Bank of America 2012 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2012 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

|

|

104 Bank of America 2012

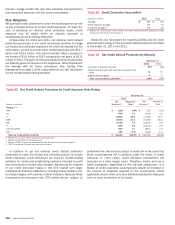

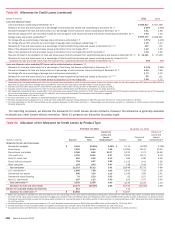

Table 58 presents the notional and fair value amounts of single-

name CDS purchased and sold on reference assets in Greece,

Ireland, Italy, Portugal and Spain. Table 58 includes only single-

name CDS netted at the counterparty level, whereas, Table 57

includes single-name, indexed and tranched CDS positions netted

by the reference asset that they are intended to hedge; therefore,

CDS purchased and sold information is not comparable between

tables.

Table 58 Single-Name CDS with Reference Assets in

Greece, Ireland, Italy, Portugal and Spain (1)

December 31, 2012

Notional Fair Value

(Dollars in billions) Purchased Sold Purchased Sold

Greece

Aggregate $ 1.8 $ 1.7 $ 0.2 $ 0.2

After legally netting (2) 0.4 0.4 0.1 0.1

Ireland

Aggregate 3.0 2.8 0.2 0.2

After legally netting (2) 1.4 1.2 0.1 0.1

Italy

Aggregate 47.4 42.1 3.5 2.8

After legally netting (2) 11.0 5.7 1.3 0.5

Portugal

Aggregate 8.1 8.0 0.5 0.5

After legally netting (2) 1.3 1.2 0.1 0.1

Spain

Aggregate 22.7 22.3 1.0 1.0

After legally netting (2) 4.0 3.7 0.2 0.2

(1) The majority of our CDS contracts on reference assets in Greece, Ireland, Italy, Portugal and

Spain are primarily with non-Eurozone counterparties.

(2) Amounts listed are after consideration of legally enforceable counterparty master netting

agreements.

Losses could result even if there is credit default protection

purchased because the purchased credit protection contracts only

pay out under certain scenarios and thus not all losses may be

covered by the credit protection contracts. The effectiveness of

our CDS protection as a hedge of these risks is influenced by a

number of factors, including the contractual terms of the CDS.

Generally, only the occurrence of a credit event as defined by the

CDS terms (which may include, among other events, the failure to

pay by, or restructuring of, the reference entity) results in a payment

under the purchased credit protection contracts. The

determination as to whether a credit event has occurred is made

by the relevant International Swaps and Derivatives Association,

Inc. (ISDA) Determination Committee (comprised of various ISDA

member firms) based on the terms of the CDS and facts and

circumstances for the event. Accordingly, uncertainties exist as to

whether any particular strategy or policy action for addressing the

European debt crisis would constitute a credit event under the

CDS. A voluntary restructuring may not trigger a credit event under

CDS terms and consequently may not trigger a payment under the

CDS contract.

In addition to our direct sovereign and non-sovereign exposures,

a significant deterioration of the European debt crisis could result

in material reductions in the value of sovereign debt and other

asset classes, disruptions in capital markets, widening of credit

spreads of U.S. and other financial institutions, loss of investor

confidence in the financial services industry, a slowdown in global

economic activity and other adverse developments. For additional

information on the debt crisis in Europe, see Item 1A. Risk Factors

of this Annual Report on Form 10-K.

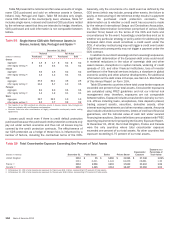

Table 59 presents countries where total cross-border exposure

exceeded one percent of our total assets. Cross-border exposures

are calculated using FFIEC guidelines and not our internal risk

management view; therefore, exposures are not comparable

between tables. Exposure includes cross-border claims by our non-

U.S. offices including loans, acceptances, time deposits placed,

trading account assets, securities, derivative assets, other

interest-earning investments and other monetary assets. Amounts

also include unfunded commitments, letters of credit and financial

guarantees, and the notional value of cash lent under secured

financing transactions. Sector definitions are consistent with FFIEC

reporting requirements for preparing the Country Exposure Report.

At December 31, 2012, the United Kingdom, France and Canada

were the only countries where total cross-border exposure

exceeded one percent of our total assets. No other countries had

exposure exceeding 0.75 percent of our total assets.

Table 59 Total Cross-border Exposure Exceeding One Percent of Total Assets

(Dollars in millions) December 31 Public Sector Banks Private Sector

Cross-border

Exposure

Exposure as a

Percentage of

Total Assets

United Kingdom 2012 $ 95 $ 5,656 $ 31,595 $ 37,346 1.69%

2011 6,401 4,424 18,056 28,881 1.36

France (1) 2012 2,556 3,215 17,639 23,410 1.06

Canada (2) 2012 1,325 3,314 18,427 23,066 1.04

(1) At December 31, 2011, total cross-border exposure for France was $16.1 billion, representing 0.75 percent of total assets.

(2) At December 31, 2011, total cross-border exposure for Canada was $16.9 billion, representing 0.79 percent of total assets.