan. Participants may elect to modify

earnings measure allocations on a periodic basis subject to the

provisions of the Pension Plan. For account balances based on

compensation credits subsequent to December 31, 2007, the

account balance earnings rate is based on a benchmark rate. For

eligible employees in the Pension Plan on or after January 1, 2008,